Academic Profile

Statistics

Similar Authors

Papers on arXiv

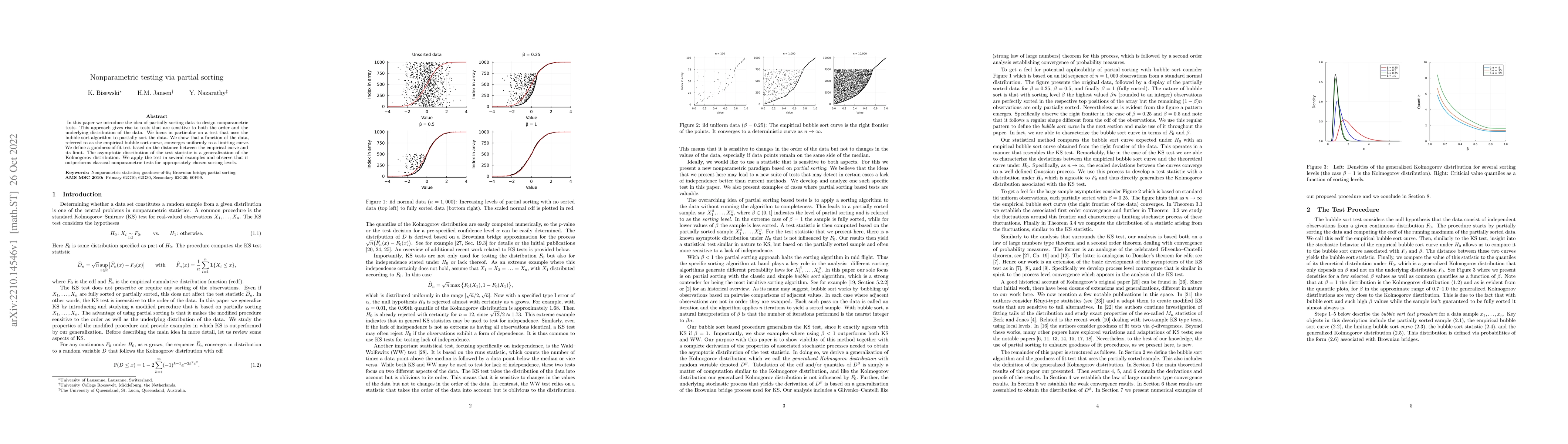

In this paper we introduce the idea of partially sorting data to design nonparametric tests. This approach gives rise to tests that are sensitive to both the order and the underlying distribution of...

In this paper we derive an upper bound for the difference between the continuous and discrete Piterbarg constants. Our result allows us to approximate the classical Piterbarg constants by their disc...

We derive a new theoretical lower bound for the expected supremum of drifted fractional Brownian motion with Hurst index $H\in(0,1)$ over (in)finite time horizon. Extensive simulation experiments in...

