Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this work, we consider the notion of "criterion collapse," in which optimization of one metric implies optimality in another, with a particular focus on conditions for collapse into error probabi...

As models grow larger and more complex, achieving better off-sample generalization with minimal trial-and-error is critical to the reliability and economy of machine learning workflows. As a proxy f...

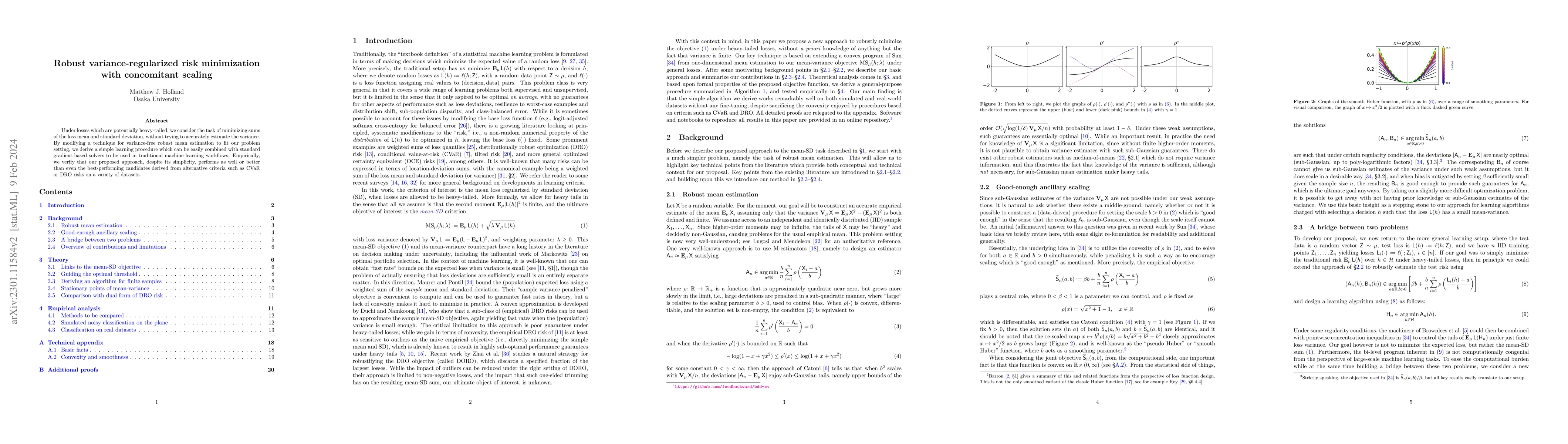

Under losses which are potentially heavy-tailed, we consider the task of minimizing sums of the loss mean and standard deviation, without trying to accurately estimate the variance. By modifying a t...

Many novel notions of "risk" (e.g., CVaR, tilted risk, DRO risk) have been proposed and studied, but these risks are all at least as sensitive as the mean to loss tails on the upside, and tend to ig...

Virtually all machine learning tasks are characterized using some form of loss function, and "good performance" is typically stated in terms of a sufficiently small average loss, taken over the rand...

Under data distributions which may be heavy-tailed, many stochastic gradient-based learning algorithms are driven by feedback queried at points with almost no performance guarantees on their own. He...

In this work, we consider the setting of learning problems under a wide class of spectral risk (or "L-risk") functions, where a Lipschitz-continuous spectral density is used to flexibly assign weigh...

We study scalable alternatives to robust gradient descent (RGD) techniques that can be used when the losses and/or gradients can be heavy-tailed, though this will be unknown to the learner. The core...

In this work, we study a new class of risks defined in terms of the location and deviation of the loss distribution, generalizing far beyond classical mean-variance risk functions. The class is easi...

In this work, we study some novel applications of conformal inference techniques to the problem of providing machine learning procedures with more transparent, accurate, and practical performance gu...

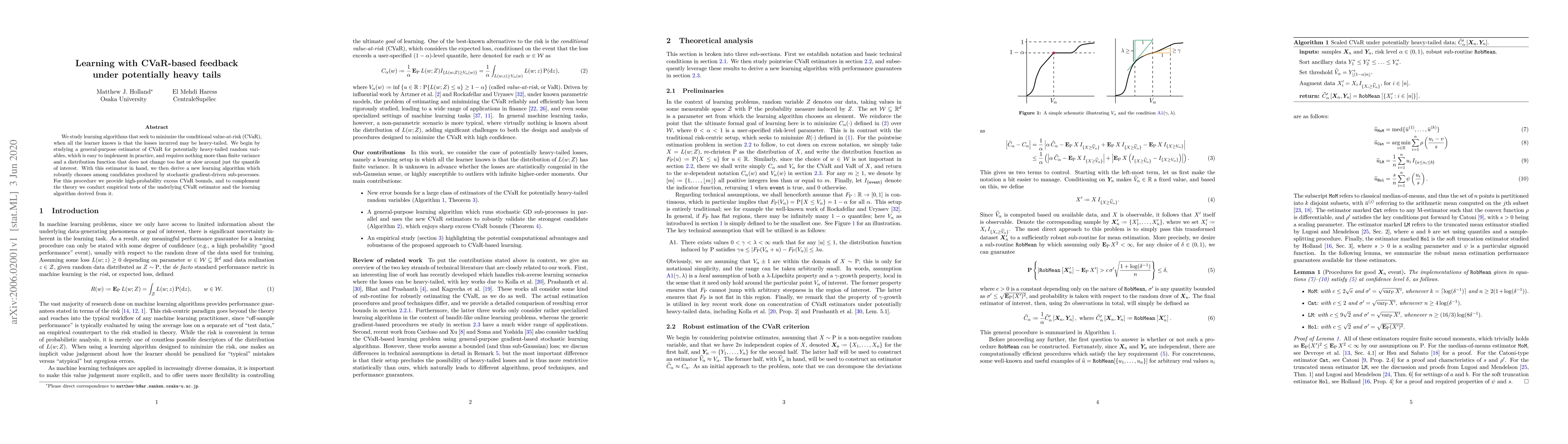

We study learning algorithms that seek to minimize the conditional value-at-risk (CVaR), when all the learner knows is that the losses incurred may be heavy-tailed. We begin by studying a general-pu...

