Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper introduces PINT (Physics-Informed Neural Time Series Models), a framework that integrates physical constraints into neural time series models to improve their ability to capture complex dyn...

Visual food recognition systems deployed in real-world environments, such as automated conveyor-belt inspection, are highly sensitive to domain shifts caused by illumination changes. While recent stud...

Accurate quantification of the relationship between forest loss and associated carbon emissions is critical for both environmental monitoring and policy evaluation. Although many studies have document...

Industrial fruit inspection systems must operate reliably under dense multi-object interactions and continuous motion, yet most existing works evaluate detection or classification at the image level w...

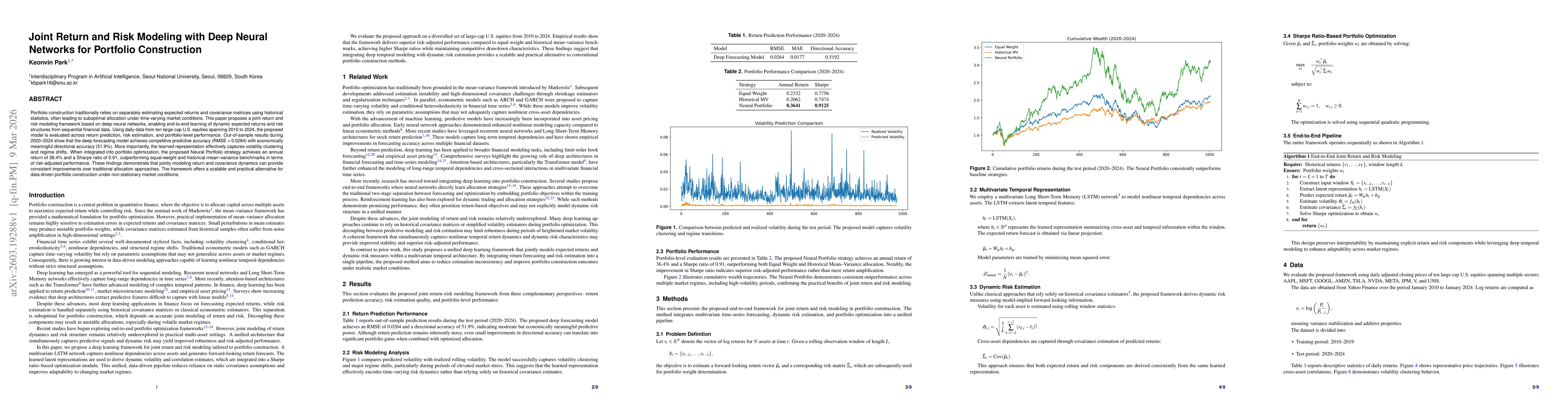

Portfolio construction traditionally relies on separately estimating expected returns and covariance matrices using historical statistics, often leading to suboptimal allocation under time-varying mar...