Academic Profile

Statistics

Similar Authors

Papers on arXiv

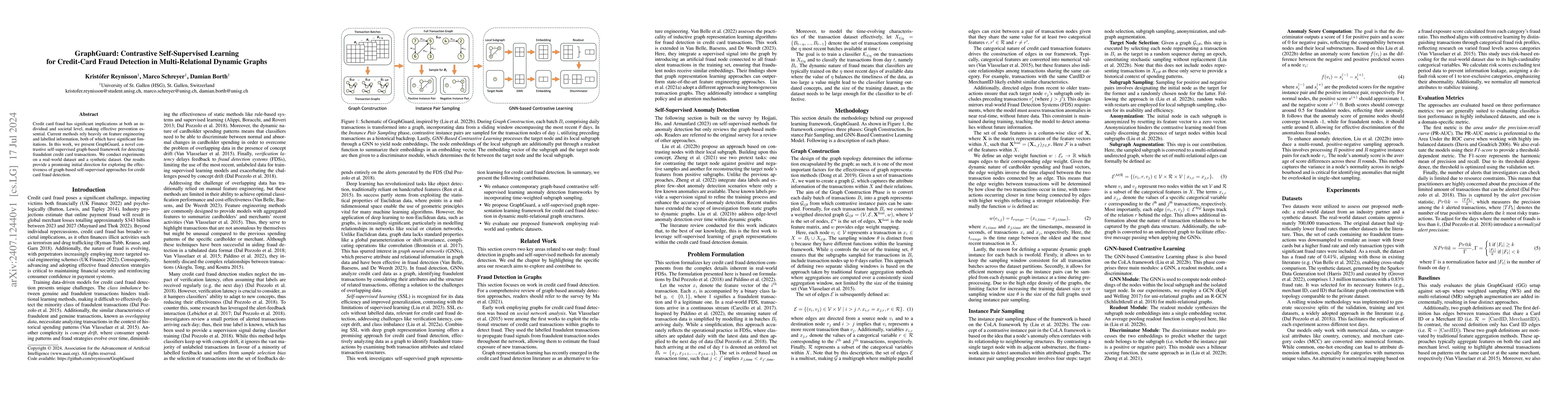

Credit card fraud has significant implications at both an individual and societal level, making effective prevention essential. Current methods rely heavily on feature engineering and labeled informat...

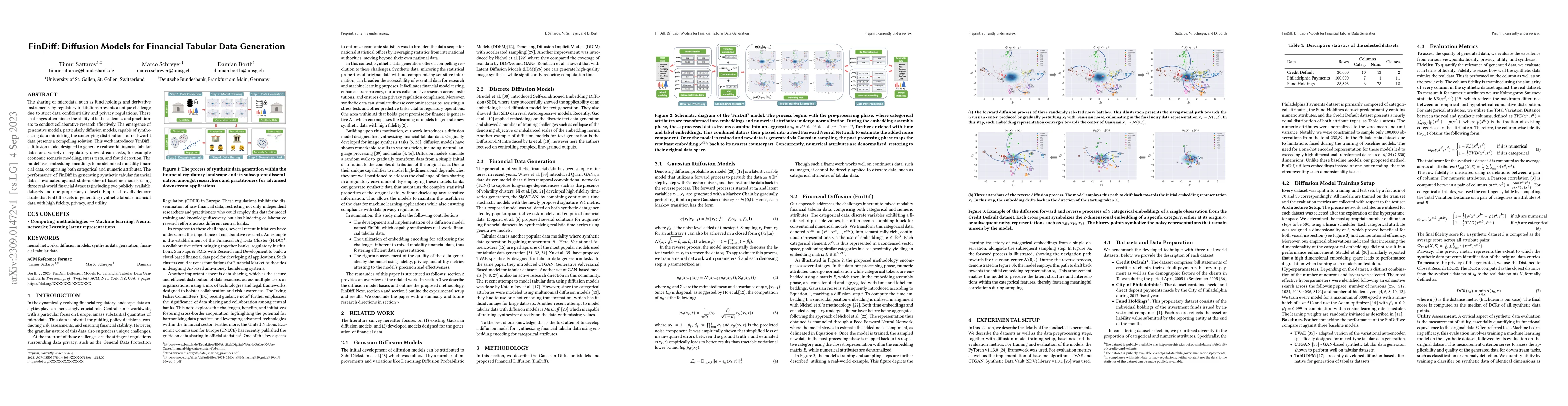

Realistic synthetic tabular data generation encounters significant challenges in preserving privacy, especially when dealing with sensitive information in domains like finance and healthcare. In thi...

