Academic Profile

Statistics

Similar Authors

Papers on arXiv

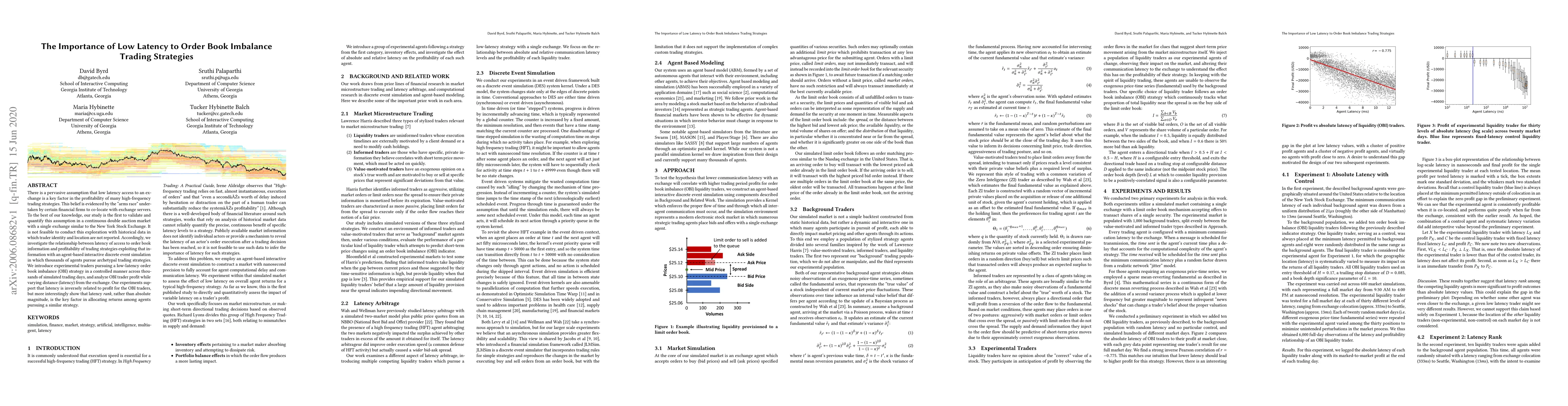

There is a pervasive assumption that low latency access to an exchange is a key factor in the profitability of many high-frequency trading strategies. This belief is evidenced by the "arms race" und...

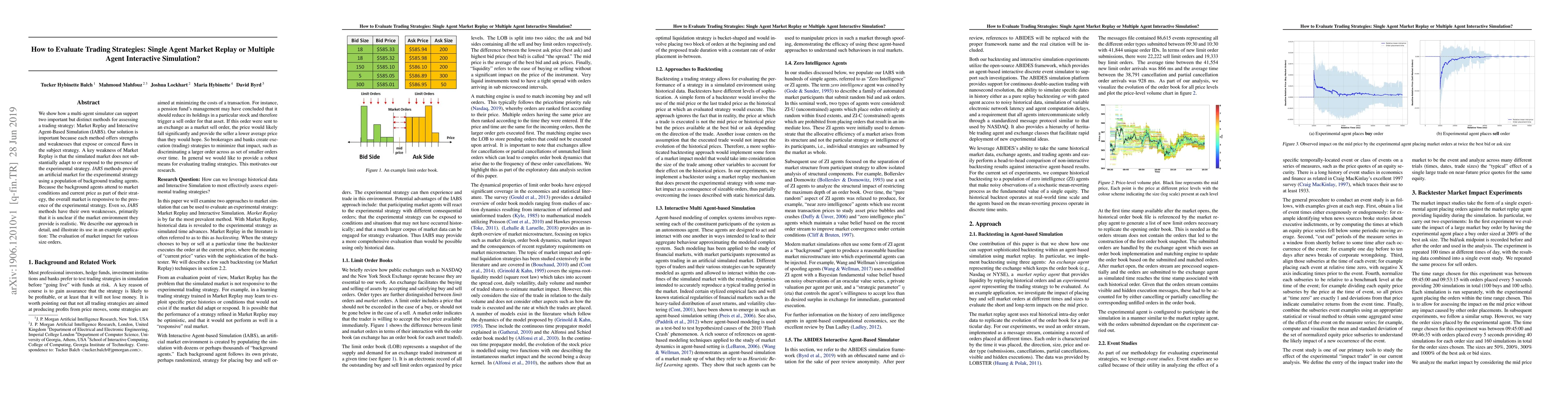

We show how a multi-agent simulator can support two important but distinct methods for assessing a trading strategy: Market Replay and Interactive Agent-Based Simulation (IABS). Our solution is impo...

This paper investigates whether artificial intelligence can enhance stock clustering compared to traditional methods. We consider this in the context of the semi-strong Efficient Markets Hypothesis (E...