Academic Profile

Statistics

Similar Authors

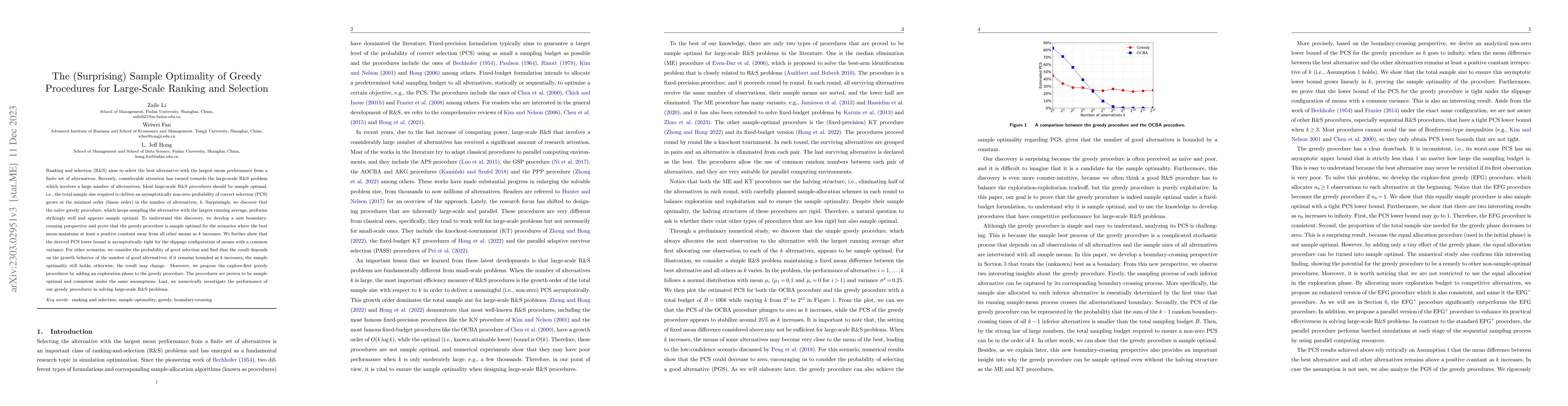

Papers on arXiv

Large-scale simulation optimization (SO) problems encompass both large-scale ranking-and-selection problems and high-dimensional discrete or continuous SO problems, presenting significant challenges...

The efficient management of large-scale queueing networks is critical for a variety of sectors, including healthcare, logistics, and customer service, where system performance has profound implicati...

We introduce AlphaRank, an artificial intelligence approach to address the fixed-budget ranking and selection (R&S) problems. We formulate the sequential sampling decision as a Markov decision proce...

Stochastic simulation models, while effective in capturing the dynamics of complex systems, are often too slow to run for real-time decision-making. Metamodeling techniques are widely used to learn ...

