Academic Profile

Statistics

Similar Authors

Papers on arXiv

The aim of this paper is to discuss an estimation and a simulation method in the \textsf{R} package YUIMA for a linear regression model driven by a Student-$t$ L\'evy process with constant scale and...

This paper presents an algorithm for the simulation of Hawkes-type processes where the intensity is expressed in terms of a continuous-time autoregressive moving average model. We identify upper bou...

The paper investigates the effect of the label green in bond markets from the lens of the trading activity. The idea is that jumps in the dynamics of returns have a specific memory nature that can b...

In this paper we introduce a new model named CARMA(p,q)-Hawkes process as the Hawkes model with exponential kernel implies a strictly decreasing behaviour of the autocorrelation function and empiric...

In this study, we propose a new formula for spread option pricing with the dependence of two assets described by a copula function. The advantage of the proposed method is that it requires only the ...

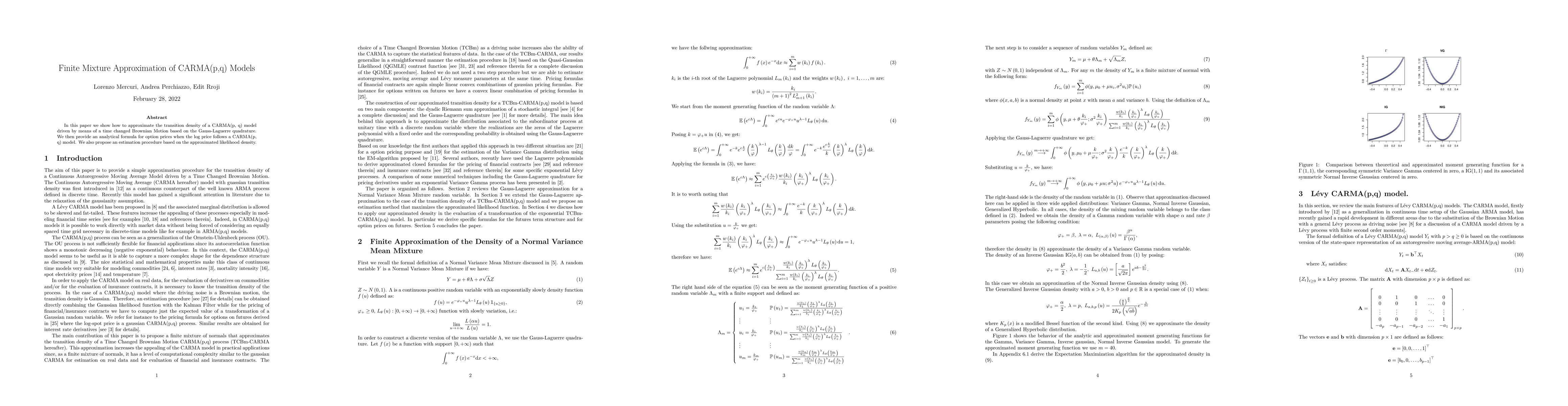

In this paper we show how to approximate the transition density of a CARMA(p, q) model driven by means of a time changed Brownian Motion based on the Gauss-Laguerre quadrature. We then provide an an...

A self-exciting point process with a continuous-time autoregressive moving average intensity process, named CARMA(p,q)-Hawkes model, has recently been introduced. The model generalizes the Hawkes proc...

This paper introduces a new market-implied object, Time to Transition (TtT), extracted from the difference between two selected nodes of the greenium term structure. TtT is defined as the latent waiti...