Academic Profile

Statistics

Similar Authors

Papers on arXiv

Coupon allocation drives customer purchases and boosts revenue. However, it presents a fundamental trade-off between exploiting the current optimal policy to maximize immediate revenue and exploring a...

We consider solving linear optimization (LO) problems with uncertain objective coefficients. For such problems, we often employ robust optimization (RO) approaches by introducing an uncertainty set ...

Off-Policy Evaluation (OPE) aims to assess the effectiveness of counterfactual policies using only offline logged data and is often used to identify the top-k promising policies for deployment in on...

This paper introduces SCOPE-RL, a comprehensive open-source Python software designed for offline reinforcement learning (offline RL), off-policy evaluation (OPE), and selection (OPS). Unlike most ex...

In modern recommendation systems, unbiased learning-to-rank (LTR) is crucial for prioritizing items from biased implicit user feedback, such as click data. Several techniques, such as Inverse Propen...

We first provide an inner-approximation hierarchy described by a sum-of-squares (SOS) constraint for the copositive (COP) cone over a general symmetric cone. The hierarchy is a generalization of tha...

In this study, we examine the various extensions of the doubly nonnegative (DNN) cone, frequently used in completely positive programming (CPP) to achieve a tighter relaxation than the positive semi...

This paper studies a distributionally robust portfolio optimization model with a cardinality constraint for limiting the number of invested assets. We formulate this model as a mixed-integer semidef...

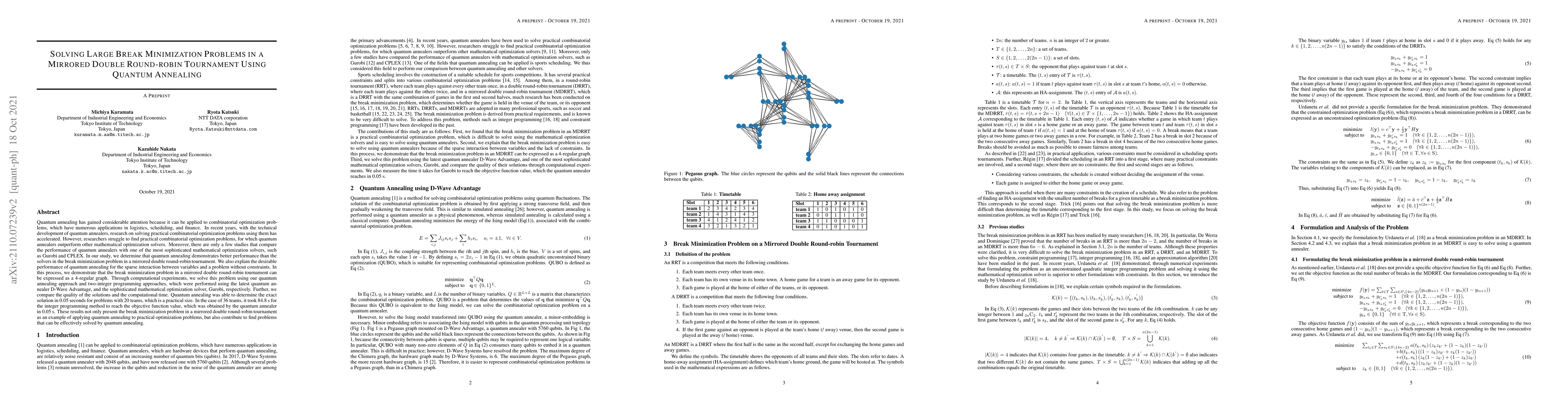

Quantum annealing (QA) has gained considerable attention because it can be applied to combinatorial optimization problems, which have numerous applications in logistics, scheduling, and finance. In ...

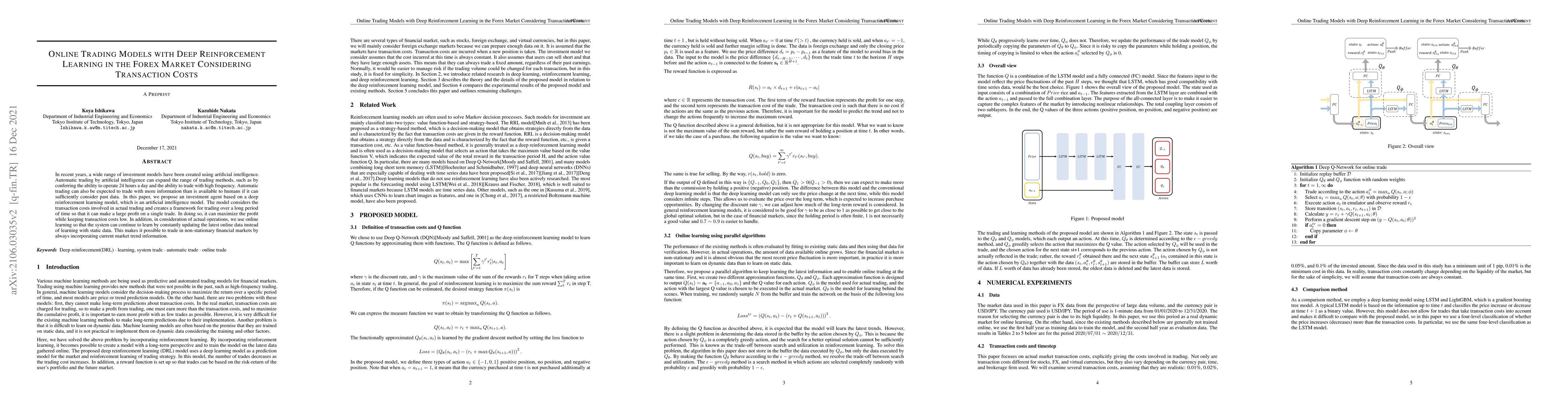

In recent years, a wide range of investment models have been created using artificial intelligence. Automatic trading by artificial intelligence can expand the range of trading methods, such as by c...

In recent years, machine learning and AI have been introduced in many industrial fields. In fields such as finance, medicine, and autonomous driving, where the inference results of a model may have ...

Japanese patents are assigned a patent classification code, FI (File Index), that is unique to Japan. FI is a subdivision of the IPC, an international patent classification code, that is related to ...

The problem of sensor network localization (SNL) can be formulated as a semidefinite programming problem with a rank constraint. We propose a new method for solving such SNL problems. We factorize a...

Recommender systems widely use implicit feedback such as click data because of its general availability. Although the presence of clicks signals the users' preference to some extent, the lack of suc...

For quantitative trading risk management purposes, we present a novel idea: the realized local volatility surface. Concisely, it stands for the conditional expected volatility when sudden market behav...

Semidefinite programming (SDP) relaxation has emerged as a promising approach for neural network verification, offering tighter bounds than other convex relaxation methods for deep neural networks (DN...

This paper focuses on forecasting hierarchical time-series data, where each higher-level observation equals the sum of its corresponding lower-level time series. In such contexts, the forecast values ...

In this paper, we propose a method for generating layouts for image-based advertisements by leveraging a Vision-Language Model (VLM). Conventional advertisement layout techniques have predominantly re...

The Wasserstein distance is a discrepancy measure between probability distributions, defined by an optimal transport problem. It has been used for various tasks such as retrieving similar items in hig...