Academic Profile

Statistics

Similar Authors

Papers on arXiv

Maximal Extractable Value (MEV) in Constant Function Market Making is fairly well understood. Does having dynamic weights, as found in liquidity boostrap pools (LBPs), Temporal-function market maker...

Dynamic AMM pools, as found in Temporal Function Market Making, rebalance their holdings to a new desired ratio (e.g. moving from being 50-50 between two assets to being 90-10 in favour of one of th...

Convex optimisation has provided a mechanism to determine arbitrage trades on automated market markets (AMMs) since almost their inception. Here we outline generic closed-form solutions for $N$-toke...

U-Net architectures are ubiquitous in state-of-the-art deep learning, however their regularisation properties and relationship to wavelets are understudied. In this paper, we formulate a multi-resol...

Work in deep clustering focuses on finding a single partition of data. However, high-dimensional data, such as images, typically feature multiple interesting characteristics one could cluster over. ...

In this paper, we investigate the algorithmic stability of unsupervised representation learning with deep generative models, as a function of repeated re-training on the same input data. Algorithms ...

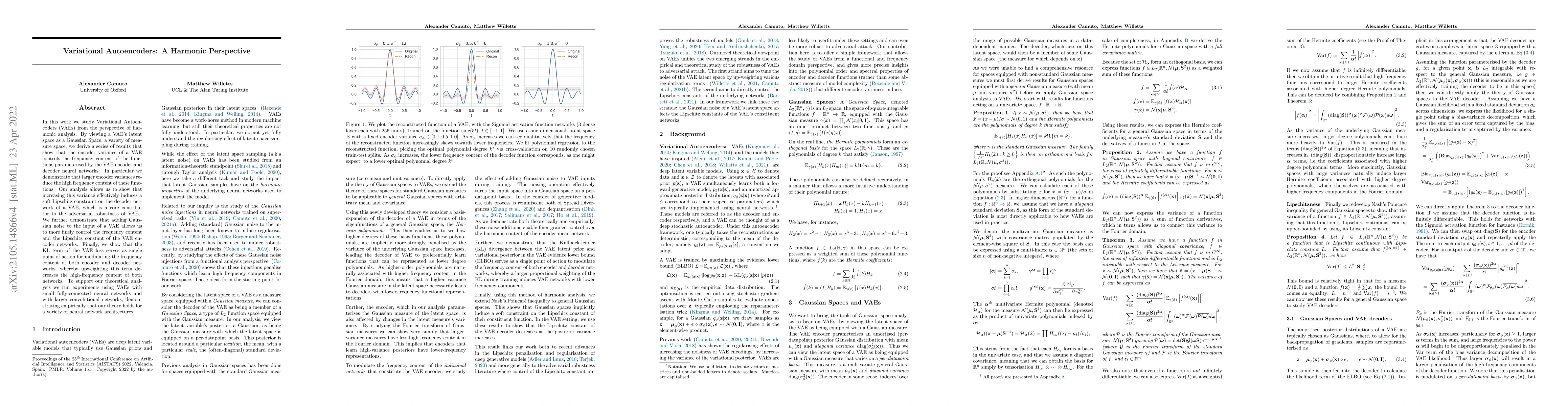

In this work we study Variational Autoencoders (VAEs) from the perspective of harmonic analysis. By viewing a VAE's latent space as a Gaussian Space, a variety of measure space, we derive a series o...

