Academic Profile

Statistics

Similar Authors

Papers on arXiv

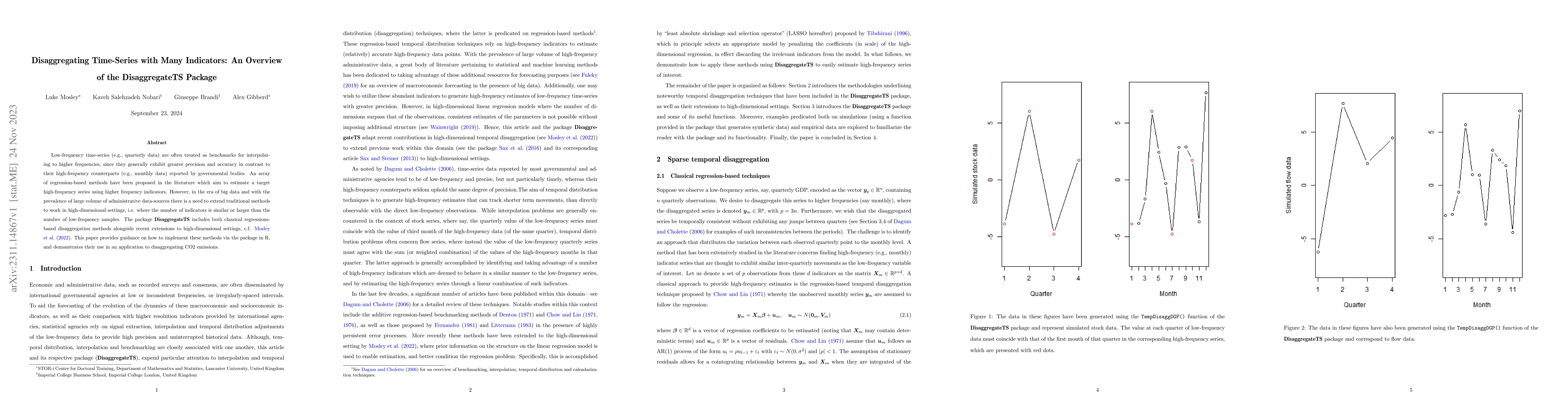

Low-frequency time-series (e.g., quarterly data) are often treated as benchmarks for interpolating to higher frequencies, since they generally exhibit greater precision and accuracy in contrast to t...

sparseDFM is an R package for the implementation of popular estimation methods for dynamic factor models (DFMs) including the novel Sparse DFM approach of Mosley et al. (2023). The Sparse DFM amelio...

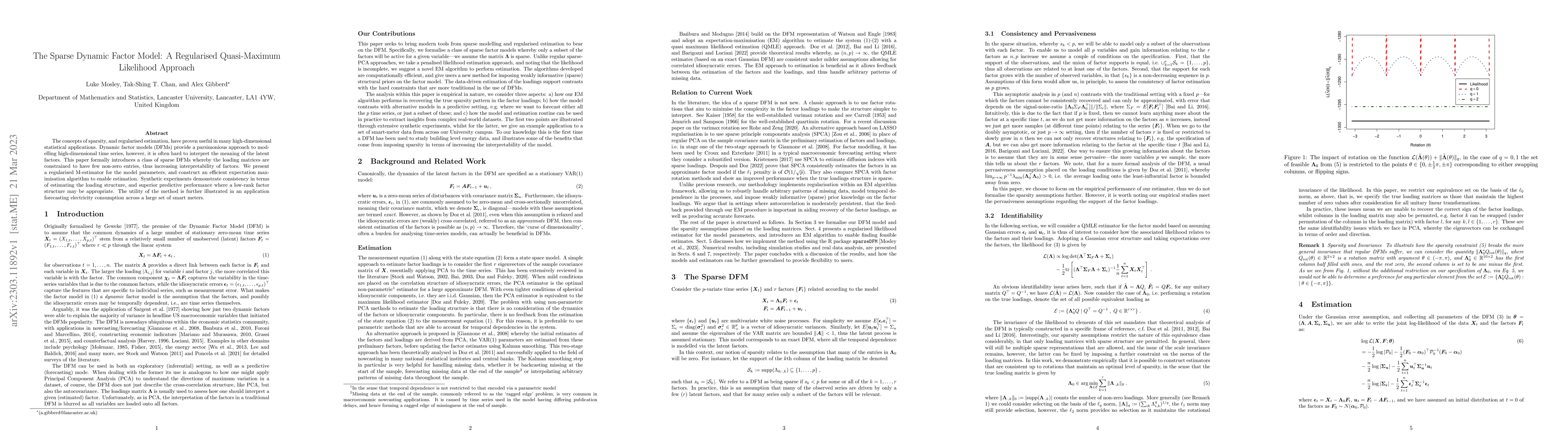

The concepts of sparsity, and regularised estimation, have proven useful in many high-dimensional statistical applications. Dynamic factor models (DFMs) provide a parsimonious approach to modelling ...

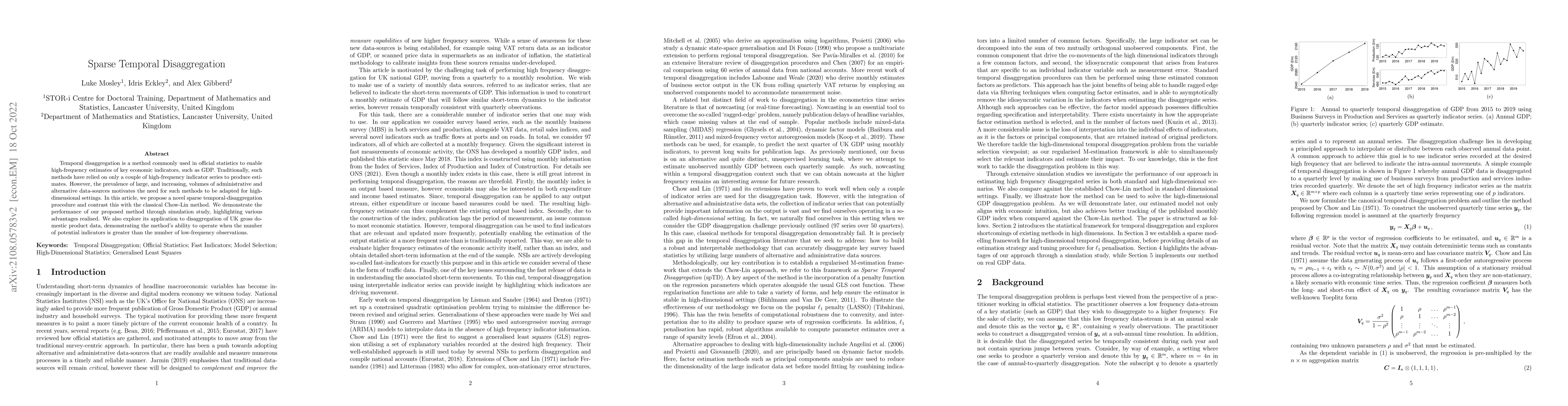

Temporal disaggregation is a method commonly used in official statistics to enable high-frequency estimates of key economic indicators, such as GDP. Traditionally, such methods have relied on only a...