Academic Profile

Statistics

Similar Authors

Papers on arXiv

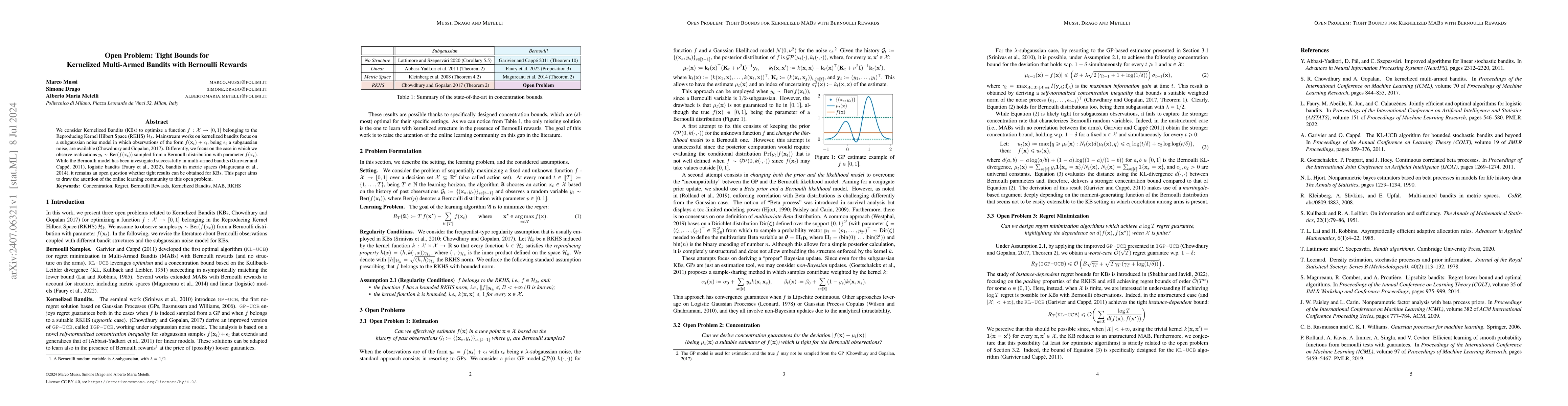

We consider Kernelized Bandits (KBs) to optimize a function $f : \mathcal{X} \rightarrow [0,1]$ belonging to the Reproducing Kernel Hilbert Space (RKHS) $\mathcal{H}_k$. Mainstream works on kernelized...

Constrained Reinforcement Learning (CRL) tackles sequential decision-making problems where agents are required to achieve goals by maximizing the expected return while meeting domain-specific constrai...

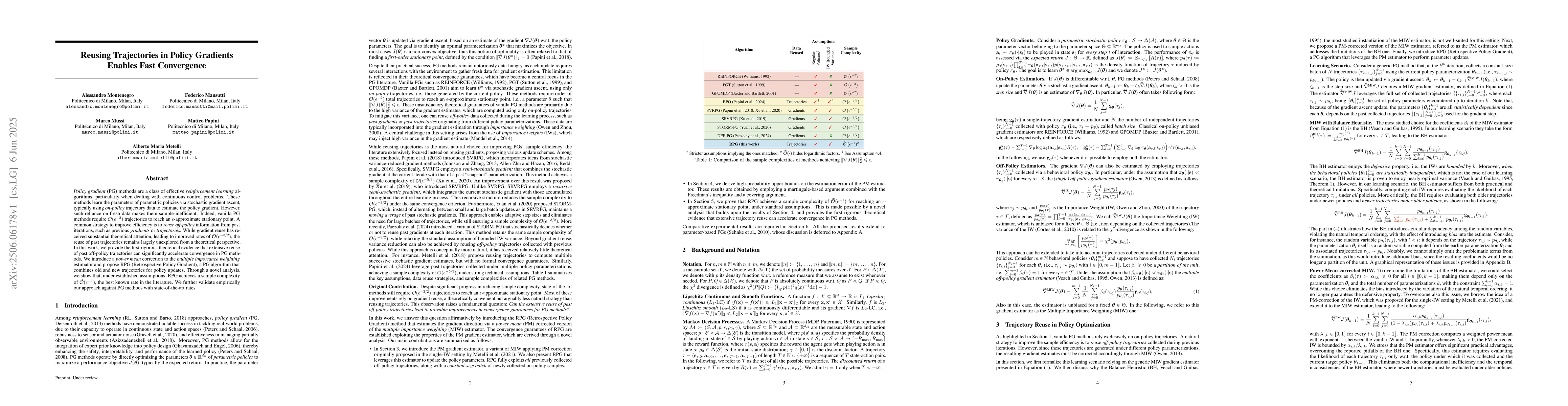

Policy gradient (PG) methods are successful approaches to deal with continuous reinforcement learning (RL) problems. They learn stochastic parametric (hyper)policies by either exploring in the space...

