Academic Profile

Statistics

Similar Authors

Papers on arXiv

A goodness-of-fit test for the Functional Linear Model with Scalar Response (FLMSR) with responses Missing at Random (MAR) is proposed in this paper. The test statistic relies on a marked empirical ...

Diffusion models play an essential role in modeling continuous-time stochastic processes in the financial field. Therefore, several proposals have been developed in the last decades to test the spec...

Given the importance of continuous-time stochastic volatility models to describe the dynamics of interest rates, we propose a goodness-of-fit test for the parametric form of the drift and diffusion ...

Novel significance tests are proposed for the quite general additive concurrent model formulation without the need of model, error structure preliminary estimation or the use of tuning parameters. M...

This paper proposes a new nonlinear approach for additive functional regression with functional response based on kernel methods along with some slight reformulation and implementation of the linear...

This paper proposes a classification model for predicting the main activity of bitcoin addresses based on their balances. Since the balances are functions of time, we apply methods from functional d...

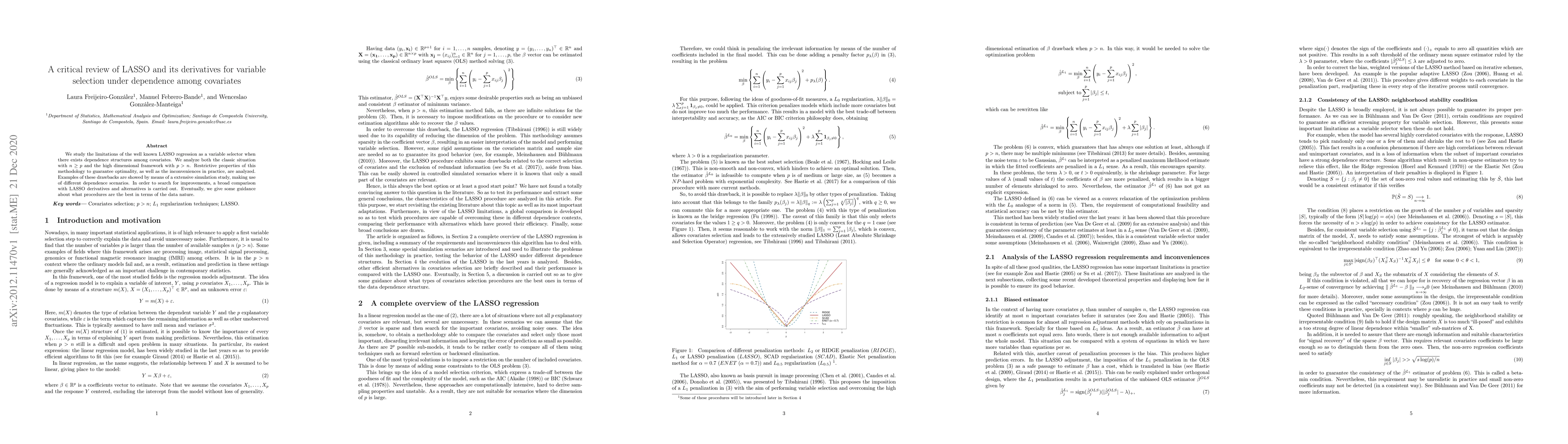

We study the limitations of the well known LASSO regression as a variable selector when there exists dependence structures among covariates. We analyze both the classic situation with $n\geq p$ and ...

It is well known that nonparametric regression estimation and inference procedures are subject to the curse of dimensionality. Moreover, model interpretability usually decreases with the data dimensio...

In a multivariate linear regression model with $p>1$ covariates, implementation of penalization techniques often implies a preliminary univariate standardization step. Although this prevents scale eff...

We provide a unified framework for independence and mean independence tests based on the Hilbert-Schmidt independence criterion, extending some previous results in the literature to hold in general to...