Academic Profile

Statistics

Similar Authors

Papers on arXiv

We discuss model and forecast combination in time series forecasting. A foundational Bayesian perspective based on agent opinion analysis theory defines a new framework for density forecast combinat...

We discuss the relation between the statistical question of inadmissibility and the probabilistic question of transience. Brown (1971) proved the mathematical link between the admissibility of the m...

The estimation of heterogeneous treatment effects in the potential outcome setting is biased when there exists model misspecification or unobserved confounding. As these biases are unobservable, wha...

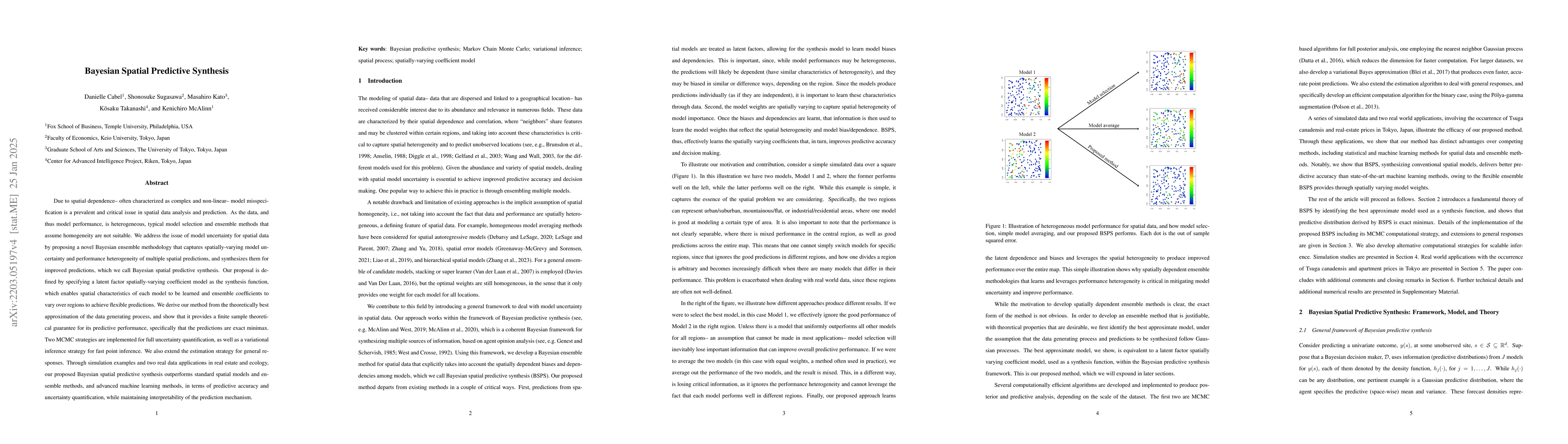

Spatial data are characterized by their spatial dependence, which is often complex, non-linear, and difficult to capture with a single model. Significant levels of model uncertainty -- arising from ...

We consider the "policy choice" problem -- otherwise known as best arm identification in the bandit literature -- proposed by Kasy and Sautmann (2021) for adaptive experimental design. Theorem 1 of ...

We consider learning causal relationships under conditional moment restrictions. Unlike causal inference under unconditional moment restrictions, conditional moment restrictions pose serious challen...

This paper studies the asymptotic convergence of computed dynamic models when the shock is unbounded. Most dynamic economic models lack a closed-form solution. As such, approximate solutions by nume...

We consider controlling the false discovery rate for testing many time series with an unknown cross-sectional correlation structure. Given a large number of hypotheses, false and missing discoveries...

This paper proposes a new estimator for selecting weights to average over least squares estimates obtained from a set of models. Our proposed estimator builds on the Mallows model average (MMA) esti...

We discuss the finite sample theoretical properties of online predictions in non-stationary time series under model misspecification. To analyze the theoretical predictive properties of statistical ...

We develop the methodology and a detailed case study in use of a class of Bayesian predictive synthesis (BPS) models for multivariate time series forecasting. This extends the recently introduced fo...

We address the problem of dynamic variable selection in time series regression with unknown residual variances, where the set of active predictors is allowed to evolve over time. To capture time-var...

The doubly robust estimator, which models both the propensity score and outcomes, is a popular approach to estimate the average treatment effect in the potential outcome setting. The primary appeal of...

Cross-validation is a standard technique used across science to test how well a model predicts new data. Data are split into $K$ "folds," where one fold (i.e., hold-out set) is used to evaluate a mode...

