Academic Profile

Statistics

Similar Authors

Papers on arXiv

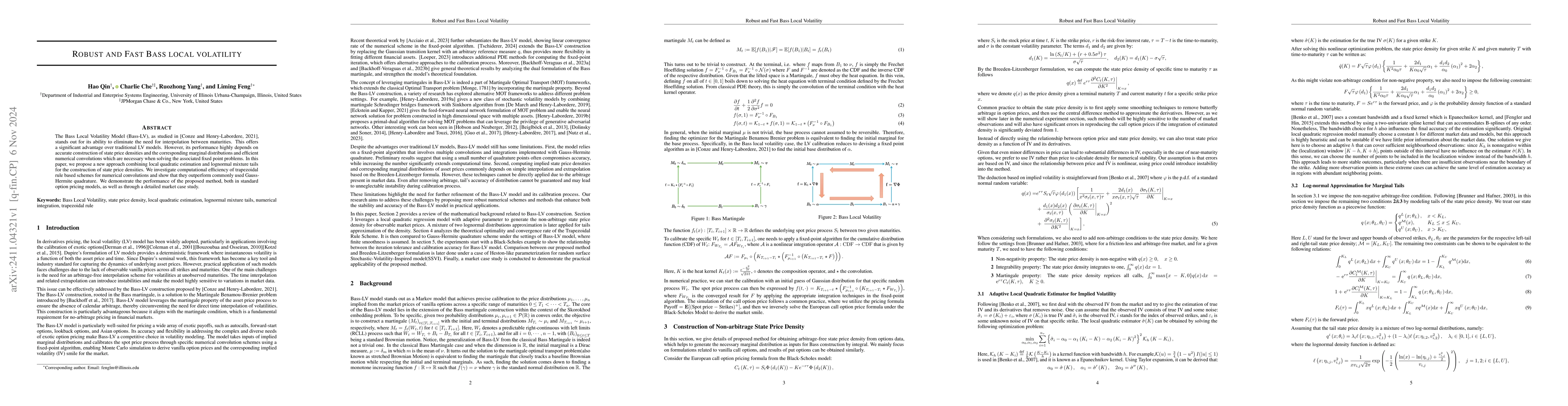

The Bass Local Volatility Model (Bass-LV), as studied in \citep{henry2021bass}, stands out for its ability to eliminate the need for interpolation between maturities. This offers a significant advanta...

Managing exotic derivatives requires accurate mark-to-market pricing and stable Greeks for reliable hedging. The Local Volatility (LV) model distinguishes itself from other pricing models by its abili...

Many quantitative finance methods and applications are formulated in terms of option-implied risk-neutral marginals rather than directly in terms of option prices. Representative examples include mart...