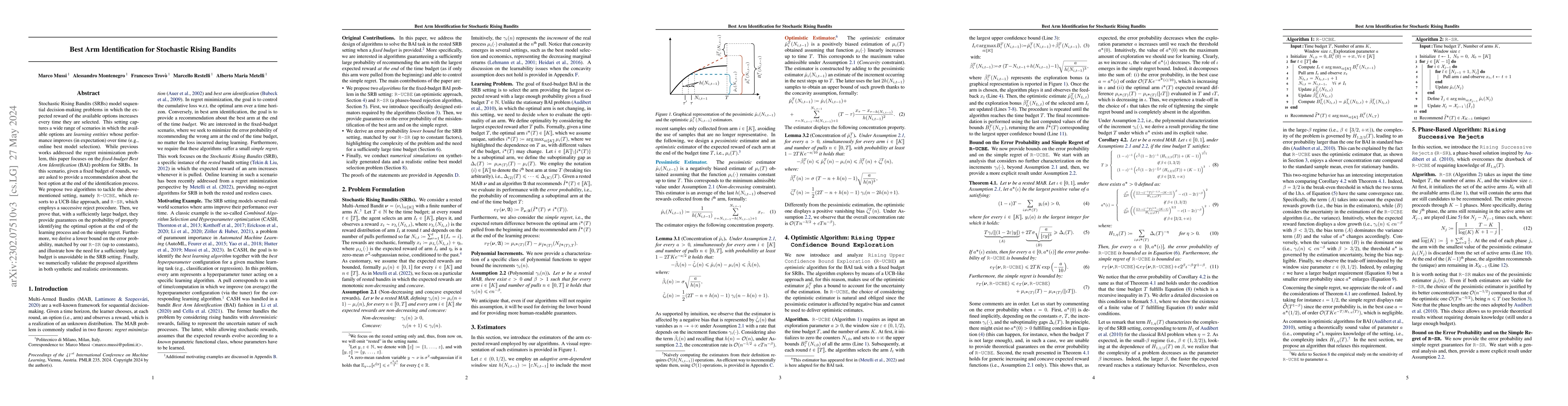

Stochastic Rising Bandits (SRBs) model sequential decision-making problems in which the expected reward of the available options increases every time they are selected. This setting captures a wide ...

Autoregressive processes naturally arise in a large variety of real-world scenarios, including stock markets, sales forecasting, weather prediction, advertising, and pricing. When facing a sequentia...

