Academic Profile

Statistics

Similar Authors

Papers on arXiv

Considering that both the entropy-based market information and the Hurst exponent are useful tools for determining whether the efficient market hypothesis holds for a given asset, we study the link ...

We are interested in the nonparametric estimation of the probability density of price returns, using the kernel approach. The output of the method heavily relies on the selection of a bandwidth para...

We determine the amount of information contained in a time series of price returns at a given time scale, by using a widespread tool of the information theory, namely the Shannon entropy, applied to...

A theoretical expression is derived for the mean squared error of a nonparametric estimator of the tail dependence coefficient, depending on a threshold that defines which rank delimits the tails of...

The fractional Brownian motion (fBm) extends the standard Brownian motion by introducing some dependence between non-overlapping increments. Consequently, if one considers for example that log-price...

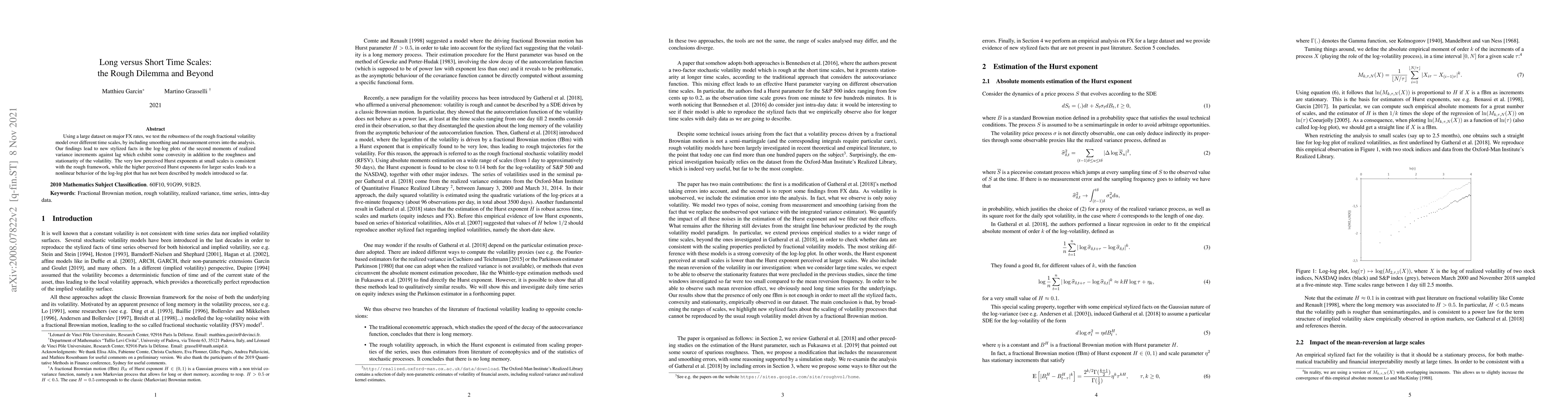

Using a large dataset on major FX rates, we test the robustness of the rough fractional volatility model over different time scales, by including smoothing and measurement errors into the analysis. ...

This paper investigates the impact of COVID-19 on financial markets. It focuses on the evolution of the market efficiency, using two efficiency indicators: the Hurst exponent and the memory paramete...

The time-varying kernel density estimation relies on two free parameters: the bandwidth and the discount factor. We propose to select these parameters so as to minimize a criterion consistent with t...

The absolute-moment method is widespread for estimating the Hurst exponent of a fractional Brownian motion $X$. But this method is biased when applied to a stationary version of $X$, in particular a...

The Fractional Stochastic Regularity Model (FSRM) is an extension of Black-Scholes model describing the multifractal nature of prices. It is based on a multifractional process with a random Hurst expo...

Starting from a basic model in which the dynamic of the transaction prices is a geometric Brownian motion disrupted by a microstructure white noise, corresponding to the random alternation of bids and...

The linear fractional stable motion (LFSM) extends the fractional Brownian motion (fBm) by considering $\alpha$-stable increments. We propose a method to forecast future increments of the LFSM from pa...

Relative entropy, as a divergence metric between two distributions, can be used for offline change-point detection and extends classical methods that mainly rely on moment-based discrepancies. To buil...

This paper introduces a novel measure to quantify the directional dependence of extreme events between two variables. The proposed approach is designed to capture asymmetric tail dependence by studyin...

The composite likelihood method reduces the computational cost of parameter estimation in time series by considering several subsets of observations instead of all observations at once. The asymptotic...