Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop methods for the solution of inhomogeneous Robin type boundary value problems (BVPs) that arise for certain linear parabolic Partial Differential Equations (PDEs) on a half line, as well a...

We propose a new theoretical framework that exploits convolution kernels to transform a Volterra path-dependent (non-Markovian) stochastic process into a standard (Markovian) diffusion process. This...

We propose a quantization-based numerical scheme for a family of decoupled FBSDEs. We simplify the scheme for the control in Pag\`es and Sagna (2018) so that our approach is fully based on recursive...

We analyze the VIX futures market with a focus on the exchange-traded notes written on such contracts, in particular we investigate the VXX notes tracking the short-end part of the futures term stru...

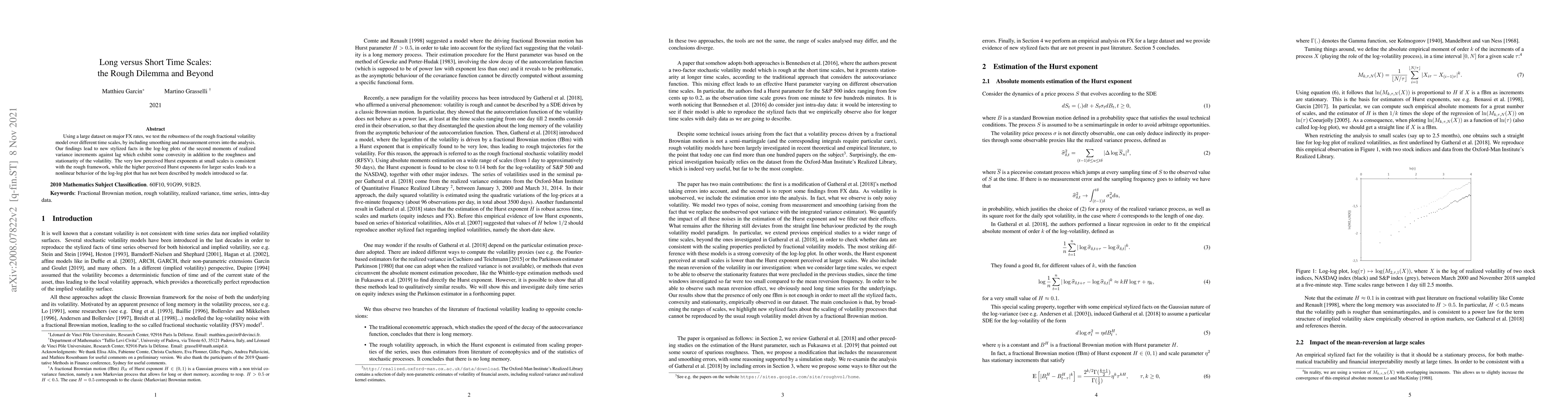

Using a large dataset on major FX rates, we test the robustness of the rough fractional volatility model over different time scales, by including smoothing and measurement errors into the analysis. ...

We investigate a class of non-Markovian processes that hold particular relevance in the realm of mathematical finance. This family encompasses path-dependent volatility models, including those pioneer...

Despite decades of research in risk management, most of the literature has focused on scalar risk measures (like e.g. Value-at-Risk and Expected Shortfall). While such scalar measures provide compact ...