Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study periodic solutions to the following divergence-form stochastic partial differential equation with Wick-renormalized gradient on the $d$-dimensional flat torus $\mathbb{T}^d$, \[ -\nabla...

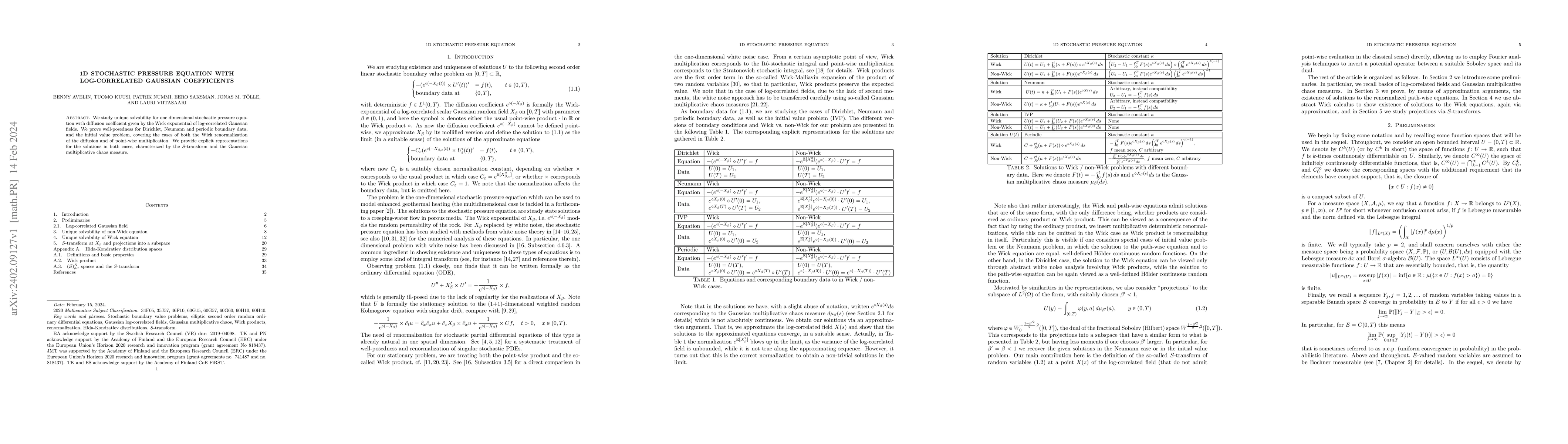

We study unique solvability for one dimensional stochastic pressure equation with diffusion coefficient given by the Wick exponential of log-correlated Gaussian fields. We prove well-posedness for D...

We prove the transfer principle for fractional Ornstein-Uhlenbeck processes, i.e., we construct a Brownian motion that has the same filtration as the fractional Ornstein-Uhlenbeck process and then r...

We consider equidistant Riemann approximations of stochastic integrals $\int_0^T f(B^H_s)dB^H_s$ with respect to the fractional Brownian motion with $H>\frac12$, where $f$ is an arbitrary function o...

Sample path properties of random processes are an interesting and extensively studied topic, especially in the case of Gaussian processes. In this article, we study the continuity properties of hype...