The sharing of microdata, such as fund holdings and derivative instruments, by regulatory institutions presents a unique challenge due to strict data confidentiality and privacy regulations. These c...

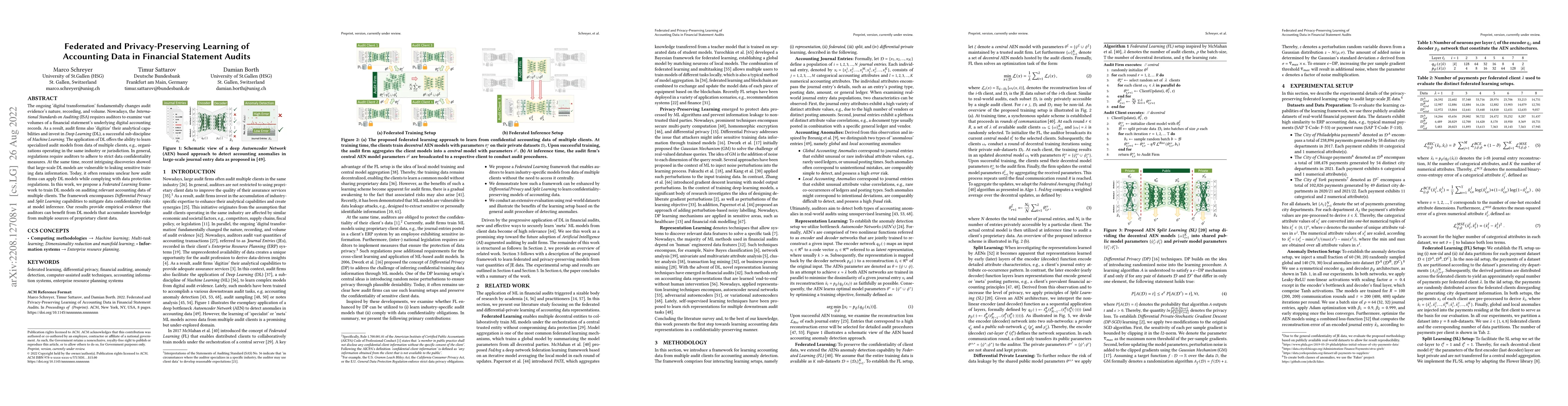

The International Standards on Auditing require auditors to collect reasonable assurance that financial statements are free of material misstatement. At the same time, a central objective of Continu...

Detecting accounting anomalies is a recurrent challenge in financial statement audits. Recently, novel methods derived from Deep-Learning (DL) have been proposed to audit the large volumes of a stat...

The ongoing 'digital transformation' fundamentally changes audit evidence's nature, recording, and volume. Nowadays, the International Standards on Auditing (ISA) requires auditors to examine vast v...