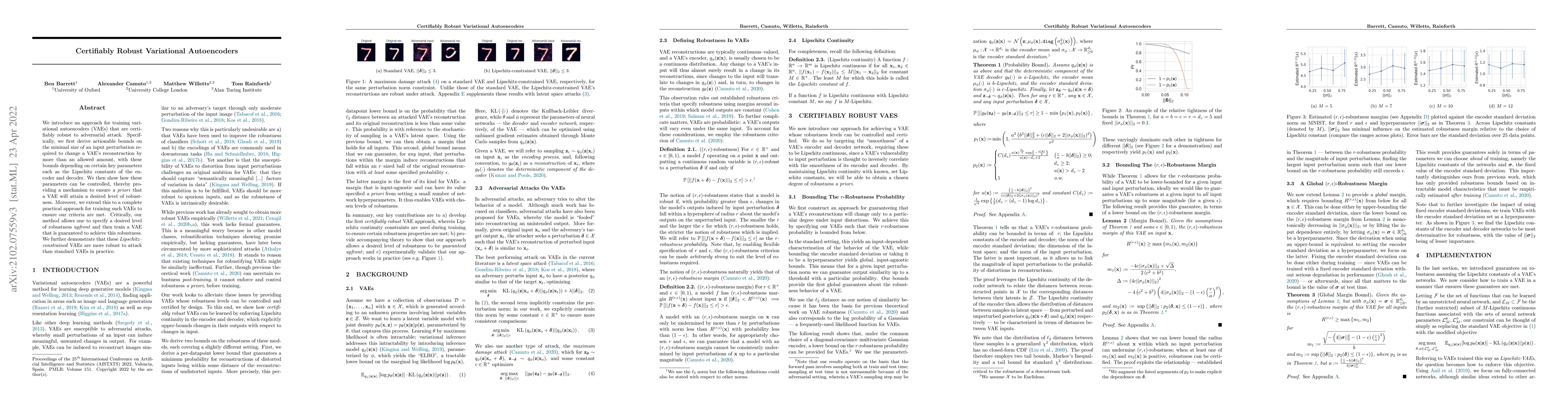

We introduce an approach for training Variational Autoencoders (VAEs) that are certifiably robust to adversarial attack. Specifically, we first derive actionable bounds on the minimal size of an inp...

We study the regularisation induced in neural networks by Gaussian noise injections (GNIs). Though such injections have been extensively studied when applied to data, there have been few studies on ...

Successfully training Variational Autoencoders (VAEs) with a hierarchy of discrete latent variables remains an area of active research. Vector-Quantised VAEs are a powerful approach to discrete VA...

Separating high-dimensional data like images into independent latent factors, i.e independent component analysis (ICA), remains an open research problem. As we show, existing probabilistic deep gene...

We show that the stochasticity in training ResNets for image classification on GPUs in TensorFlow is dominated by the non-determinism from GPUs, rather than by the initialisation of the weights and ...

We develop a new method for regularising neural networks. We learn a probability distribution over the activations of all layers of the model and then insert imputed values into the network during t...

Variational autoencoders (VAEs) have recently been shown to be vulnerable to adversarial attacks, wherein they are fooled into reconstructing a chosen target image. However, how to defend against su...

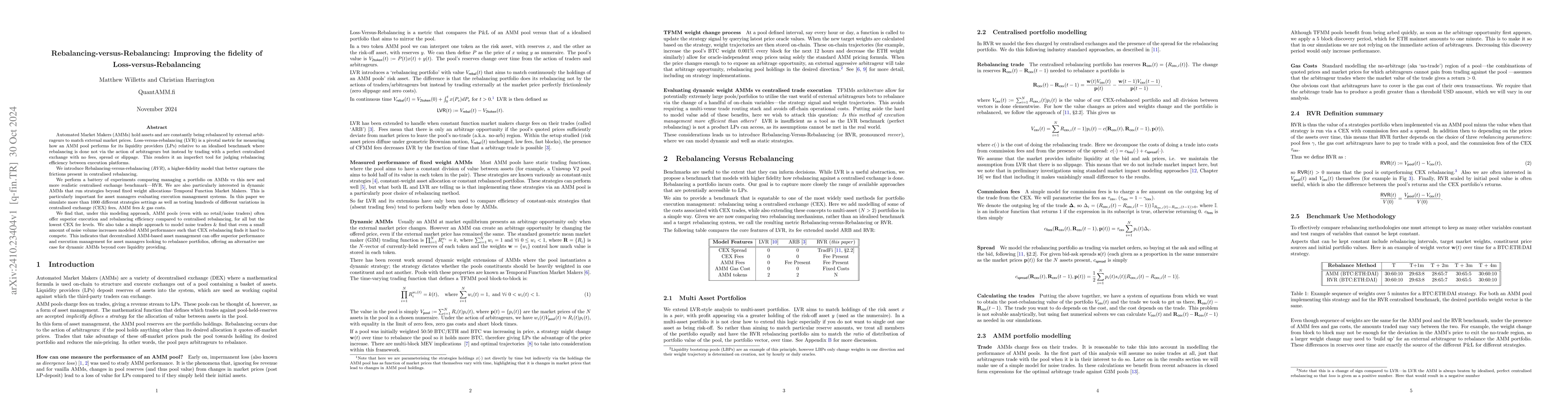

Automated Market Makers (AMMs) hold assets and are constantly being rebalanced by external arbitrageurs to match external market prices. Loss-versus-rebalancing (LVR) is a pivotal metric for measuring...

