Academic Profile

Statistics

Similar Authors

Papers on arXiv

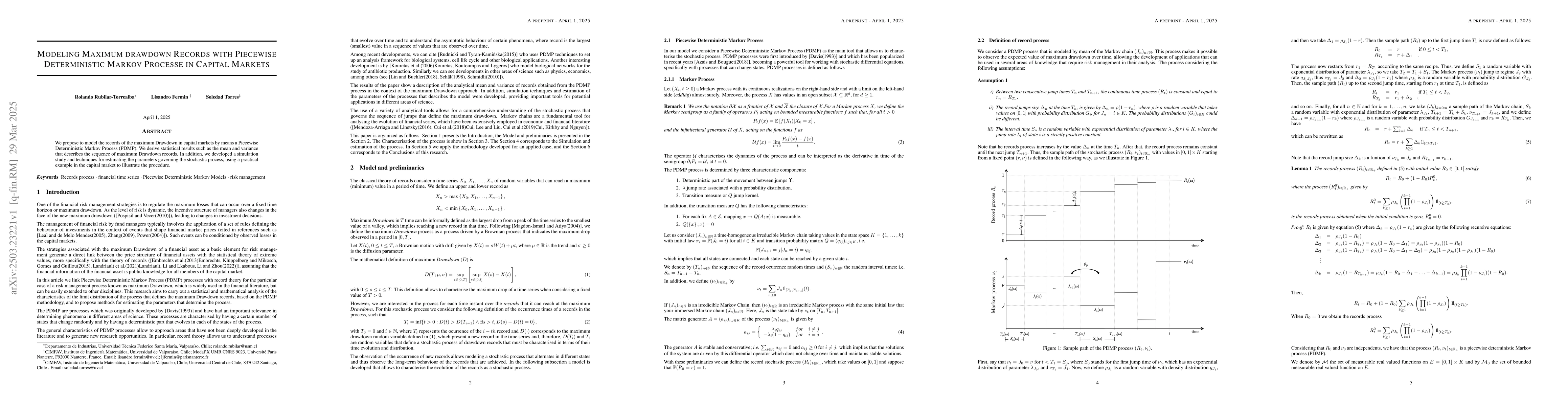

We propose to model the records of the maximum Drawdown in capital markets by means a Piecewise Deterministic Markov Process (PDMP). We derive statistical results such as the mean and variance that de...

This article is dedicated to the estimation of the regression function when the explanatory variable is a weakly dependent process whose correlation coefficient exhibits exponential decay and has a kn...

This paper is the second part of our study on the non-parametric estimation of MS-NAR processes started with [L. Fermin et al. 2017]. We consider the Nadaraya-Watson type regression function estimator...

We study a stochastic functional differential equation (SFDE) with memory driven by a fractional Brownian motion (fBm) with Hurst parameter H>1/2. An Euler-type numerical scheme is proposed and analyz...