Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider an Ito-financial market at which the risky assets' returns are derived endogenously through a market-clearing condition amongst heterogeneous risk-averse investors with quadratic prefere...

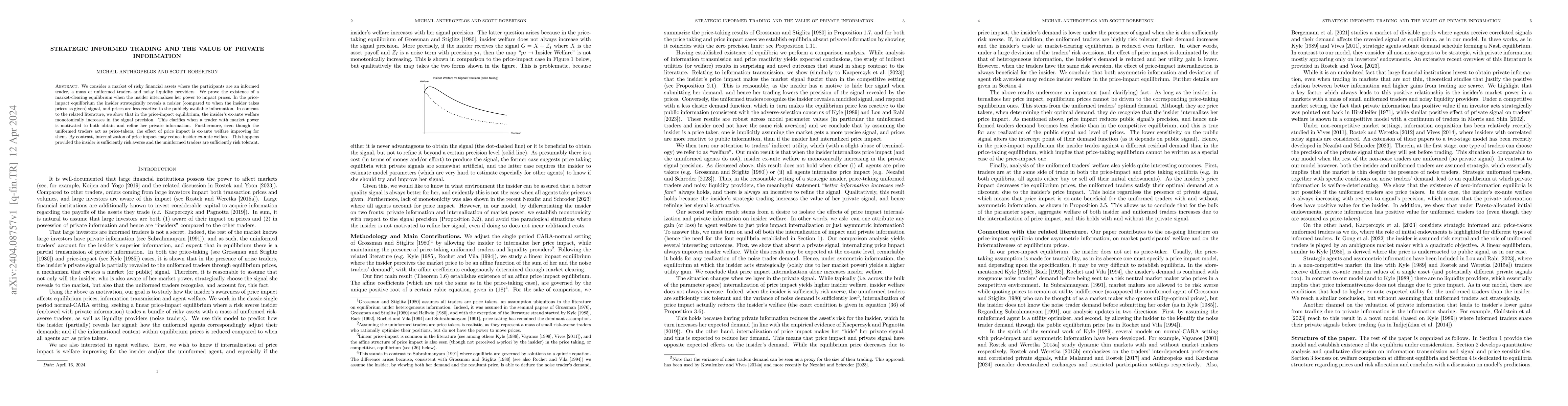

We consider a market of risky financial assets where the participants are an informed trader, a mass of uniformed traders and noisy liquidity providers. We prove the existence of a market-clearing e...

We consider portfolio selection under nonparametric $\alpha$-maxmin ambiguity in the neighbourhood of a reference distribution. We show strict concavity of the portfolio problem under ambiguity aver...

In an Ito-diffusion market, two fund managers trade under relative performance concerns. For both the asset specialization and diversification settings, we analyze the passive and competitive cases....

We introduce a strategic behavior in reinsurance bilateral transactions, where agents choose the risk preferences they will appear to have in the transaction. Within a wide class of risk measures, w...

We consider a financial market in which traders potentially face restrictions in trading some of the available securities. Traders are heterogeneous with respect to their beliefs and risk profiles, ...

In an incomplete financial market with general continuous semimartingale dynamics; we model an investor with log-utility preferences who, in addition to an initial capital, receives units of a non-tra...