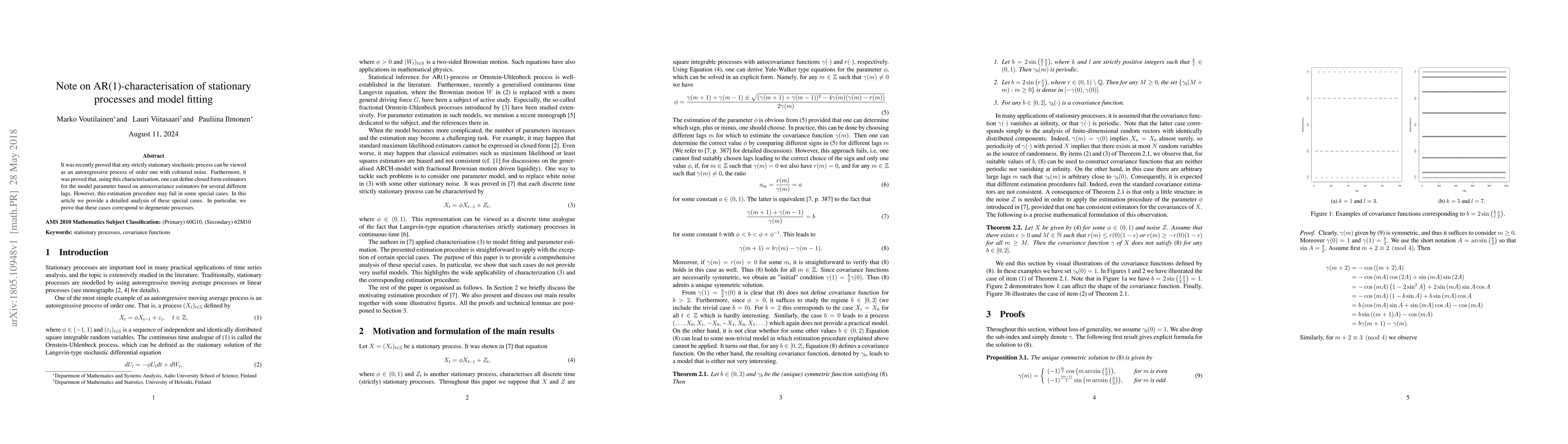

In this article we characterise discrete time stationary fields by difference equations involving stationary increment fields and self-similar fields. This gives connections between stationary field...

In this article we prove that estimator stability is enough to show that leave-one-out cross validation is a sound procedure, by providing concentration bounds in a general framework. In particular,...

We study the existence and regularity of local times for general $d$-dimensional stochastic processes. We give a general condition for their existence and regularity properties. To emphasize the con...

We consider equidistant approximations of stochastic integrals driven by H\"older continuous Gaussian processes of order $H>\frac12$ with discontinuous integrands involving bounded variation functio...

Breast cancer is the most common cancer among Western women. Fortunately, organized screening has reduced breast cancer mortality and, consequently, the European Union has recommended screening with...

This paper considers the problem of reconstructing missing parts of functions based on their observed segments. It provides, for Gaussian processes and arbitrary bijective transformations thereof, t...

In this paper we consider the mean transition time of an over-damped Brownian particle between local minima of a smooth potential. When the minima and saddles are non-degenerate this is in the low n...

In this article we study the asymptotic behaviour of the least square estimator in a linear regression model based on random observation instances. We provide mild assumptions on the moments and dep...

This paper develops a new integrated ball (pseudo)metric which provides an intermediary between a chosen starting (pseudo)metric d and the L_p distance in general function spaces. Selecting d as the...

We prove a result on the fractional Sobolev regularity of composition of paths of low fractional Sobolev regularity with functions of bounded variation. The result relies on the notion of variabilit...

In this article we consider existence and uniqueness of the solutions to a large class of stochastic partial differential of form $\partial_t u = L_x u + b(t,u)+\sigma(t,u)\dot{W}$, driven by a Gaus...

In this article we present a {\it quantitative} central limit theorem for the stochastic fractional heat equation driven by a a general Gaussian multiplicative noise, including the cases of space-ti...

Let $Z = (Z_t)_{t \geq 0}$ be the Rosenblatt process with Hurst index $H \in (1/2, 1)$. We prove joint continuity for the local time of $Z$, and establish H\"older conditions for the local time. The...

We define compositions $\varphi(X)$ of H\"older paths $X$ in $\mathbb{R}^n$ and functions of bounded variation $\varphi$ under a relative condition involving the path and the gradient measure of $\v...

We propose a novel strategy for multivariate extreme value index estimation. In applications such as finance, volatility and risk present in the components of a multivariate time series are often dr...

Generalisations of the Ornstein-Uhlenbeck process defined through Langevin equation $dU_t = - \Theta U_t dt + dG_t,$ such as fractional Ornstein-Uhlenbeck processes, have recently received a lot of ...

We study one-dimensional stochastic differential equations of form $dX_t = \sigma(X_t)dY_t$, where $Y$ is a suitable H\"older continuous driver such as the fractional Brownian motion $B^H$ with $H>\...

In this article we introduce and study oscillating Gaussian processes defined by $X_t = \alpha_+ Y_t {\bf 1}_{Y_t >0} + \alpha_- Y_t{\bf 1}_{Y_t<0}$, where $\alpha_+,\alpha_->0$ are free parameters ...

