Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study a planar random motion $\big(X(t),Y(t)\big)$ with orthogonal directions which can turn clockwise, counterclockwise and reverse its direction each with a different probability. The support o...

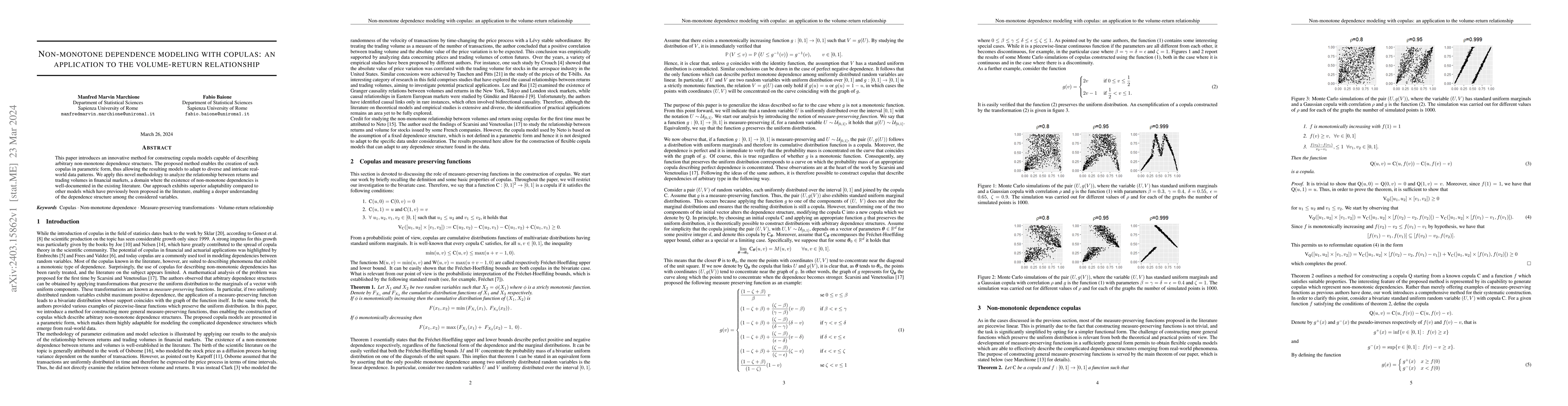

This paper introduces an innovative method for constructing copula models capable of describing arbitrary non-monotone dependence structures. The proposed method enables the creation of such copulas...

This paper introduces $\textbf{gemact}$, a $\textbf{Python}$ package for actuarial modelling based on the collective risk model. The library supports applications to risk costing and risk transfer, ...

In this paper we study Fresnel pseudoprocesses whose signed measure density is a solution to a higher-order extension of the equation of vibrations of rods. We also investigate space-fractional exte...

In this paper we study pseudo-processes related to odd-order heat-type equations composed with L\'evy stable subordinators. The aim of the article is twofold. We first show that the pseudo-density o...

