Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we present a probabilistic numerical algorithm combining dynamic programming, Monte Carlo simulations and local basis regressions to solve non-stationary optimal multiple switching pr...

Coarse correlated equilibria (CCE) are a good alternative to Nash equilibria (NE), as they arise more naturally as outcomes of learning algorithms and they may exhibit higher payoffs than NE. CCEs i...

In the framework of continuous time symmetric stochastic differential games in open loop strategies, we introduce a generalization of mean field game solution, called coarse correlated solution. Thi...

In a discrete space and time framework, we study the mean field game limit for a class of symmetric $N$-player games based on the notion of correlated equilibrium. We give a definition of correlated...

We propose a model where a producer and a consumer can affect the price dynamics of some commodity controlling drift and volatility of, respectively, the production rate and the consumption rate. We...

We consider a mean field game describing the limit of a stochastic differential game of $N$-players whose state dynamics are subject to idiosyncratic and common noise and that can be absorbed when t...

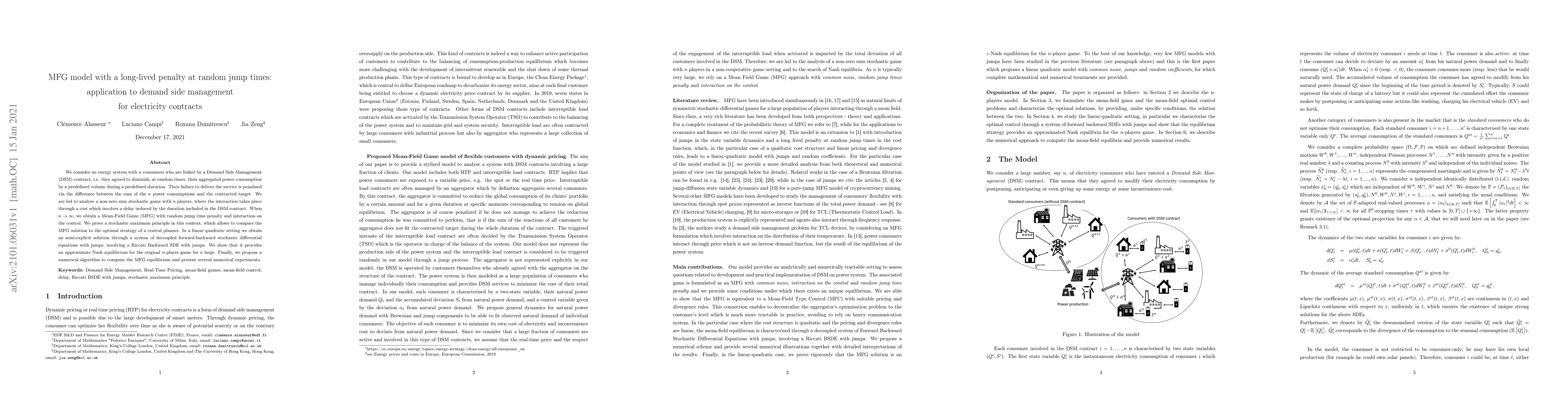

We consider an energy system with $n$ consumers who are linked by a Demand Side Management (DSM) contract, i.e. they agreed to diminish, at random times, their aggregated power consumption by a pred...

We study a new kind of non-zero-sum stochastic differential game with mixed impulse/switching controls, motivated by strategic competition in commodity markets. A representative upstream firm produc...

We study Nash equilibria for a sequence of symmetric $N$-player stochastic games of finite-fuel capacity expansion with singular controls and their mean-field game (MFG) counterpart. We construct a ...

In the context of simple finite-state discrete time systems, we introduce a generalization of mean field game solution, called correlated solution, which can be seen as the mean field game analogue ...

We design three continuous--time models in finite horizon of a commodity price, whose dynamics can be affected by the actions of a representative risk--neutral producer and a representative risk--ne...

Mean-field games with absorption is a class of games, that have been introduced in Campi and Fischer (2018) and that can be viewed as natural limits of symmetric stochastic differential games with a...

Starting from the Avellaneda-Stoikov framework, we consider a market maker who wants to optimally set bid/ask quotes over a finite time horizon, to maximize her expected utility. The intensities of ...

We frame dynamic persuasion in a partial observation stochastic control Leader-Follower game with an ergodic criterion. The Receiver controls the dynamics of a multidimensional unobserved state proces...

We propose a mean field game (MFG) framework to model the evolution of renewable energy production in competitive electricity markets. Producers interact through the spot price while optimising their ...

We study a mean field game (MFG) of state and control with state dynamics described by stochastic differential equations driven by both idiosyncratic and common noise, and subject to the constraint th...

We introduce optimal coarse correlated equilibria for continuous-time mean field games. A coarse correlated equilibrium is a randomized recommendation scheme from which no player can gain by ignoring ...