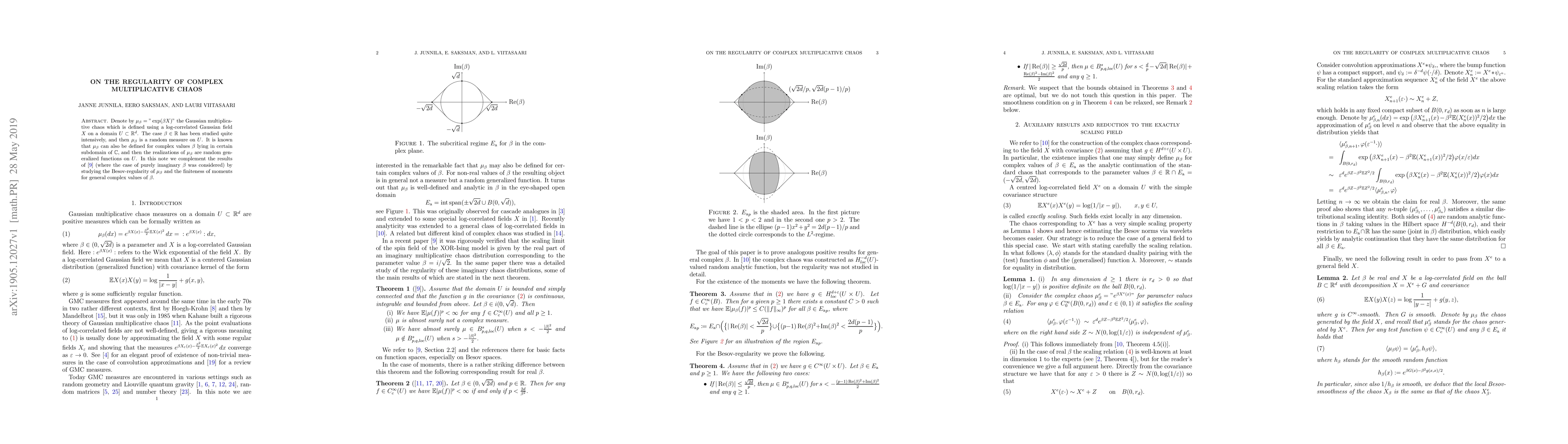

Denote by $\mu_\beta="\exp(\beta X)"$ the Gaussian multiplicative chaos which is defined using a log-correlated Gaussian field $X$ on a domain $U\subset\mathbb{R}^d$. The case $\beta\in\mathbb{R}$ h...

It was recently proved that any strictly stationary stochastic process can be viewed as an autoregressive process of order one with coloured noise. Furthermore, it was proved that, using this charac...

