Academic Profile

Statistics

Similar Authors

Papers on arXiv

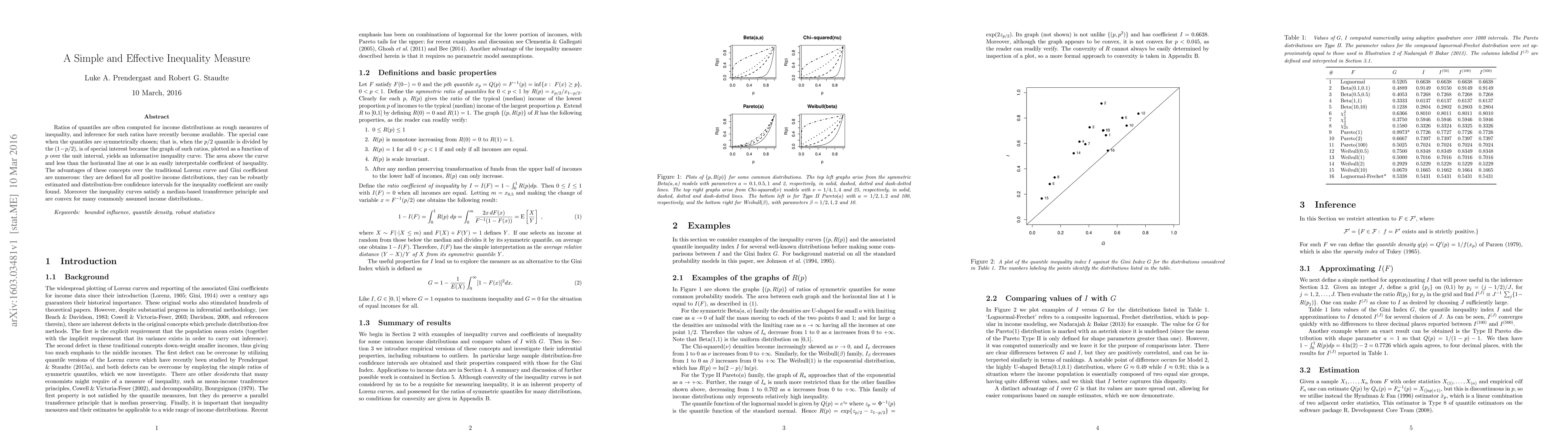

Ratios of quantiles are often computed for income distributions as rough measures of inequality, and inference for such ratios have recently become available. The special case when the quantiles are...

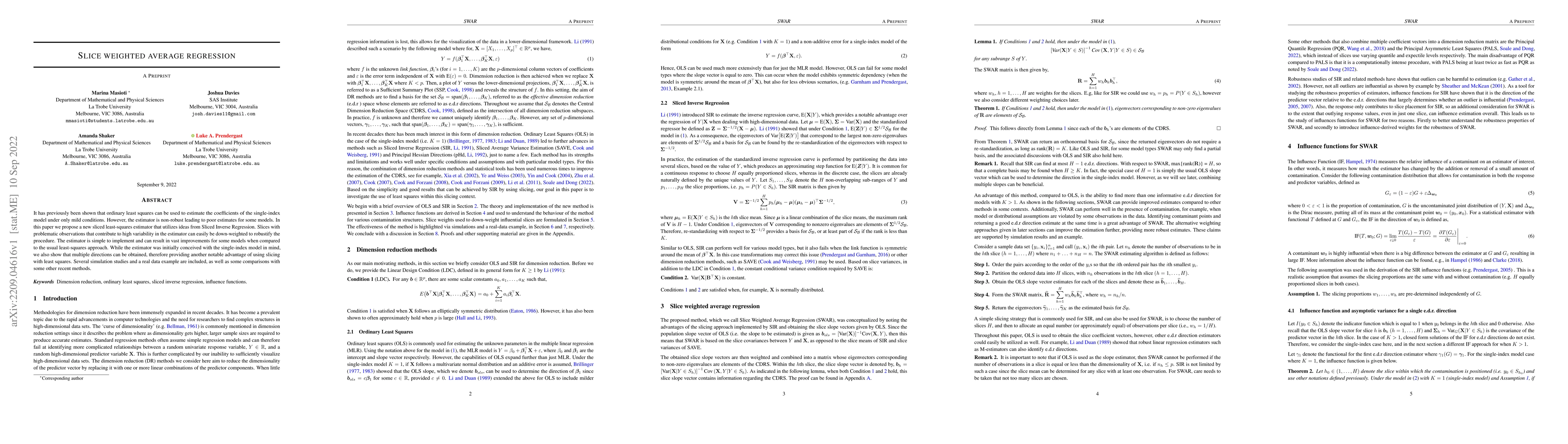

It has previously been shown that ordinary least squares can be used to estimate the coefficients of the single-index model under only mild conditions. However, the estimator is non-robust leading t...

