Academic Profile

Statistics

Similar Authors

Papers on arXiv

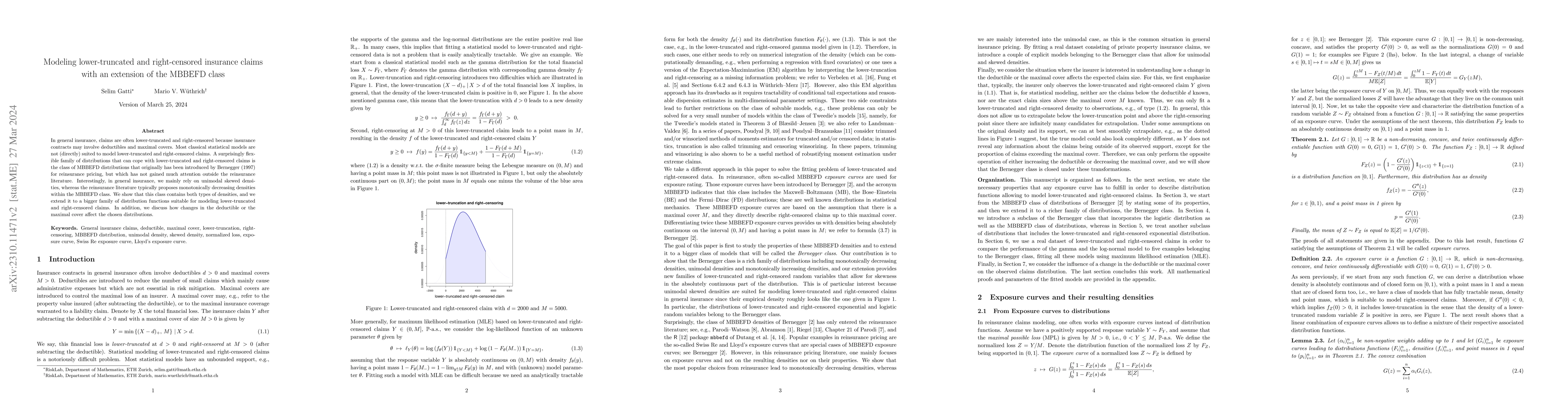

In general insurance, claims are often lower-truncated and right-censored because insurance contracts may involve deductibles and maximal covers. Most classical statistical models are not (directly)...

State-space models are widely used in many applications. In the domain of count data, one such example is the model proposed by Harvey and Fernandes (1989). Unlike many of its parameter-driven alter...

A very popular model-agnostic technique for explaining predictive models is the SHapley Additive exPlanation (SHAP). The two most popular versions of SHAP are a conditional expectation version and a...

Insurance pricing systems should fulfill the auto-calibration property to ensure that there is no systematic cross-financing between different price cohorts. Often, regression models are not auto-ca...

Indirect discrimination is an issue of major concern in algorithmic models. This is particularly the case in insurance pricing where protected policyholder characteristics are not allowed to be used...

The Gini index does not give a strictly consistent scoring rule in general. Therefore, maximizing the Gini index may lead to wrong decisions. The main issue is that the Gini index is a rank-based sc...

In applications of predictive modeling, such as insurance pricing, indirect or proxy discrimination is an issue of major concern. Namely, there exists the possibility that protected policyholder cha...

A main difficulty in actuarial claim size modeling is that there is no simple off-the-shelf distribution that simultaneously provides a good distributional model for the main body and the tail of th...

Deep learning models have gained great popularity in statistical modeling because they lead to very competitive regression models, often outperforming classical statistical models such as generalize...

We introduce a neural network approach for assessing the risk of a portfolio of assets and liabilities over a given time period. This requires a conditional valuation of the portfolio given the stat...

Inspired by the large success of Transformers in Large Language Models, these architectures are increasingly applied to tabular data. This is achieved by embedding tabular data into low-dimensional Eu...

Random delays between the occurrence of accident events and the corresponding reporting times of insurance claims is a standard feature of insurance data. The time lag between the reporting and the pr...

Auto-calibration is an important property of regression functions for actuarial applications. Comparably little is known about statistical testing of auto-calibration. Denuit et al.~(2024) recently pu...