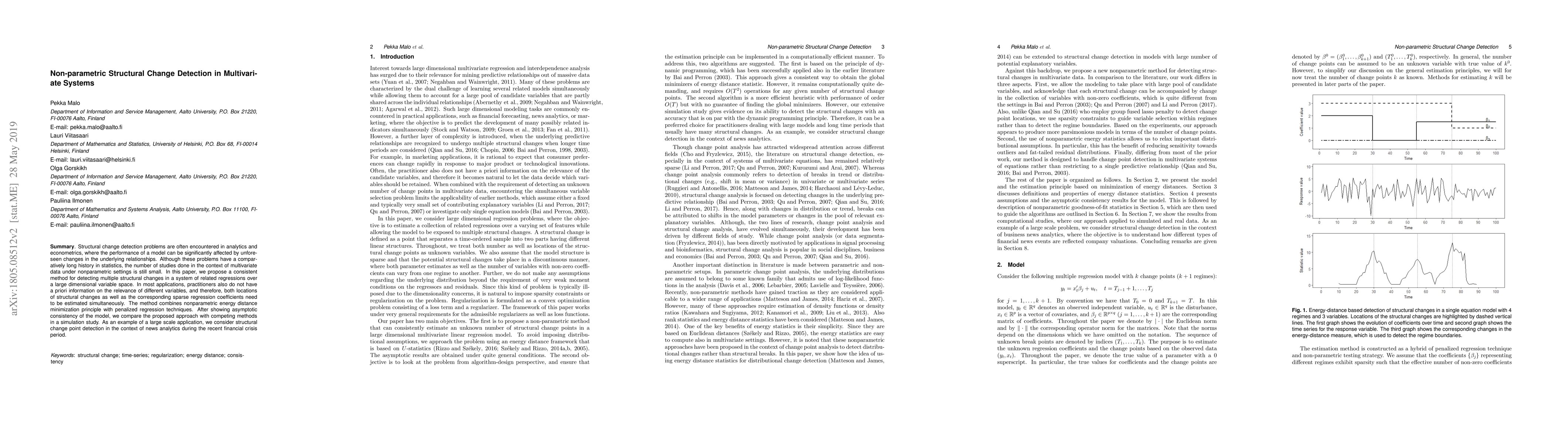

Structural change detection problems are often encountered in analytics and econometrics, where the performance of a model can be significantly affected by unforeseen changes in the underlying relat...

In this article, we show that a general class of weakly stationary time series can be modeled applying Gaussian subordinated processes. We show that, for any given weakly stationary time series $(z_...

This paper studies reinforcement learning (RL) in infinite-horizon dynamic decision processes with almost-sure safety constraints. Such safety-constrained decision processes are central to application...

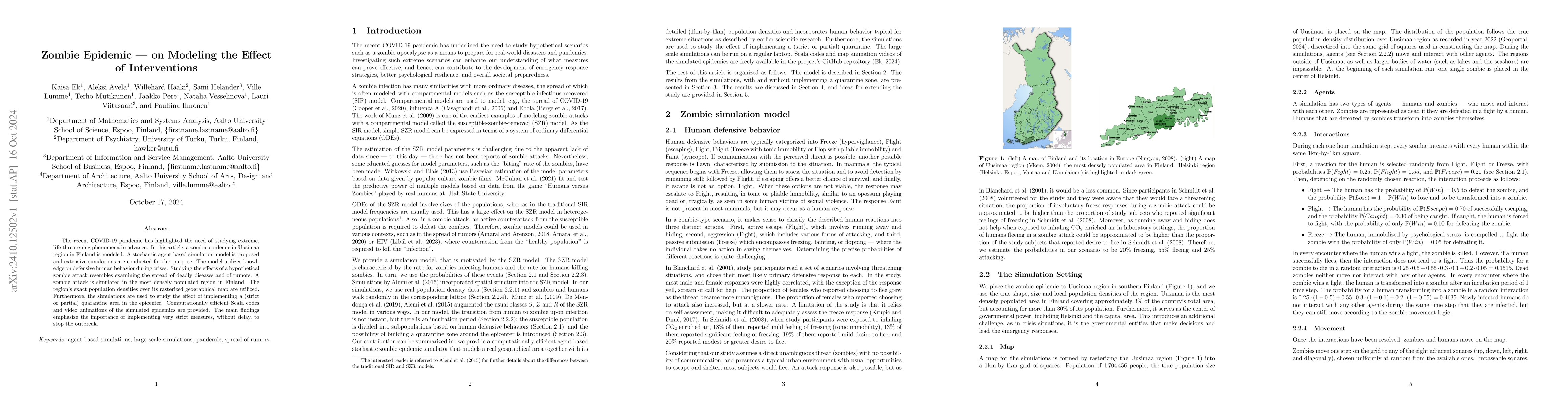

The recent COVID-19 pandemic has highlighted the need of studying extreme, life-threatening phenomena in advance. In this article, a zombie epidemic in Uusimaa region in Finland is modeled. A stochast...

We consider the projected normal distribution, with isotropic variance, on the 2-sphere using intrinsic statistics. We show that in this case, the expectation commutes with the projection and that the...

Within the context of rough path analysis via fractional calculus, we show how the notion of variability can be used to prove the existence of integrals with respect to H\"older continuous multiplicat...

In this article, we study the explosion time of the solution to autonomous stochastic differential equations driven by the fractional Brownian motion with Hurst parameter $H>1/2$. With the help of the...

The small noise cut-off phenomenon in continuous time and space has been studied in the recent literature for the linear and non-linear stable Langevin dynamics with additive L\'evy drivers - understo...

