Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop and analyze a class of unbiased Monte Carlo estimators for multivariate jump-diffusion processes with state-dependent drift, volatility, jump intensity and jump size. A change of measure ...

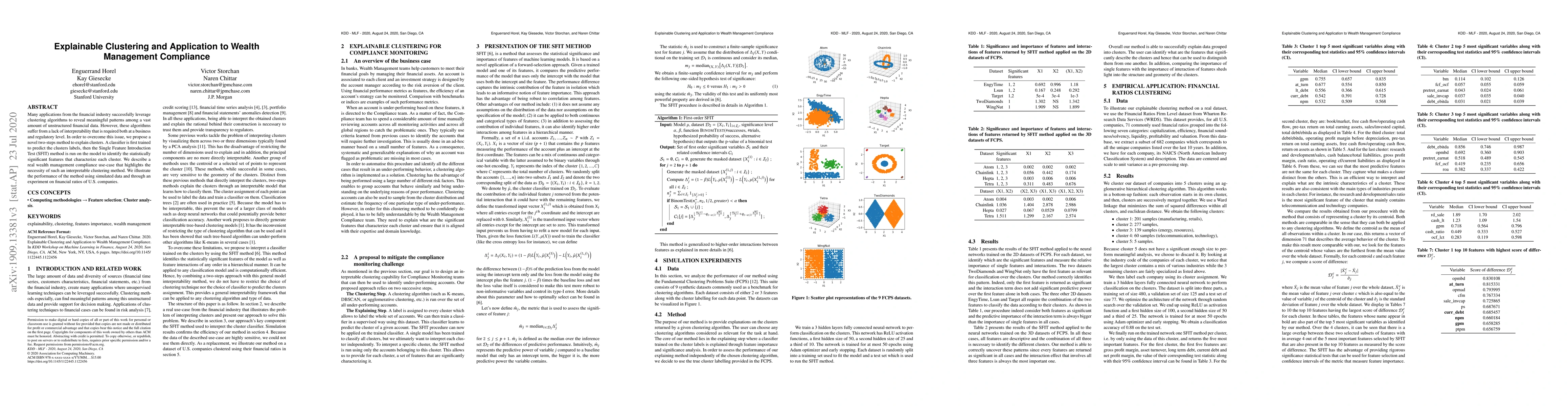

Many applications from the financial industry successfully leverage clustering algorithms to reveal meaningful patterns among a vast amount of unstructured financial data. However, these algorithms ...

We develop a pivotal test to assess the statistical significance of the feature variables in a single-layer feedforward neural network regression model. We propose a gradient-based test statistic an...

Although neural networks can achieve very high predictive performance on various different tasks such as image recognition or natural language processing, they are often considered as opaque "black ...

In many financial prediction problems, the behavior of individual units (such as loans, bonds, or stocks) is influenced by observable unit-level factors and macroeconomic variables, as well as by late...

The opacity of many supervised learning algorithms remains a key challenge, hindering scientific discovery and limiting broader deployment -- particularly in high-stakes domains. This paper develops m...

Panel data, in which multiple units are repeatedly observed over time, arise throughout science and engineering. Quantifying predictive uncertainty in such settings is challenging because conformal pr...

As high-quality public web corpora become increasingly exhausted, clean long-context documents have become a scarce and expensive source of training data for large language models (LLMs). Existing lon...