Real-world data is laden with outlying values. The challenge for machine learning is that the learner typically has no prior knowledge of whether the feedback it receives (losses, gradients, etc.) w...

We study a scalable alternative to robust gradient descent (RGD) techniques that can be used when the gradients can be heavy-tailed, though this will be unknown to the learner. The core technique is...

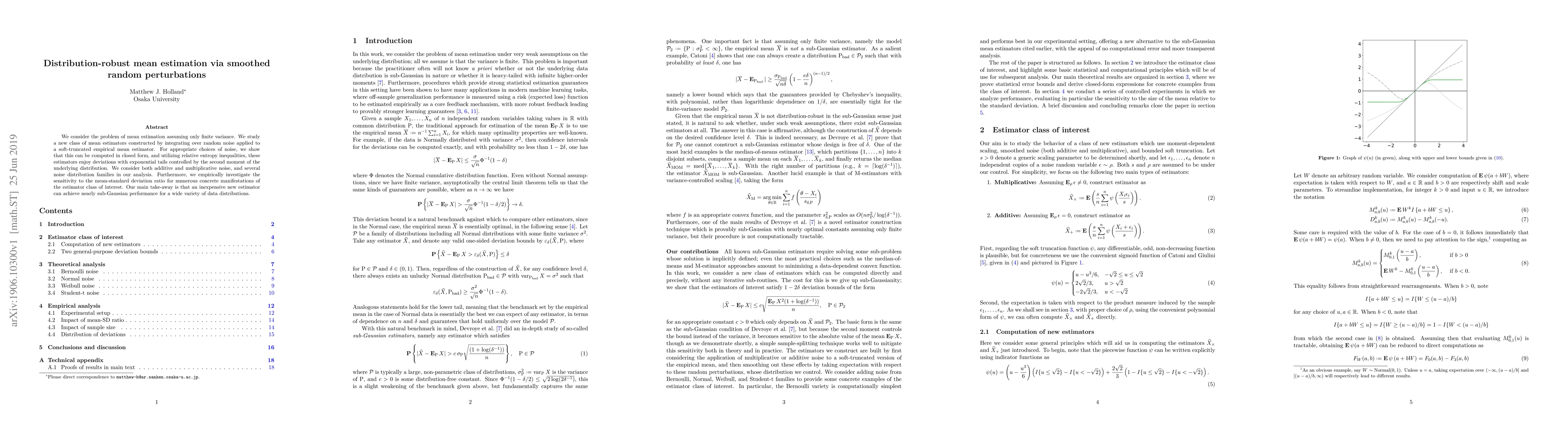

We consider the problem of mean estimation assuming only finite variance. We study a new class of mean estimators constructed by integrating over random noise applied to a soft-truncated empirical m...

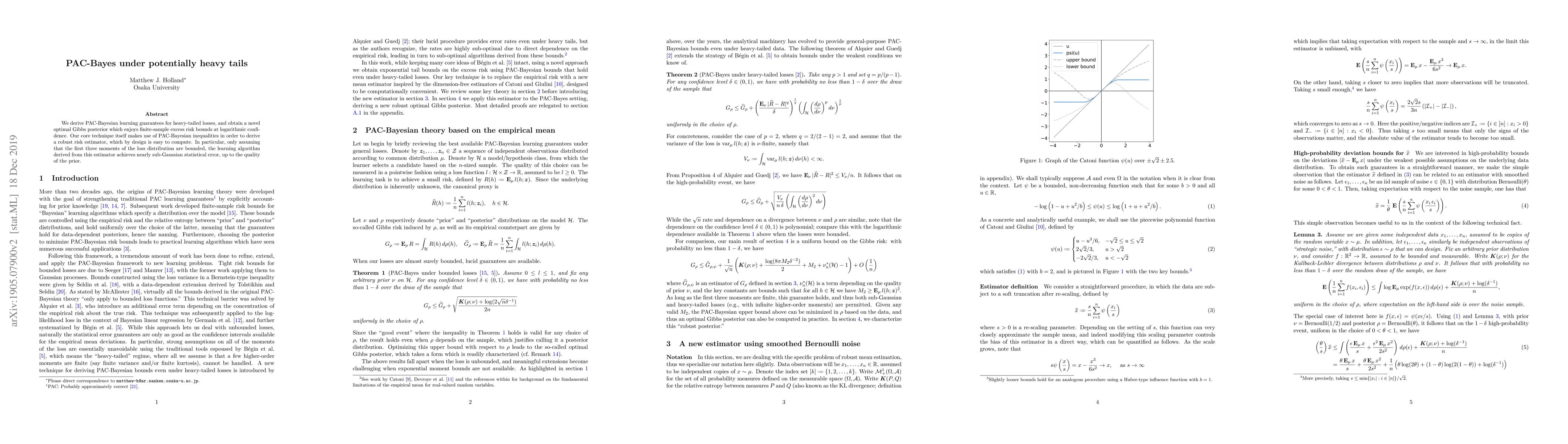

We derive PAC-Bayesian learning guarantees for heavy-tailed losses, and obtain a novel optimal Gibbs posterior which enjoys finite-sample excess risk bounds at logarithmic confidence. Our core techn...

While the traditional formulation of machine learning tasks is in terms of performance on average, in practice we are often interested in how well a trained model performs on rare or difficult data po...