Academic Profile

Statistics

Similar Authors

Papers on arXiv

Statistical arbitrage is a prevalent trading strategy which takes advantage of mean reverse property of spread of paired stocks. Studies on this strategy often rely heavily on model assumption. In t...

In this paper, we explore an optimal timing strategy for the trading of price spreads exhibiting mean-reverting characteristics. A sequential optimal stopping framework is formulated to analyze the ...

This paper studies how to price and hedge options under stock models given as a path-dependent SDE solution. When the path-dependent SDE coefficients have Fr\'{e}chet derivatives, an option price is...

We propose the Hawkes flocking model that assesses systemic risk in high-frequency processes at the two perspectives -- endogeneity and interactivity. We examine the futures markets of WTI crude oil...

We study the optimal order placement strategy with the presence of a liquidity cost. In this problem, a stock trader wishes to clear her large inventory by a predetermined time horizon $T$. A trader...

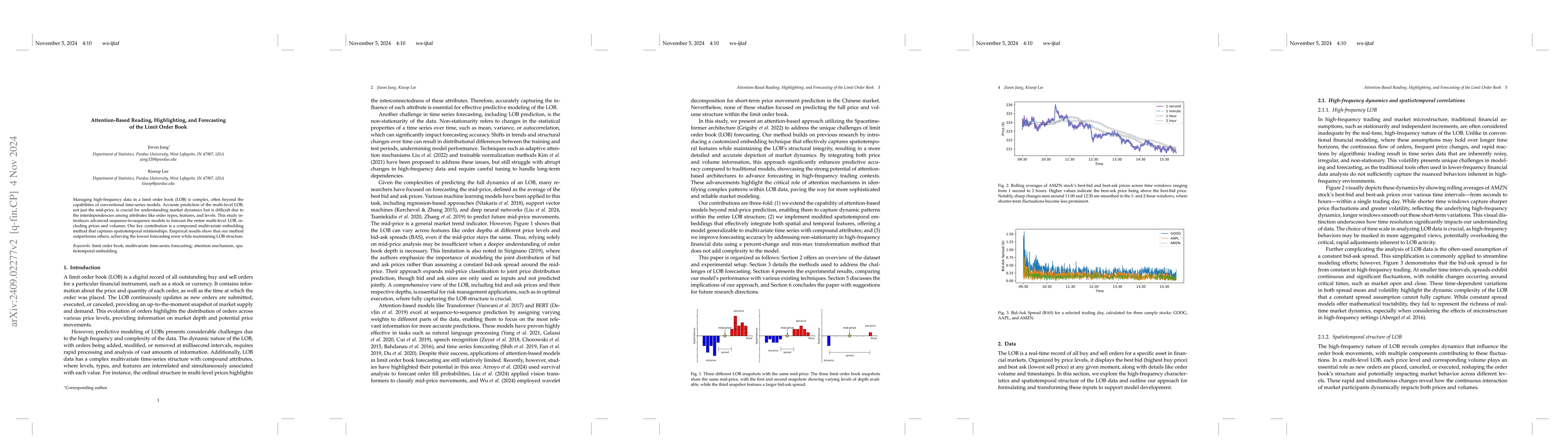

Managing high-frequency data in a limit order book (LOB) is a complex task that often exceeds the capabilities of conventional time-series forecasting models. Accurately predicting the entire multi-le...

Deep hedging uses recurrent neural networks to hedge financial products that cannot be fully hedged in incomplete markets. Previous work in this area focuses on minimizing some measure of quadratic he...

The signature transform is a principled feature map for continuous-time paths, valued for its uniqueness and universality. Recovering a path from its truncated signature is, however, structurally ill-...