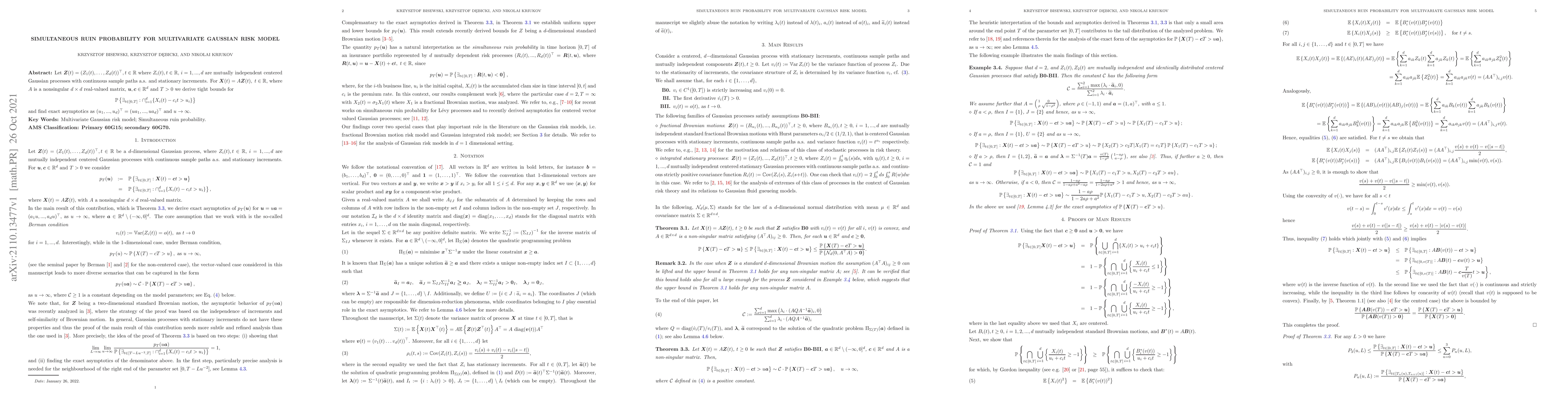

Let $\textbf{Z}(t)=(Z_1(t) ,\ldots, Z_d(t))^\top , t \in \mathbb{R}$ where $Z_i(t), t\in \mathbb{R}$, $i=1,...,d$ are mutually independent centered Gaussian processes with continuous sample paths a....

We consider a family of sup-functionals of (drifted) fractional Brownian motion with Hurst parameter $H\in(0,1)$. This family includes, but is not limited to: expected value of the supremum, expecte...

In this manuscript, we address open questions raised by Dieker \& Yakir (2014), who proposed a novel method of estimation of (discrete) Pickands constants $\mathcal{H}^\delta_\alpha$ using a family ...

Motivated by the harmonic mean formula in [1], we investigate the relation between the sojourn time and supremum of a random process $X(t),t\in \mathbb{R}^d$ and extend the harmonic mean formula for...

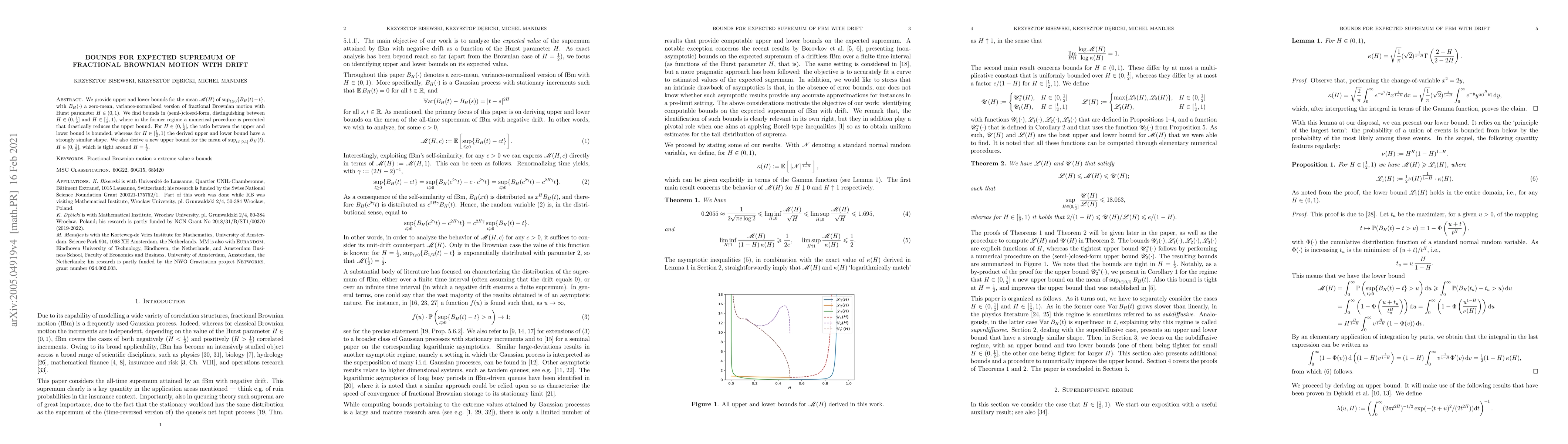

We provide upper and lower bounds for the mean ${\mathscr M}(H)$ of $\sup_{t\geqslant 0} \{B_H(t) - t\}$, with $B_H(\cdot)$ a zero-mean, variance-normalized version of fractional Brownian motion wit...