Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper delves into a nonparametric estimation approach for the interaction function within diffusion-type particle system models. We introduce two estimation methods based upon an empirical risk...

This paper investigates the estimation of the interaction function for a class of McKean-Vlasov stochastic differential equations. The estimation is based on observations of the associated particle ...

In this paper, we present the asymptotic theory for integrated functions of increments of Brownian local times in space. Specifically, we determine their first-order limit, along with the asymptotic...

In this paper we study the asymptotic theory for quadratic variation of a harmonizable fractional $\al$-stable process. We show a law of large numbers with a non-ergodic limit and obtain weak conver...

In this paper we study the properties of the Lasso estimator of the drift component in the diffusion setting. More specifically, we consider a multivariate parametric diffusion model $X$ observed co...

In this paper, we consider the problem of joint parameter estimation for drift and diffusion coefficients of a stochastic McKean-Vlasov equation and for the associated system of interacting particle...

The linear fractional stable motion generalizes two prominent classes of stochastic processes, namely stable L\'evy processes, and fractional Brownian motion. For this reason it may be regarded as a...

In this paper we study the problem of semiparametric estimation for a class of McKean-Vlasov stochastic differential equations. Our aim is to estimate the drift coefficient of a MV-SDE based on obse...

In this paper, we develop a penalized realized variance (PRV) estimator of the quadratic variation (QV) of a high-dimensional continuous It\^{o} semimartingale. We adapt the principle idea of regula...

This paper presents new limit theorems for power variation of fractional type symmetric infinitely divisible random fields. More specifically, the random field $X = (X(\boldsymbol{t}))_{\boldsymbol{...

In this paper we present new theoretical results for the Dantzig and Lasso estimators of the drift in a high dimensional Ornstein-Uhlenbeck model under sparsity constraints. Our focus is on oracle i...

In this paper we present a parametric estimation method for certain multi-parameter heavy-tailed L\'evy-driven moving averages. The theory relies on recent multivariate central limit theorems obtain...

In this paper we present new theoretical results on optimal estimation of certain random quantities based on high frequency observations of a L\'evy process. More specifically, we investigate the as...

In this paper we present an estimator for the three-dimensional parameter $(\sigma, \alpha, H)$ of the linear fractional stable motion, where $H$ represents the self-similarity parameter, and $(\sig...

In this paper we present a numerical scheme for stochastic differential equations based upon the Wiener chaos expansion. The approximation of a square integrable stochastic differential equation is ...

In this paper, we address high-dimensional parametric estimation of the drift function in diffusion models, specifically focusing on a $d$-dimensional ergodic diffusion process observed at discrete ti...

Statistical inference for stochastic processes has advanced significantly due to applications in diverse fields, but challenges remain in high-dimensional settings where parameters are allowed to grow...

This paper develops a statistical framework for goodness-of-fit testing of volatility functions in McKean-Vlasov stochastic differential equations, which describe large systems of interacting particle...

We study the local asymptotic normality (LAN) property for the likelihood function associated with discretely observed $d$-dimensional McKean-Vlasov stochastic differential equations over a fixed time...

In this paper, we propose a new jump robust quantile-based realised variance measure of ex-post return variation that can be computed using potentially noisy data. The estimator is consistent for the ...

In this paper, we show how to estimate the asymptotic (conditional) covariance matrix, which appears in central limit theorems in high-frequency estimation of asset return volatility. We provide a rec...

In this paper, we propose a nonparametric way to test the hypothesis that time-variation in intraday volatility is caused solely by a deterministic and recurrent diurnal pattern. We assume that noisy ...

We provide a set of probabilistic laws for estimating the quadratic variation of continuous semimartingales with realized range-based variance -- a statistic that replaces every squared return of real...

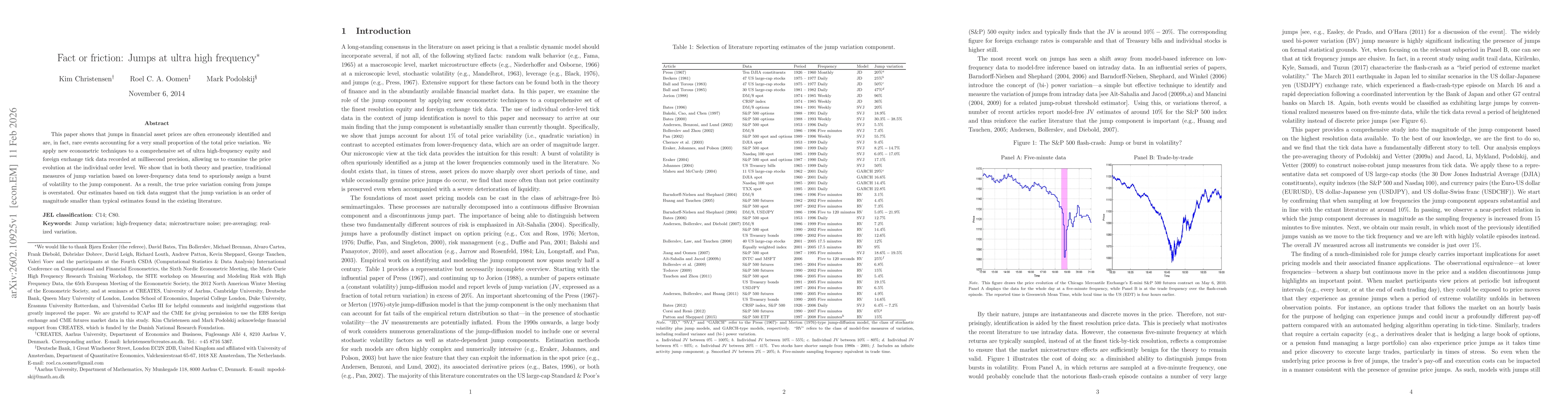

This paper shows that jumps in financial asset prices are often erroneously identified and are, in fact, rare events accounting for a very small proportion of the total price variation. We apply new e...

In this paper, we present a realized range-based multipower variation theory, which can be used to estimate return variation and draw jump-robust inference about the diffusive volatility component, wh...

This paper presents a Hayashi-Yoshida type estimator for the covariation matrix of continuous Itô semimartingales observed with noise. The coordinates of the multivariate process are assumed to be obs...

We show how pre-averaging can be applied to the problem of measuring the ex-post covariance of financial asset returns under microstructure noise and non-synchronous trading. A pre-averaged realised c...