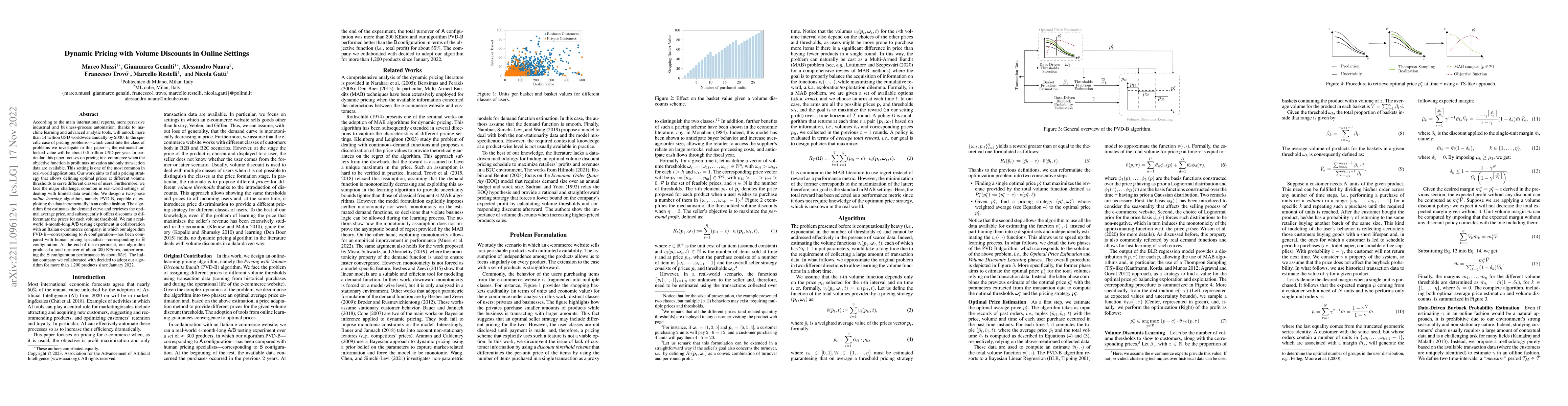

According to the main international reports, more pervasive industrial and business-process automation, thanks to machine learning and advanced analytic tools, will unlock more than 14 trillion USD ...

In many real-world sequential decision-making problems, an action does not immediately reflect on the feedback and spreads its effects over a long time frame. For instance, in online advertising, in...

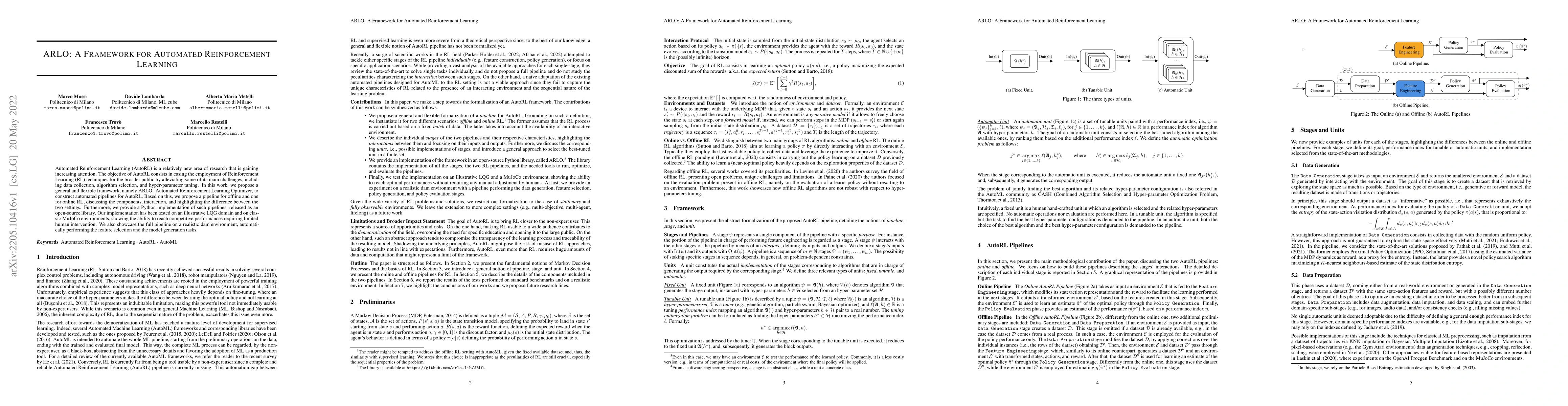

Automated Reinforcement Learning (AutoRL) is a relatively new area of research that is gaining increasing attention. The objective of AutoRL consists in easing the employment of Reinforcement Learni...

Rested and Restless Bandits are two well-known bandit settings that are useful to model real-world sequential decision-making problems in which the expected reward of an arm evolves over time due to t...

The increase of renewable energy generation towards the zero-emission target is making the problem of controlling power grids more and more challenging. The recent series of competitions Learning To R...

In this work, we provide a refined analysis of the UCBVI algorithm (Azar et al., 2017), improving both the bonus terms and the regret analysis. Additionally, we compare our version of UCBVI with both ...

Policy gradient (PG) methods are a class of effective reinforcement learning algorithms, particularly when dealing with continuous control problems. These methods learn the parameters of parametric po...

Constrained Reinforcement Learning (CRL) addresses sequential decision-making problems where agents are required to achieve goals by maximizing the expected return while meeting domain-specific constr...

In recent years, \emph{Reinforcement Learning} (RL) has made remarkable progress, achieving superhuman performance in a wide range of simulated environments. As research moves toward deploying RL in r...