In many application areas of extreme value theory, the variables of interest are not directly observable but instead contain errors. In this article, we quantify the effect of these errors in moment-b...

We derive a Tanaka-type formula for the solution of a stochastic differential equation (SDE) driven by fractional Brownian motion (fBm) with Hurst parameter $H > \frac{1}{2}$. While Tanaka formulas fo...

The Vasicek model is a commonly used interest rate model, and there exist many extensions and generalizations of it. However, most generalizations of the model are either univariate or assume the nois...

In this article, we introduce a novel non-parametric predictor, based on conditional expectation, for the unknown diffusion coefficient function $\sigma$ in the stochastic partial differential equatio...

A generalisation of the extended Kalman filter for Stiefel manifold-valued measurements is presented. We provide simulations on the 2-sphere and the space of orthogonal 4-by-2 matrices which show sign...

In this paper we first introduce the setting of filtering on Stiefel manifolds. Then, assuming the underlying system process is constant, the convergence of the extended Kalman filter with Stiefel man...

In this article, we characterize continuous stationary fields via generalized Langevin dynamics. This gives natural connections between stationary fields, stationary increment fields, self-similar fie...

We consider four prototypes of variational problems and prove the existence of fractal minimizers through the direct method in the calculus of variations. By design these minimizers are Hölder curves ...

We prove that, under the Hörmander criterion on an Itô process, all its martingale observables are smooth. As a consequence, we also obtain a generalized Feynman-Kac formula providing smooth solutions...

This paper develops a framework for the error analysis in nonparametric model fitting of fractional stochastic differential equations based on discrete observations. We identify and quantify the main ...

We prove precise almost sure lower path regularity results for a wide class of stochastic processes in all space dimensions $d\geq 1$. Examples include Gaussian processes, in particular, fractional Br...

We investigate a generalized stochastic fractional neuronal model combining fractional dynamics with correlated stochastic inputs. The proposed framework is described by a fractional differential equa...

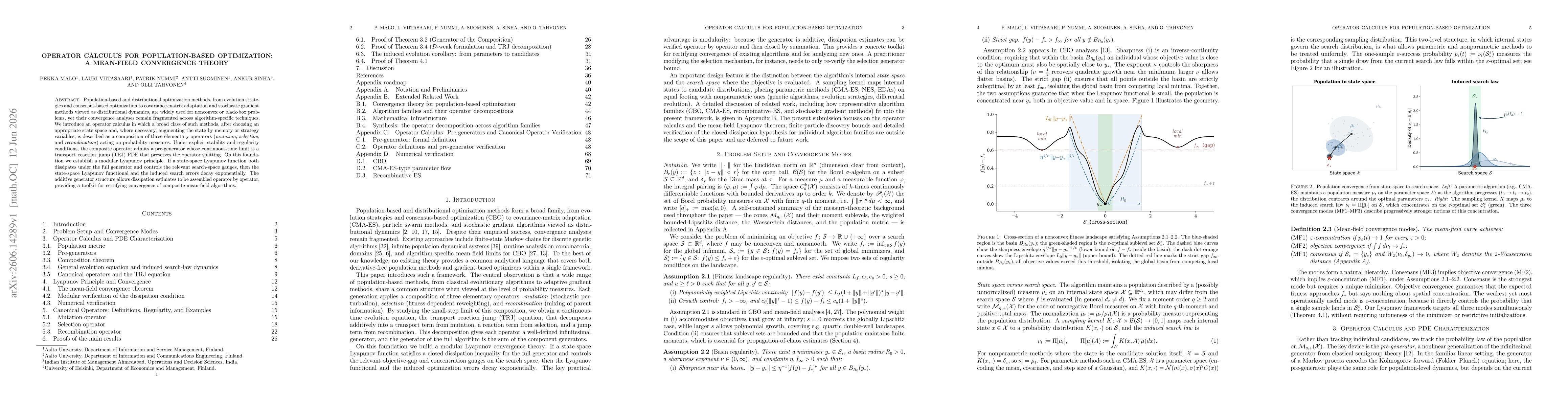

Population-based and distributional optimization methods, from evolution strategies and consensus-based optimization to covariance-matrix adaptation and stochastic gradient methods viewed as distribut...