Academic Profile

Statistics

Similar Authors

Papers on arXiv

This study proposes a reversible jump Markov chain Monte Carlo method for estimating parameters of lognormal distribution mixtures for income. Using simulated data examples, we examined the proposed...

Using the asymmetric stochastic volatility model, this study investigates the day-of-the-week and holiday effects on the returns and volatility of Bitcoin from January 1, 2013 to August 31, 2019; in...

This study is concerned with estimating the inequality measures associated with the underlying hypothetical income distribution from the times series grouped data on the Lorenz curve. We adopt the D...

We examine the effects of monetary policy on income inequality in Japan using a novel econometric approach that jointly estimates the Gini coefficient based on micro-level grouped data of households...

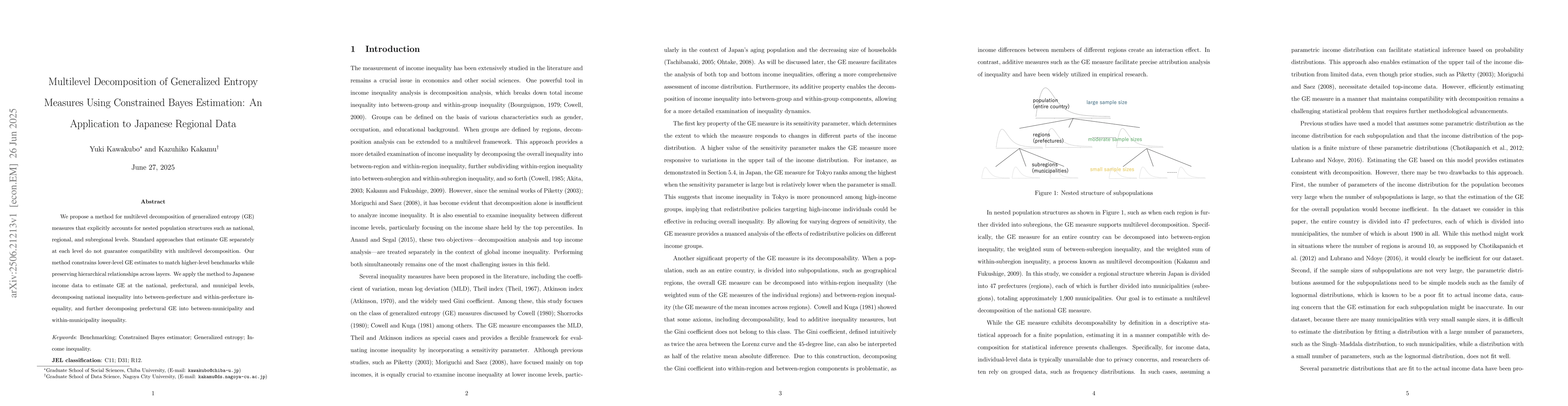

We propose a method for multilevel decomposition of generalized entropy (GE) measures that explicitly accounts for nested population structures such as national, regional, and subregional levels. Stan...

We develop a Bayesian state-space model for analyzing the dynamic evolution of income distributions using grouped income data. The model combines the generalized beta distribution of the second kind (...