Academic Profile

Statistics

Similar Authors

Papers on arXiv

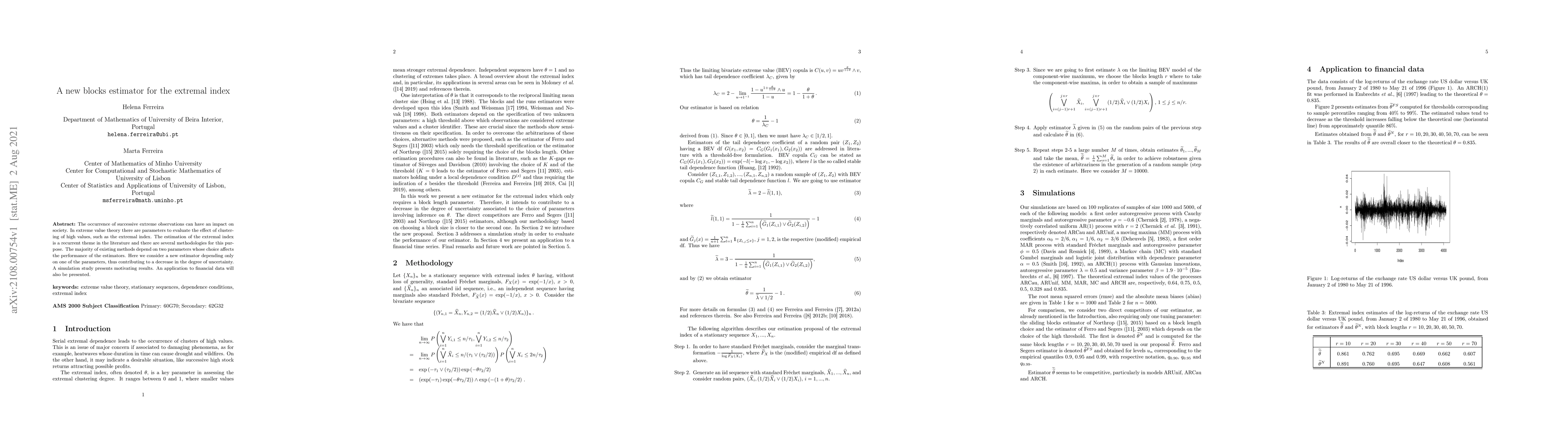

The occurrence of successive extreme observations can have an impact on society. In extreme value theory there are parameters to evaluate the effect of clustering of high values, such as the extrema...

The risk of occurrence of atypical phenomena is a cross-cutting concern in several areas, such as engineering, climatology, finance, actuarial, among others. Extreme value theory is the natural tool...

We define a multivariate medial correlation coefficient that extends the probabilistic interpretation and properties of Blomqvist's $\beta$ coefficient, incorporates multivariate marginal dependenci...

The extreme values theory presents specific tools for modeling and predicting extreme phenomena. In particular, risk assessment is often analyzed through measures for tail dependence and high values...

The modeling of risk situations that occur in a space-time framework can be done using max-stable random fields on lattices. Although the summary coefficients for the spatial and temporal behaviour ...