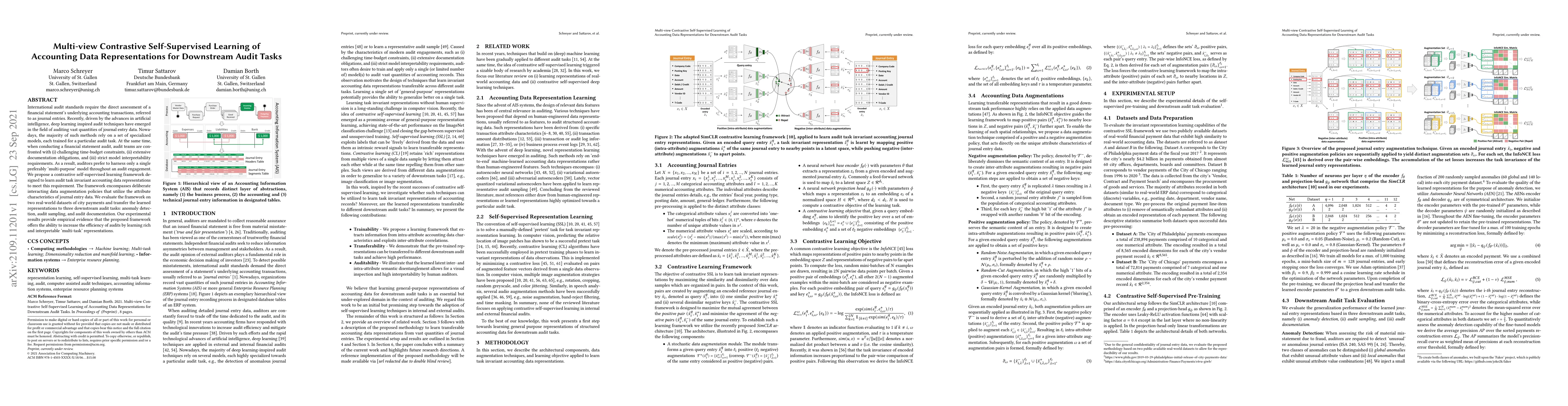

International audit standards require the direct assessment of a financial statement's underlying accounting journal entries. Driven by advances in artificial intelligence, deep-learning inspired au...

International audit standards require the direct assessment of a financial statement's underlying accounting transactions, referred to as journal entries. Recently, driven by the advances in artific...

Nowadays, organizations collect vast quantities of sensitive information in `Enterprise Resource Planning' (ERP) systems, such as accounting relevant transactions, customer master data, or strategic...

The audit of financial statements is designed to collect reasonable assurance that an issued statement is free from material misstatement 'true and fair presentation'. International audit standards ...

Nowadays, organizations collect vast quantities of accounting relevant transactions, referred to as 'journal entries', in 'Enterprise Resource Planning' (ERP) systems. The aggregation of those entri...

The detection of fraud in accounting data is a long-standing challenge in financial statement audits. Nowadays, the majority of applied techniques refer to handcrafted rules derived from known fraud...

The increasing demand for privacy-preserving data analytics in finance necessitates solutions for synthetic data generation that rigorously uphold privacy standards. We introduce DP-Fed-FinDiff framew...

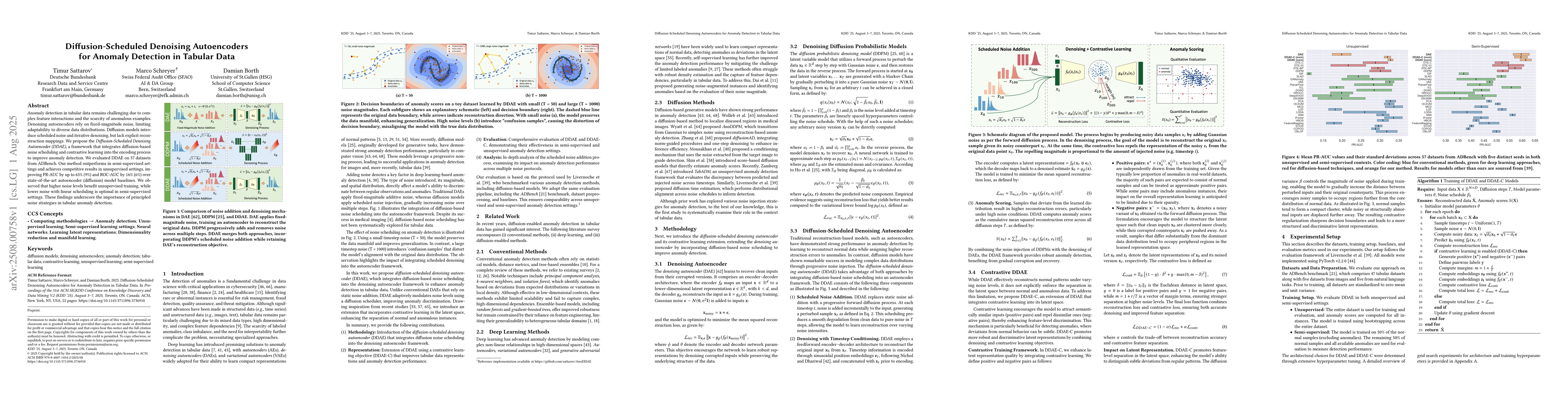

Anomaly detection in tabular data remains challenging due to complex feature interactions and the scarcity of anomalous examples. Denoising autoencoders rely on fixed-magnitude noise, limiting adaptab...

We introduce DP-FinDiff, a differentially private diffusion framework for synthesizing mixed-type tabular data. DP-FinDiff employs embedding-based representations for categorical features, reducing en...