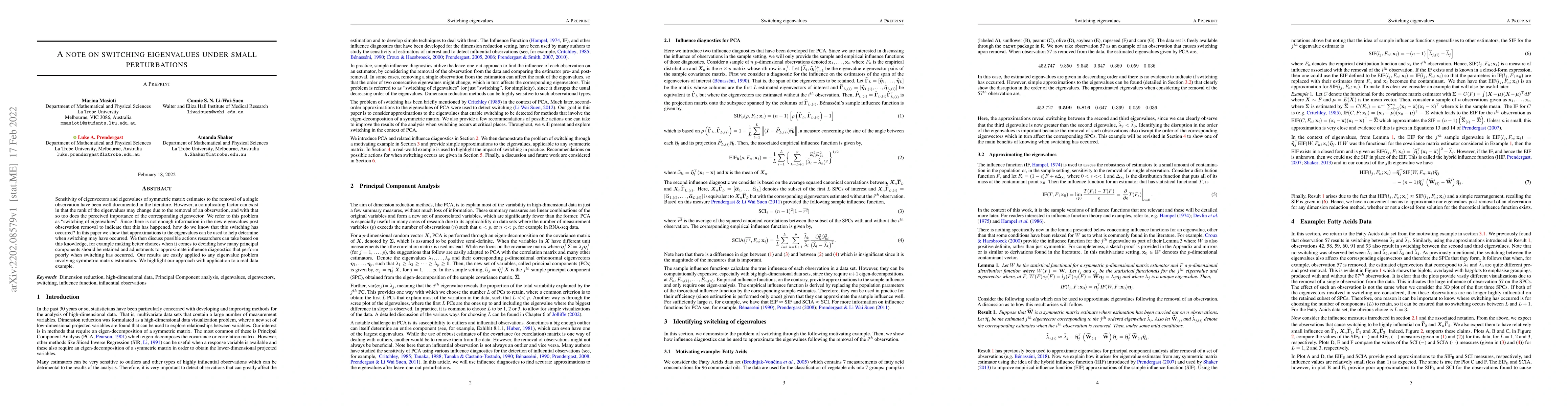

Sensitivity of eigenvectors and eigenvalues of symmetric matrix estimates to the removal of a single observation have been well documented in the literature. However, a complicating factor can exist...