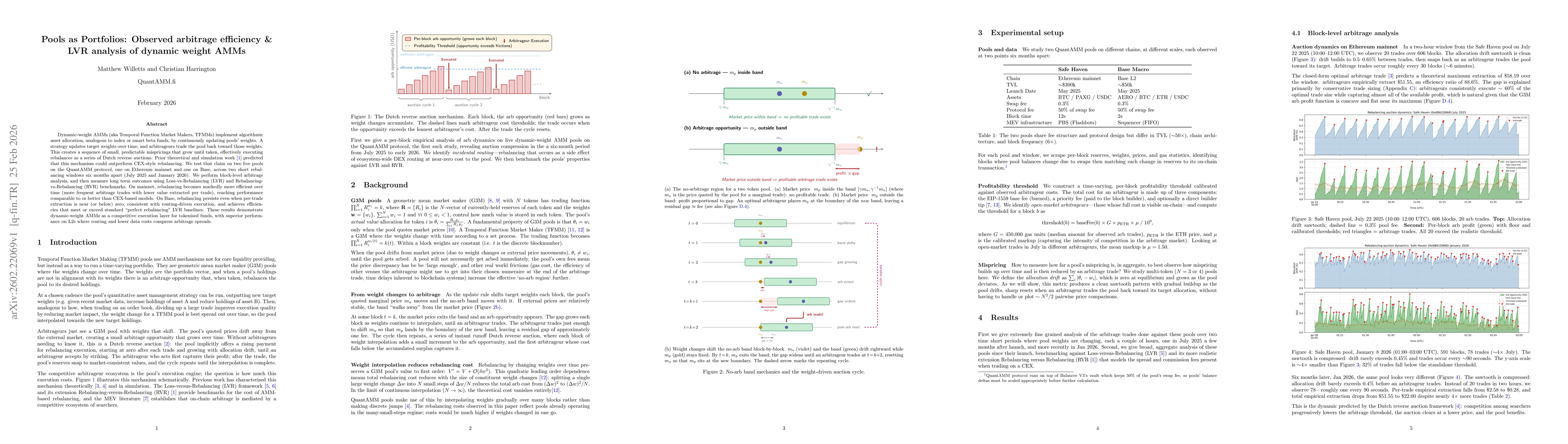

Dynamic-weight AMMs (aka Temporal Function Market Makers, TFMMs) implement algorithmic asset allocation, analogous to index or smart beta funds, by continuously updating pools' weights. A strategy upd...

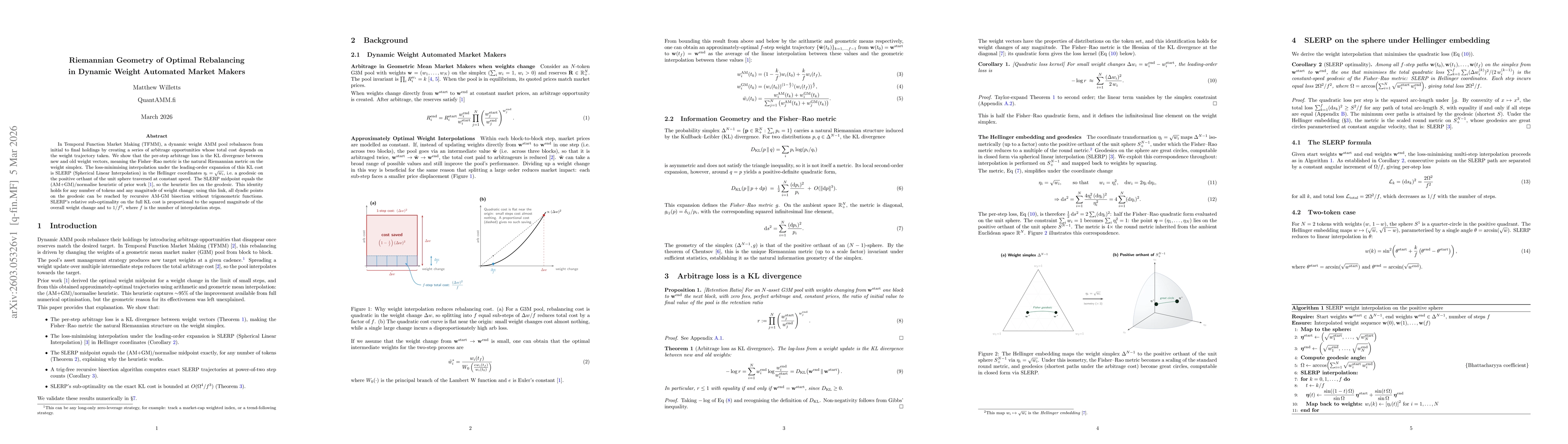

In Temporal Function Market Making (TFMM), a dynamic weight AMM pool rebalances from initial to final holdings by creating a series of arbitrage opportunities whose total cost depends on the weight tr...