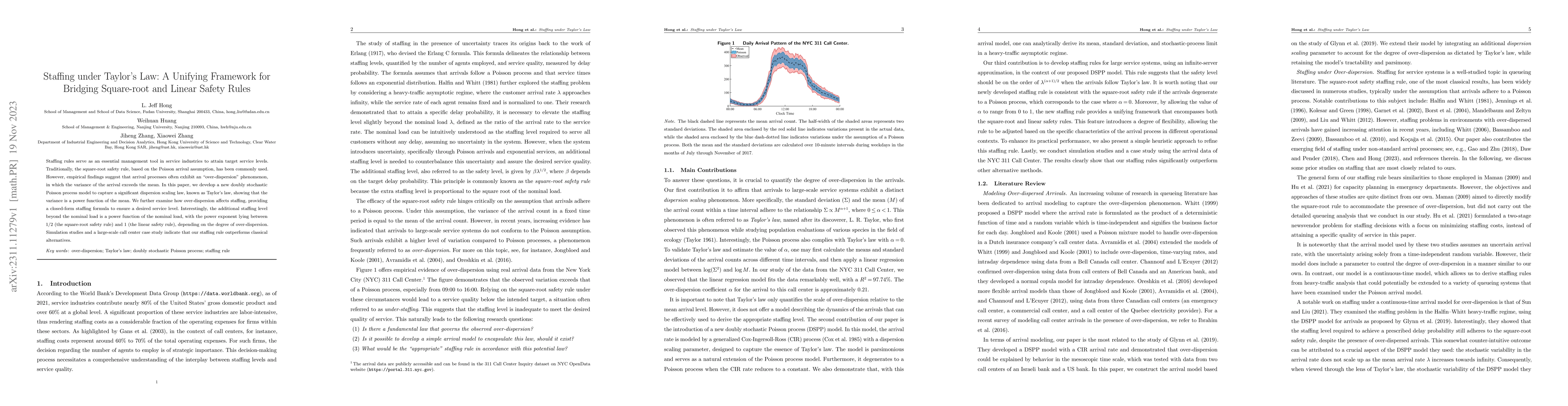

Staffing rules serve as an essential management tool in service industries to attain target service levels. Traditionally, the square-root safety rule, based on the Poisson arrival assumption, has b...

Ranking and selection (R&S) aims to select the best alternative with the largest mean performance from a finite set of alternatives. Recently, considerable attention has turned towards the large-sca...

${\rm CoVaR}$ is one of the most important measures of financial systemic risks. It is defined as the risk of a financial portfolio conditional on another financial portfolio being at risk. In this ...

Many large-scale production networks include thousands types of final products and tens to hundreds thousands types of raw materials and intermediate products. These networks face complicated invent...

Simulation models are widely used in practice to facilitate decision-making in a complex, dynamic and stochastic environment. But they are computationally expensive to execute and optimize, due to l...

We consider a contextual online learning (multi-armed bandit) problem with high-dimensional covariate $\mathbf{x}$ and decision $\mathbf{y}$. The reward function to learn, $f(\mathbf{x},\mathbf{y})$...

In this paper, we briefly review the development of ranking-and-selection (R&S) in the past 70 years, especially the theoretical achievements and practical applications in the last 20 years. Differe...

In contextual continuum-armed bandits, the contexts $x$ and the arms $y$ are both continuous and drawn from high-dimensional spaces. The payoff function to learn $f(x,y)$ does not have a particular ...

Knowledge gradient is a design principle for developing Bayesian sequential sampling policies to solve optimization problems. In this paper we consider the ranking and selection problem in the prese...

We consider a problem of ranking and selection via simulation in the context of personalized decision making, where the best alternative is not universal but varies as a function of some observable ...

Ranking and selection (R&S) conventionally aims to select the unique best alternative with the largest mean performance from a finite set of alternatives. However, for better supporting decision makin...

Robust ranking and selection (R&S) is an important and challenging variation of conventional R&S that seeks to select the best alternative among a finite set of alternatives. It captures the common in...

This paper addresses the estimation of the systemic risk measure known as CoVaR, which quantifies the risk of a financial portfolio conditional on another portfolio being at risk. We identify two prin...