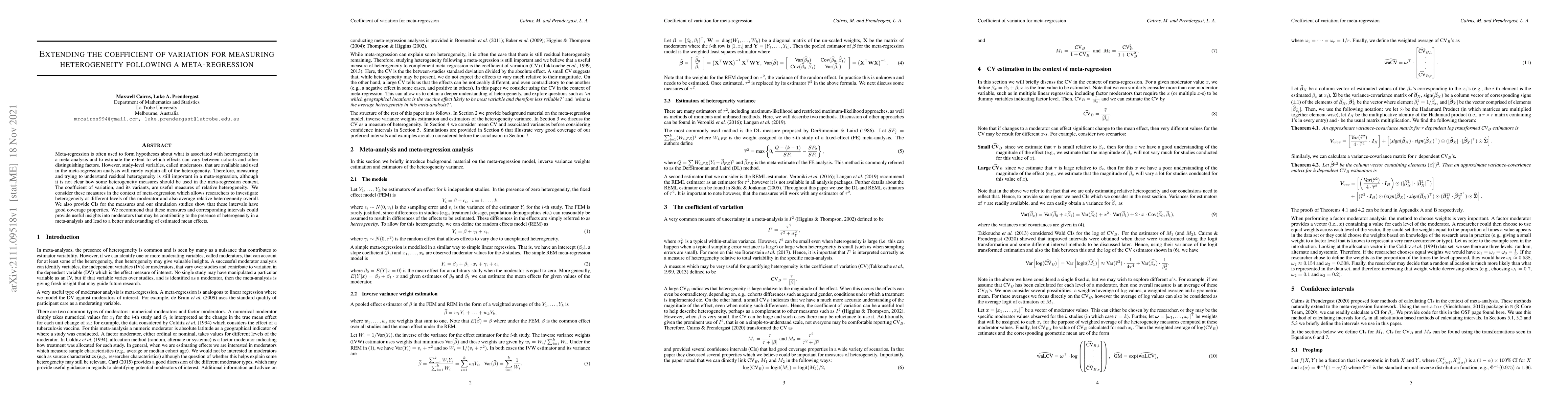

Meta-regression is often used to form hypotheses about what is associated with heterogeneity in a meta-analysis and to estimate the extent to which effects can vary between cohorts and other disting...

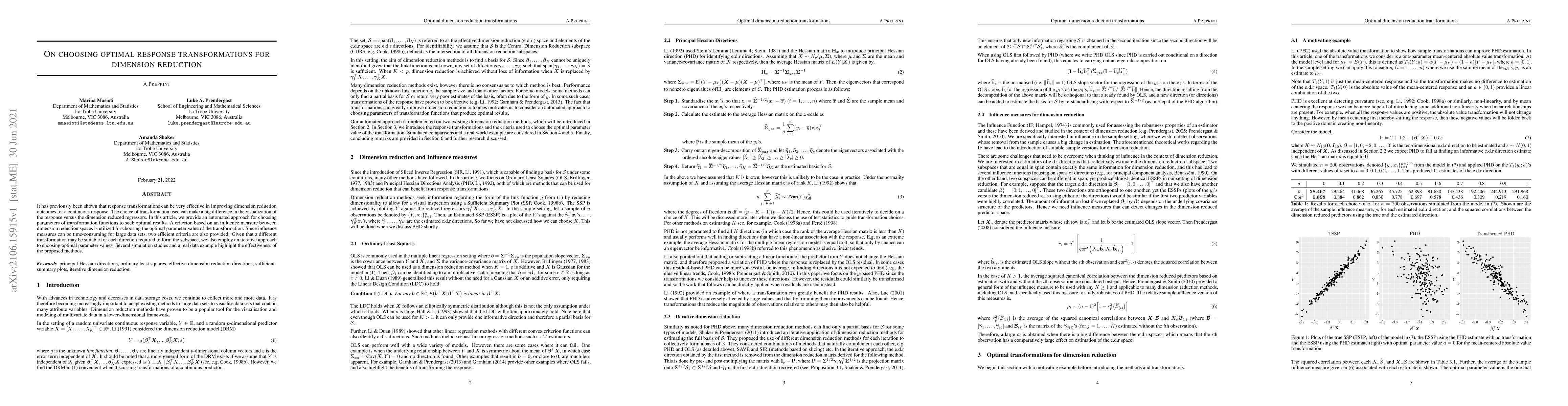

It has previously been shown that response transformations can be very effective in improving dimension reduction outcomes for a continuous response. The choice of transformation used can make a big...

