Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider the Reinforcement Learning problem of controlling an unknown dynamical system to maximise the long-term average reward along a single trajectory. Most of the literature considers system ...

Motivated by the design of fast reinforcement learning algorithms, we study the diffusive limit of a class of pure jump ergodic stochastic control problems. We show that, whenever the intensity of j...

We consider the diffusive limit of a typical pure-jump Markovian control problem as the intensity of the driving Poisson process tends to infinity. We show that the convergence speed is provided by ...

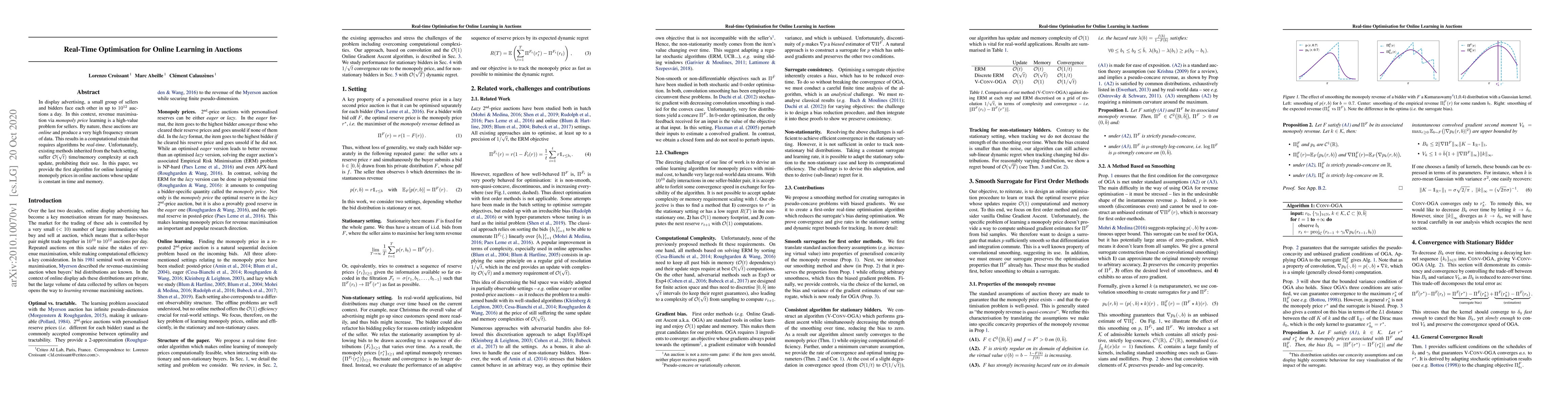

In display advertising, a small group of sellers and bidders face each other in up to 10 12 auctions a day. In this context, revenue maximisation via monopoly price learning is a high-value problem ...

Despite the impressive progress in statistical Optimal Transport (OT) in recent years, there has been little interest in the study of the \emph{sequential learning} of OT. Surprisingly so, as this pro...

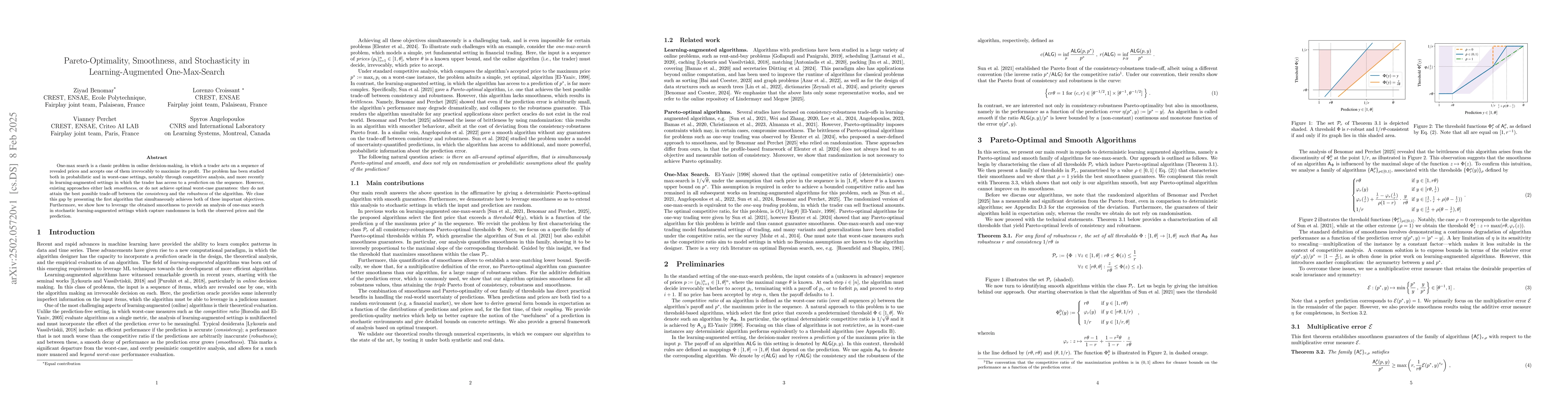

One-max search is a classic problem in online decision-making, in which a trader acts on a sequence of revealed prices and accepts one of them irrevocably to maximise its profit. The problem has been ...