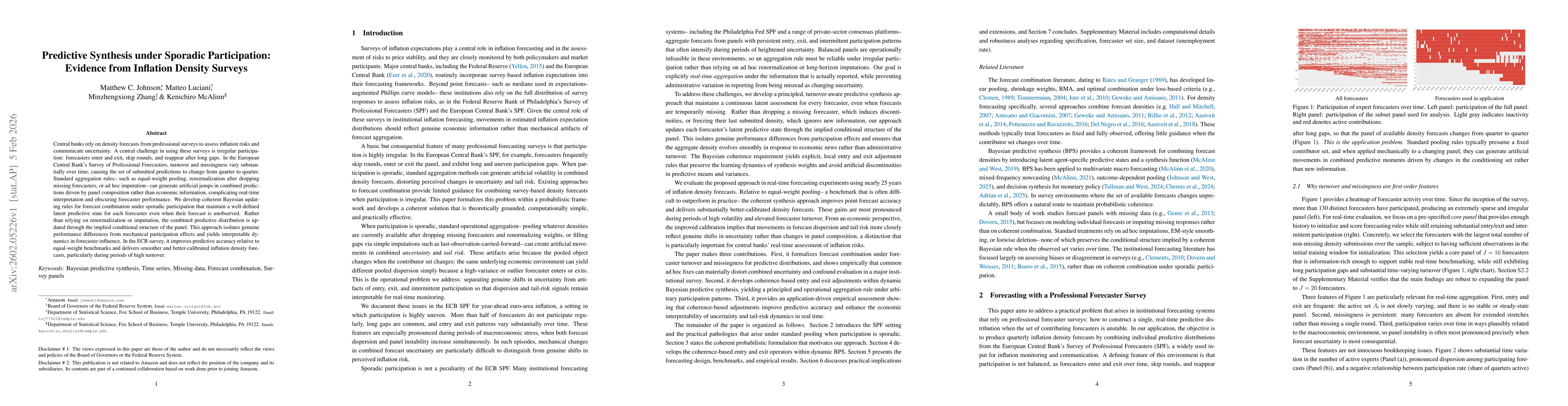

Central banks rely on density forecasts from professional surveys to assess inflation risks and communicate uncertainty. A central challenge in using these surveys is irregular participation: forecast...

Loss-based updating, including generalized Bayes, Gibbs, and quasi-posteriors, replaces likelihoods by a user-chosen loss and produces a posterior-like distribution via exponential tilt. We give a dec...

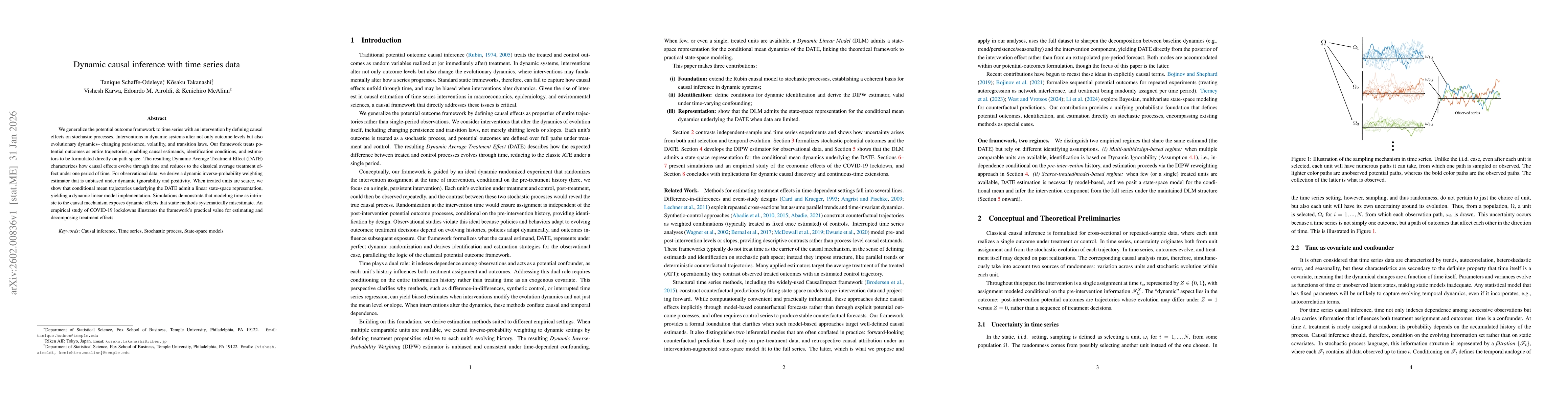

We generalize the potential outcome framework to time series with an intervention by defining causal effects on stochastic processes. Interventions in dynamic systems alter not only outcome levels but...

We consider predictive density estimation under logarithmic score for $d$-dimensional infinitely divisible location models. Taking the formal Bayes predictive density under the Lebesgue prior as a ben...