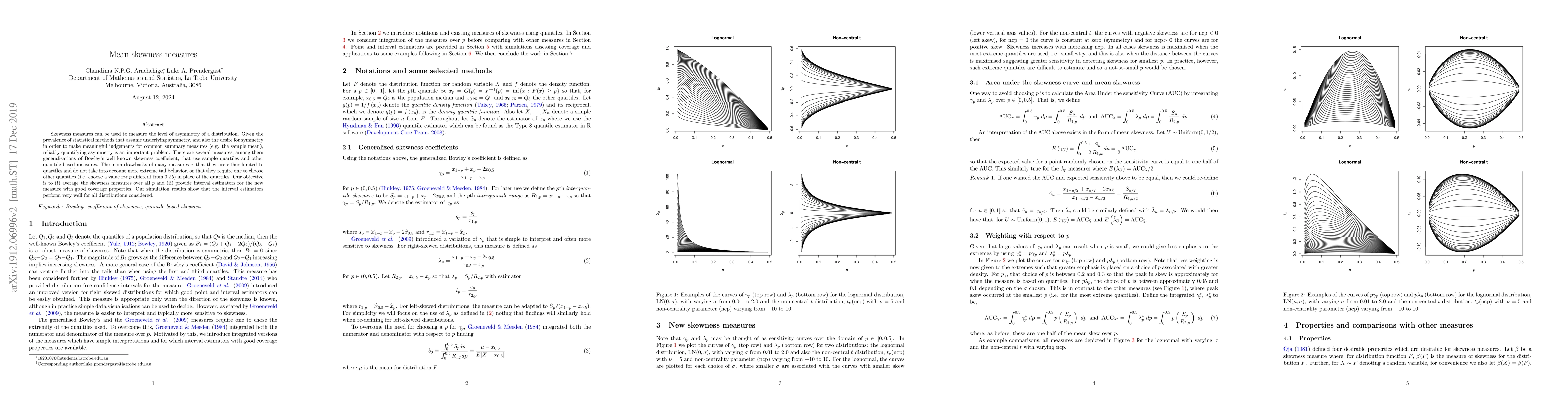

Skewness measures can be used to measure the level of asymmetry of a distribution. Given the prevalence of statistical methods that assume underlying symmetry, and also the desire for symmetry in or...

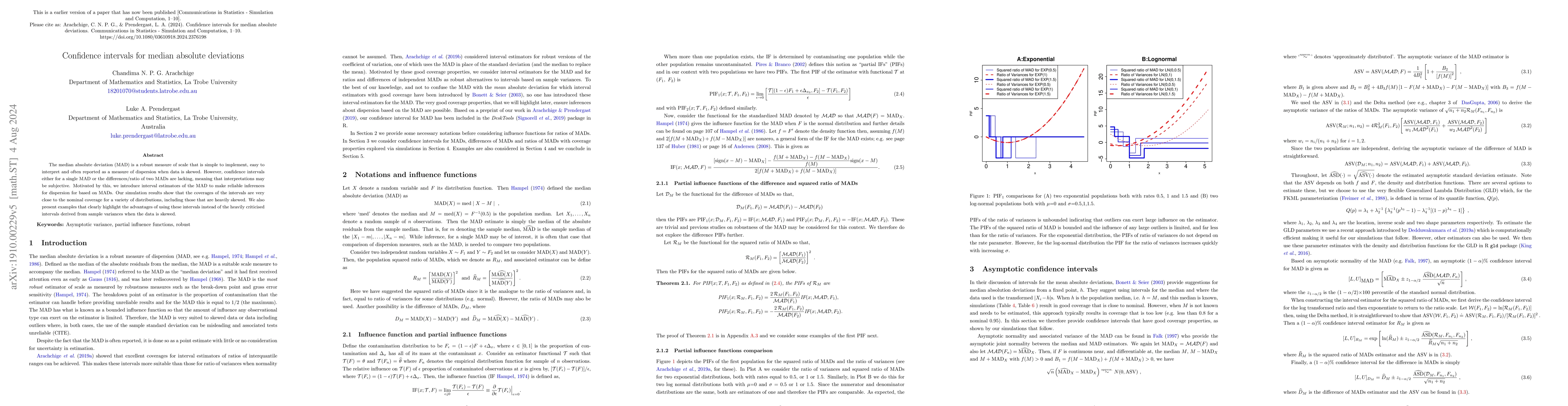

The median absolute deviation (MAD) is a robust measure of scale that is simple to implement and easy to interpret. Motivated by this, we introduce interval estimators of the MAD to make reliable in...

Whilst influence functions for linear discriminant analysis (LDA) have been found for a single discriminant when dealing with two groups, until now these have not been derived in the setting of a ge...

Income inequality measures are often used as an indication of economic health. How to obtain reliable confidence intervals for these measures based on sampled data has been studied extensively in re...

The coefficient of variation (CV) is commonly used to measure relative dispersion. However, since it is based on the sample mean and standard deviation, outliers can adversely affect the CV. Additio...

Sample quantiles, such as the median, are often better suited than the sample mean for summarising location characteristics of a data set. Similarly, linear combinations of sample quantiles and ratios...

In recent years, there has been much progress toward the development of methods for converting three- and five-number summary statistics (i.e. minimum, maximum, median, and quartiles) to means and sta...