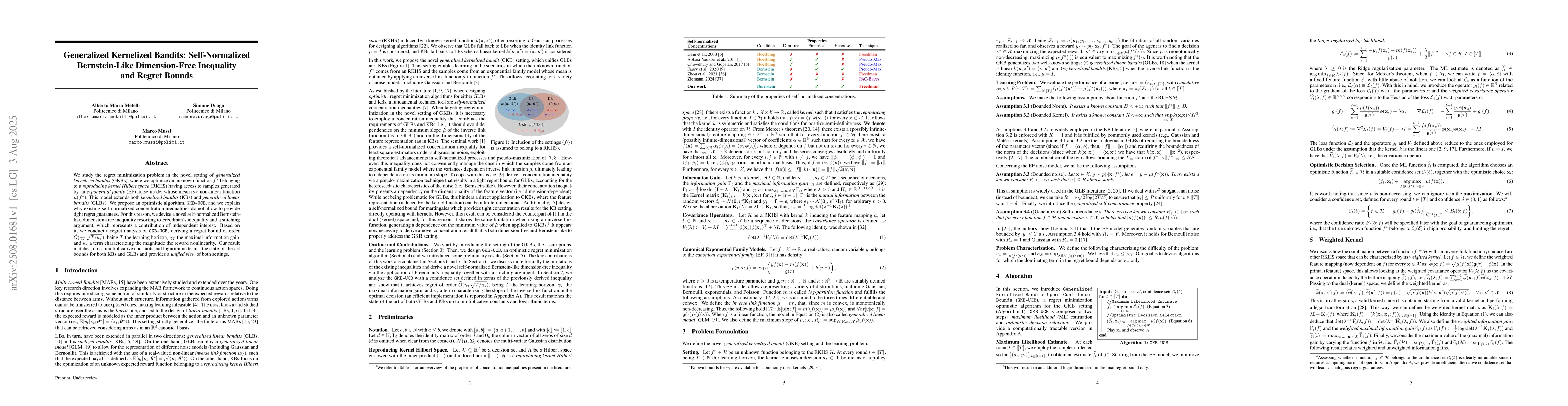

We study the regret minimization problem in the novel setting of generalized kernelized bandits (GKBs), where we optimize an unknown function $f^*$ belonging to a reproducing kernel Hilbert space (RKH...

The necessary integration of renewable energy sources, combined with the expanding scale of power networks, presents significant challenges in controlling modern power grids. Traditional control syste...

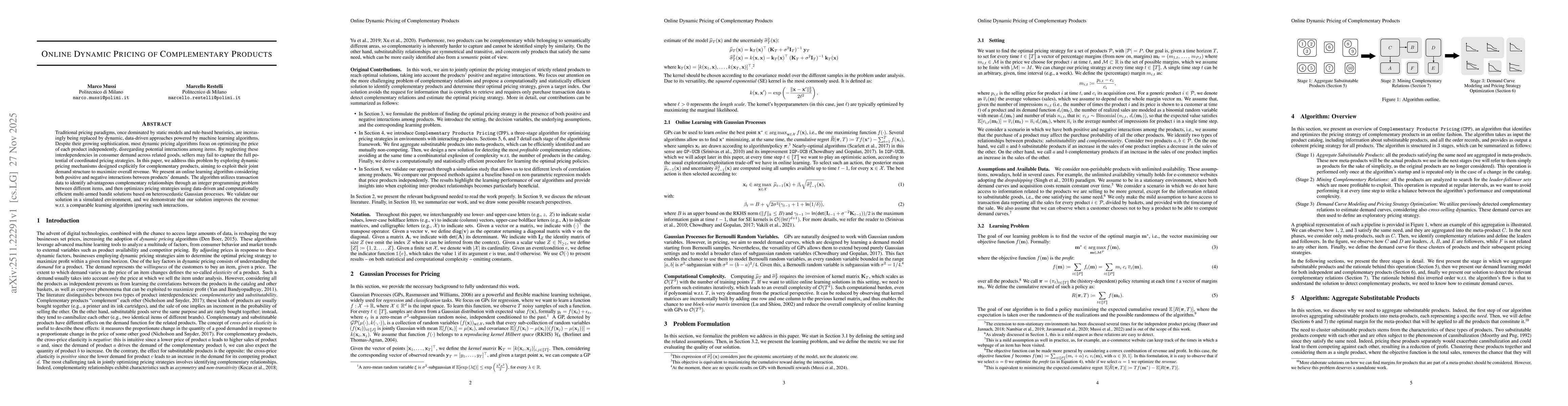

Traditional pricing paradigms, once dominated by static models and rule-based heuristics, are increasingly being replaced by dynamic, data-driven approaches powered by machine learning algorithms. Des...