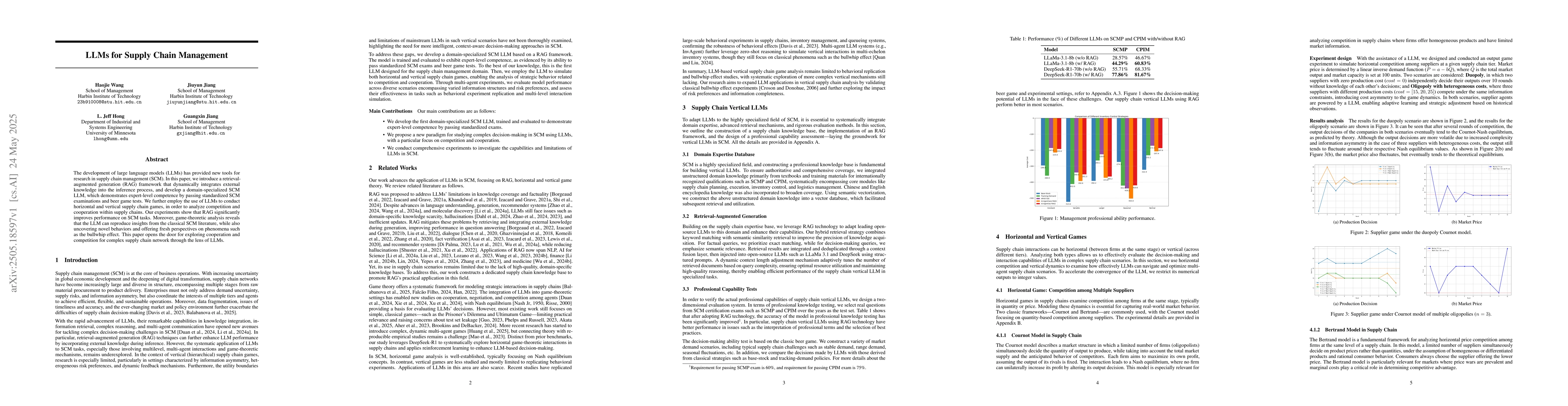

The development of large language models (LLMs) has provided new tools for research in supply chain management (SCM). In this paper, we introduce a retrieval-augmented generation (RAG) framework that ...

The rapid expansion of cross-border e-commerce (CBEC) has created significant opportunities for small and medium-sized enterprises (SMEs), yet financing remains a critical challenge due to SMEs' limit...

Ranking and selection (R&S) aims to identify the alternative with the best mean performance among $k$ simulated alternatives. The practical value of R&S depends on accurate simulation input modeling, ...

Selecting the best alternative from a finite set represents a broad class of pure exploration problems. Traditional approaches to pure exploration have predominantly relied on Gaussian or sub-Gaussian...

In this work, we study contextual strongly convex simulation optimization and adopt an "optimize then predict" (OTP) approach for real-time decision making. In the offline stage, simulation optimizati...

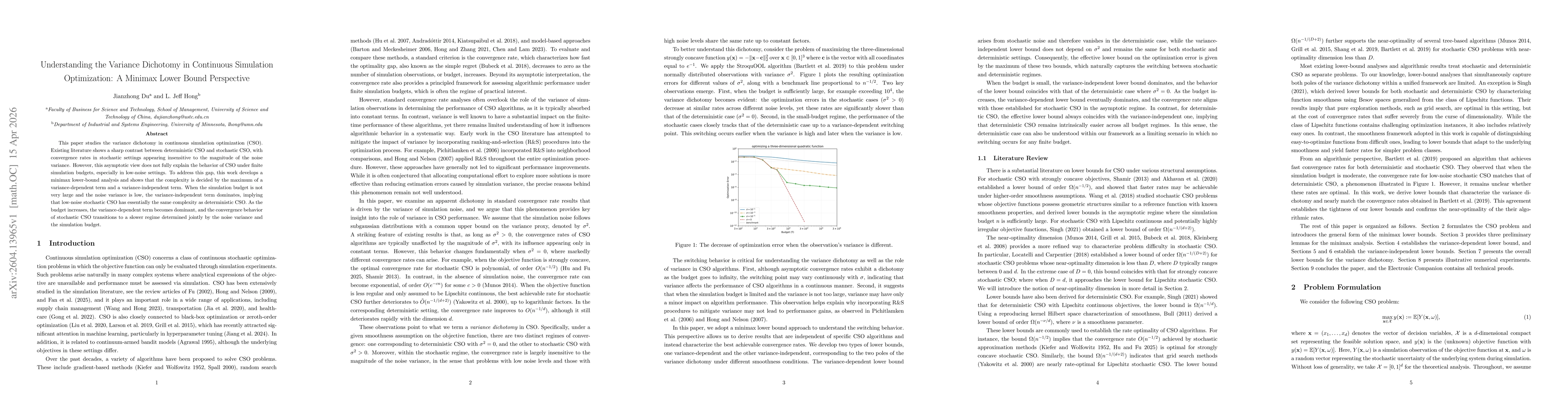

This paper studies the variance dichotomy in continuous simulation optimization (CSO). Existing literature shows a sharp contrast between deterministic CSO and stochastic CSO, with convergence rates i...