Marcelo C. Medeiros

The University of Illinois at Urbana-Champaign

Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper examines the effectiveness of several forecasting methods for predicting inflation, focusing on aggregating disaggregated forecasts - also known in the literature as the bottom-up approac...

We propose a model to forecast large realized covariance matrices of returns, applying it to the constituents of the S\&P 500 daily. To address the curse of dimensionality, we decompose the return c...

In this paper we examine the relation between market returns and volatility measures through machine learning methods in a high-frequency environment. We implement a minute-by-minute rolling window ...

This paper has the goal of evaluating how changes in mobility has affected the infection spread of Covid-19 throughout the 2020-2021 years. However, identifying a "clean" causal relation is not an e...

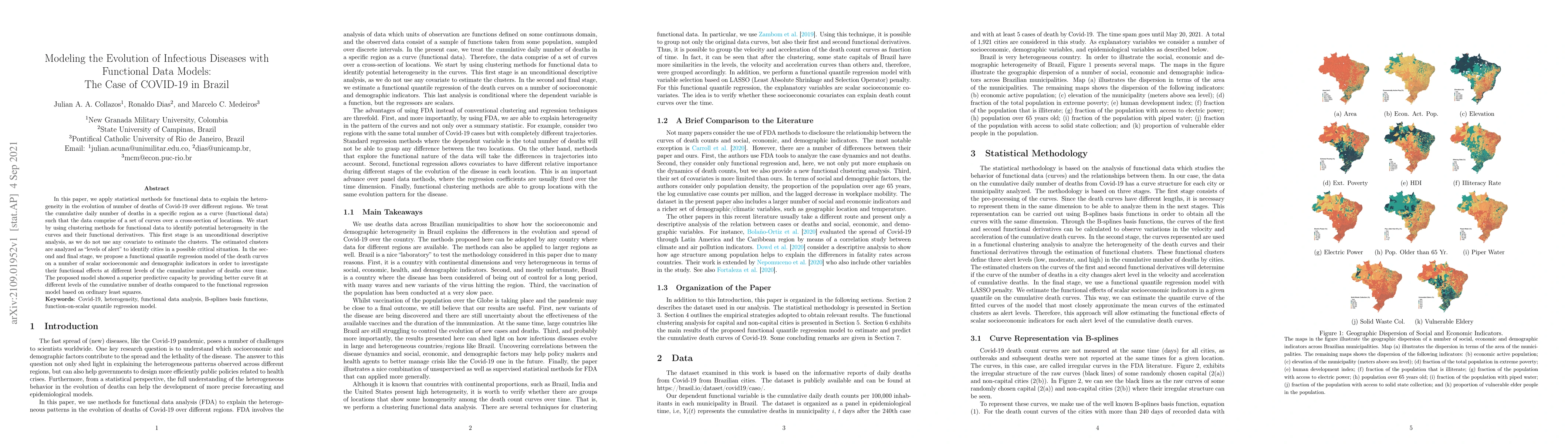

In this paper, we apply statistical methods for functional data to explain the heterogeneity in the evolution of number of deaths of Covid-19 over different regions. We treat the cumulative daily nu...

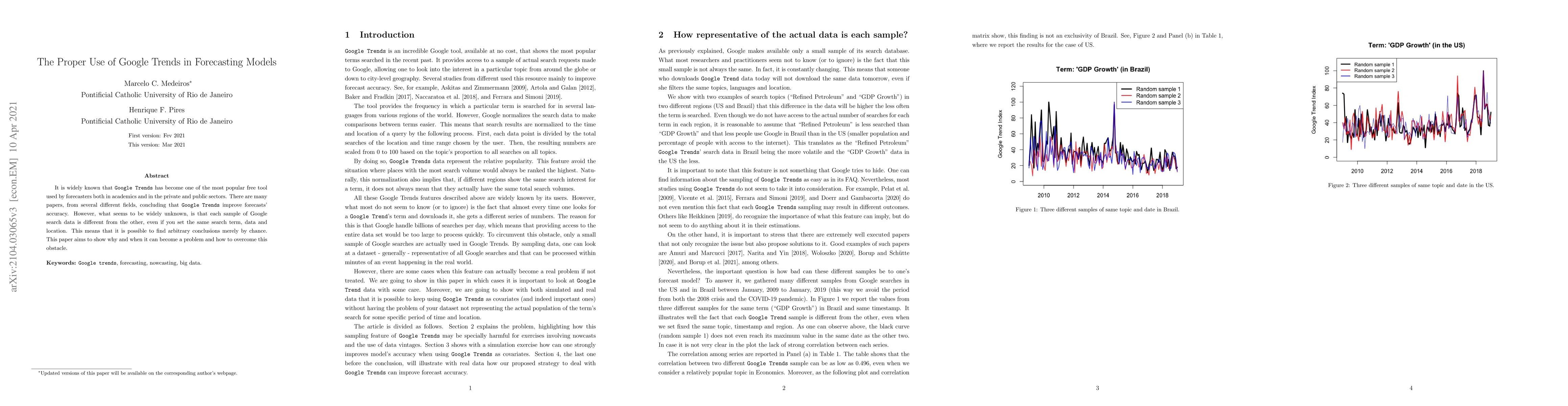

It is widely known that Google Trends have become one of the most popular free tools used by forecasters both in academics and in the private and public sectors. There are many papers, from several ...

Factor and sparse models are two widely used methods to impose a low-dimensional structure in high-dimensions. However, they are seemingly mutually exclusive. We propose a lifting method that combin...

In this paper we survey the most recent advances in supervised machine learning and high-dimensional models for time series forecasting. We consider both linear and nonlinear alternatives. Among the...

Optimal pricing, i.e., determining the price level that maximizes profit or revenue of a given product, is a vital task for the retail industry. To select such a quantity, one needs first to estimat...

We adopt an artificial counterfactual approach to assess the impact of lockdowns on the short-run evolution of the number of cases and deaths in some US states. To do so, we explore the different ti...

This paper considers the finite horizon portfolio rebalancing problem in terms of mean-variance optimization, where decisions are made based on current information on asset returns and transaction cos...

The forecasting combination puzzle is a well-known phenomenon in forecasting literature, stressing the challenge of outperforming the simple average when aggregating forecasts from diverse methods. Th...