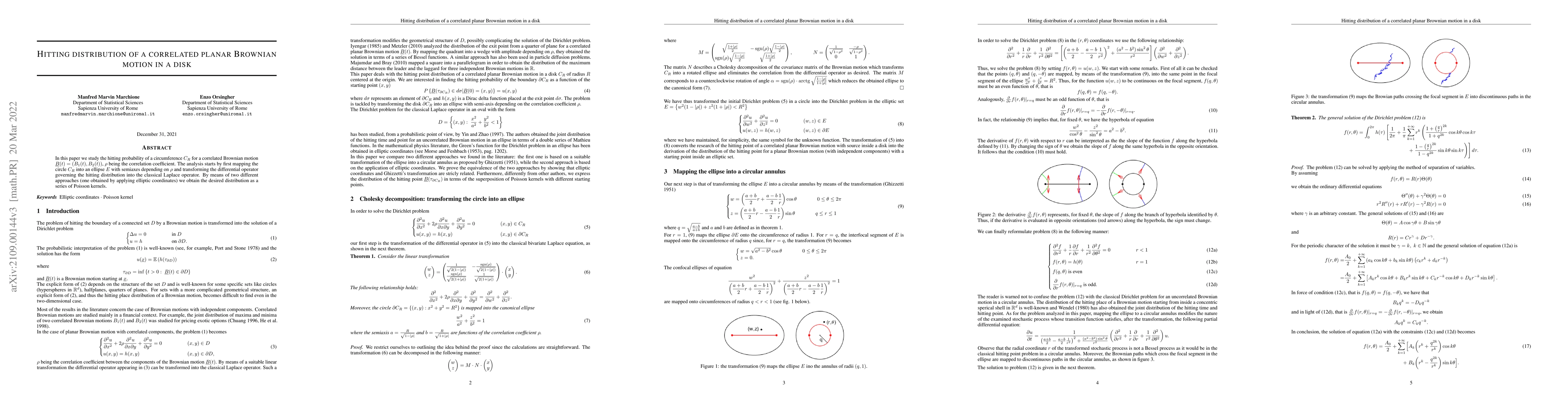

In this paper we study the hitting probability of a circumference $C_R$ for a correlated Brownian motion $\underline{B}(t)=\left(B_1(t), B_2(t)\right)$, $\rho$ being the correlation coefficient. The...

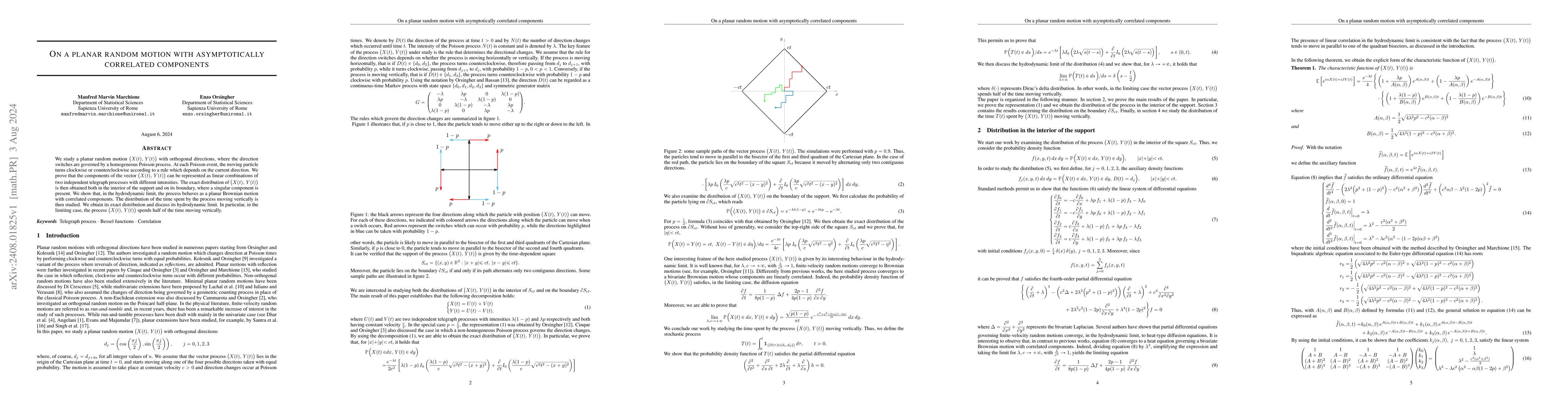

We study a planar random motion $\big(X(t),\,Y(t)\big)$ with orthogonal directions, where the direction switches are governed by a homogeneous Poisson process. At each Poisson event, the moving partic...

In this paper, we study univariate and planar random motions with variable propagation speeds. We first consider motions with space-varying velocity, which can be reduced to constant-velocity motions ...

In this paper, we study boundary-value problems describing the exit distribution of finite-velocity random motions from prescribed domains. For the standard telegraph process, with and without drift, ...