State-space models are popular models in econometrics. Recently, these models have gained some popularity in the actuarial literature. The best known state-space models are of Kalman-filter type. Thes...

A statistical model is said to be calibrated if the resulting mean estimates perfectly match the true means of the underlying responses. Aiming for calibration is often not achievable in practice as o...

Originally introduced in cooperative game theory, Shapley values have become a very popular tool to explain machine learning predictions. Based on Shapley's fairness axioms, every input (feature compo...

Modeling feature interactions in tabular data remains a key challenge in predictive modeling, for example, as used for insurance pricing. This paper proposes the Tree-like Pairwise Interaction Network...

The starting point of our network architecture is the Credibility Transformer which extends the classical Transformer architecture by a credibility mechanism to improve model learning and predictive p...

The Gini score is a popular tool in statistical modeling and machine learning for model validation and model selection. It is a purely rank based score that allows one to assess risk rankings. The Gin...

Integer-valued generalized autoregressive conditional heteroskedastic (INGARCH) models are a popular framework for modeling serial dependence in count time-series. While convenient for modeling, predi...

We introduce Tab-TRM (Tabular-Tiny Recursive Model), a network architecture that adapts the recursive latent reasoning paradigm of Tiny Recursive Models (TRMs) to insurance modeling. Drawing inspirati...

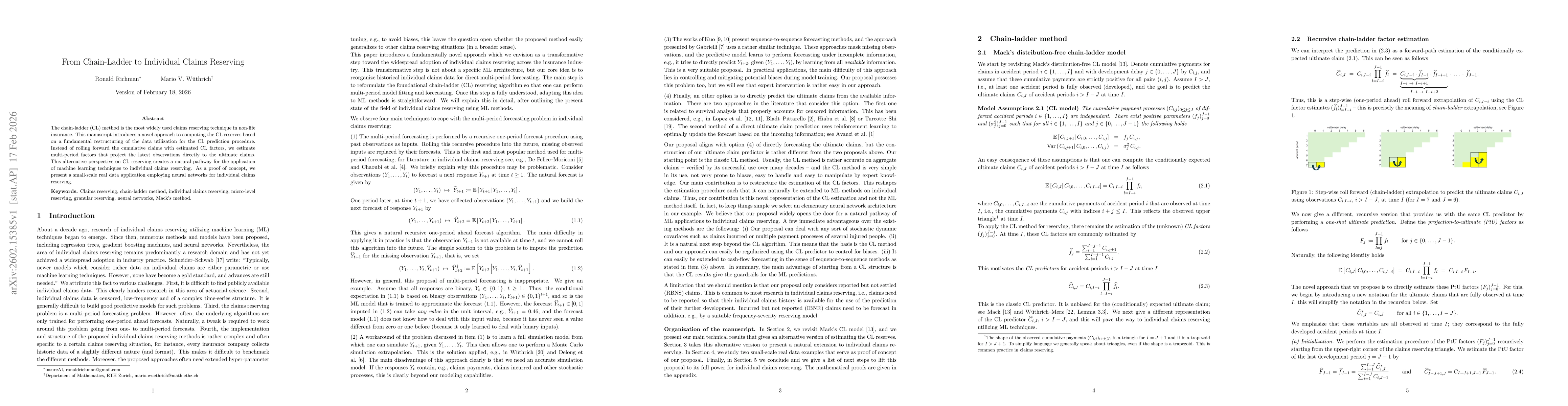

The chain-ladder (CL) method is the most widely used claims reserving technique in non-life insurance. This manuscript introduces a novel approach to computing the CL reserves based on a fundamental r...

Individual claims reserving has not yet become established in actuarial practice. We attribute this to the absence of a satisfactory methodology: existing approaches tend to be either overly complex o...

Claims reserving is one of the most important actuarial tasks in non-life insurance modeling. There are several popular methods to perform claims reserving such as the chain-ladder (CL), the Bornhuett...

Traditional insurance pricing relies on risk-based principles that ensure actuarial fairness and solvency but do not explicitly account for policyholders' price sensitivity. We formulate insurance pri...

The balance property is an important property of fitted statistical models deployed for insurance pricing. It guarantees that the total actuarial price in the fitted model is equal to the totally obse...