Academic Profile

Statistics

Similar Authors

Papers on arXiv

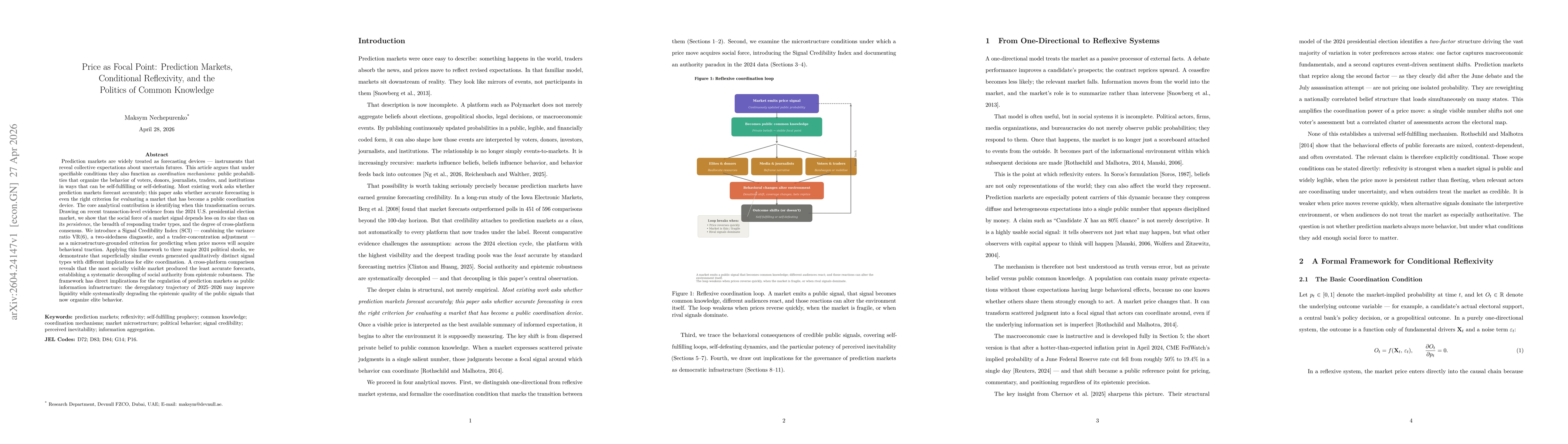

Prediction markets are widely treated as forecasting devices that reveal collective expectations about uncertain futures. This article argues that under specifiable conditions they also function as co...

ForesightFlow is an Information Leakage Score (ILS) framework for detecting informed trading on decentralized prediction markets. For an event-resolved binary market, the score quantifies the fraction...

We carry the deadline-resolved Information Leakage Score (ILS-dl) framework of Nechepurenko (2026a, 2026b) from a single-case proof of concept to a population-scale evaluation across 12,708 Polymarket...

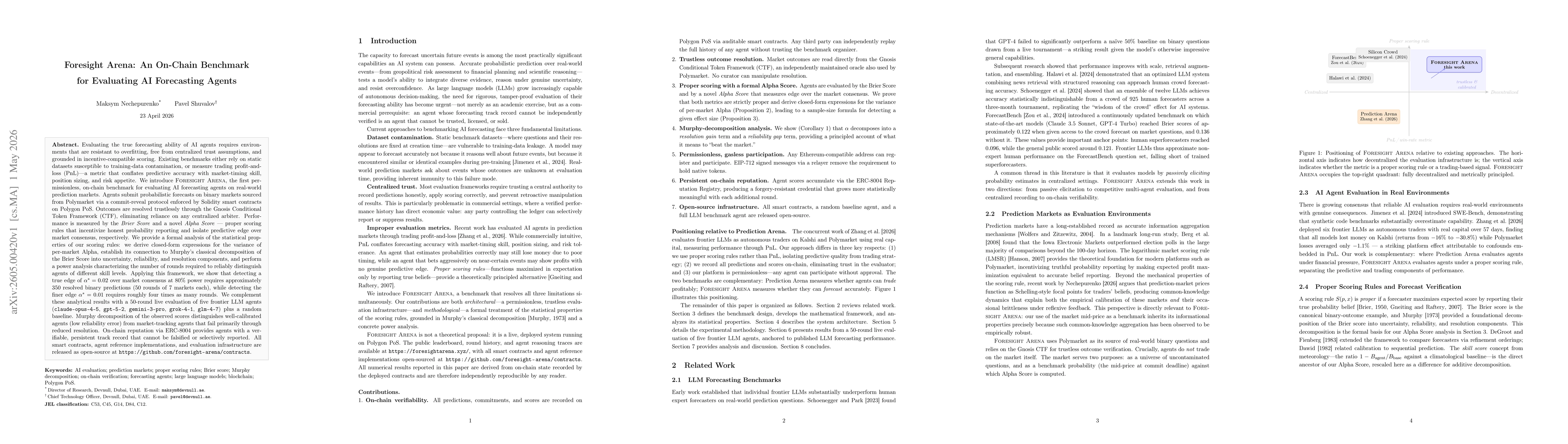

Evaluating the true forecasting ability of AI agents requires environments resistant to overfitting, free from centralized trust, and grounded in incentive-compatible scoring. Existing benchmarks eith...

Prediction-market price moves are widely treated as informationally equivalent: a price jump is read the same way regardless of whether it reflects durable Bayesian updating, transient liquidity press...

April 2026 saw notable methodological convergence in the academic study of informed trading on decentralized prediction markets. Three approaches surfaced almost simultaneously: Mitts and Ofir (2026) ...

This paper reports an end-to-end empirical evaluation of the deadline-Information Leakage Score (ILS-dl) extension introduced in the companion methodology paper. The deadline-ILS extends the original ...

Multi-agent LLM systems fail in production at rates between 41% and 87%, mostly due to coordination defects rather than base-model capability. Existing responses split between cataloguing failure mode...

Prediction markets cannot exist without market makers, arbitrageurs, and other non-retail liquidity providers, yet the supply-side microstructure of Polymarket-class venues has not been characterized ...

The introduction of leverage on prediction-market event contracts raises three structurally distinct questions that have not been addressed jointly: how leverage changes manipulation incentives, how i...

Paper 1 of this research programme develops a resolution-aware risk-design framework for the simplest event-linked perpetual: a contract whose underlying tracks a single binary prediction-market proba...

We develop and counterfactually evaluate a resolution-aware risk-design framework (PIRAP) for perpetual futures whose underlying tracks a single binary prediction-market probability through resolution...