Academic Profile

Statistics

Similar Authors

Papers on arXiv

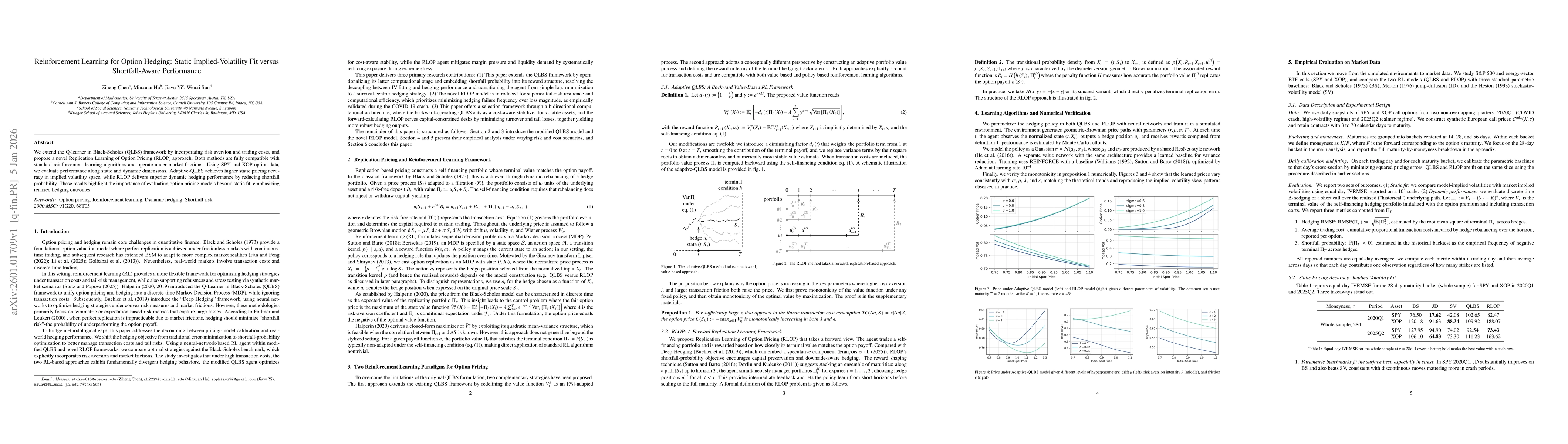

We extend the Q-learner in Black-Scholes (QLBS) framework by incorporating risk aversion and trading costs, and propose a novel Replication Learning of Option Pricing (RLOP) approach. Both methods are...

The deployment of autonomous AI agents in derivatives markets has widened a practical gap between static model calibration and realized hedging outcomes. We introduce two reinforcement learning framew...

In limited-data settings, a single endpoint mean of an evaluation metric such as the Continuous Ranked Probability Score (CRPS) is itself a random variable, yet it is routinely reported as if it were ...

Standard evaluations of Bayesian deep learning methods assume that metric estimates are reliable, but we show this assumption fails under data scarcity. Method rankings are not only unreliable at smal...

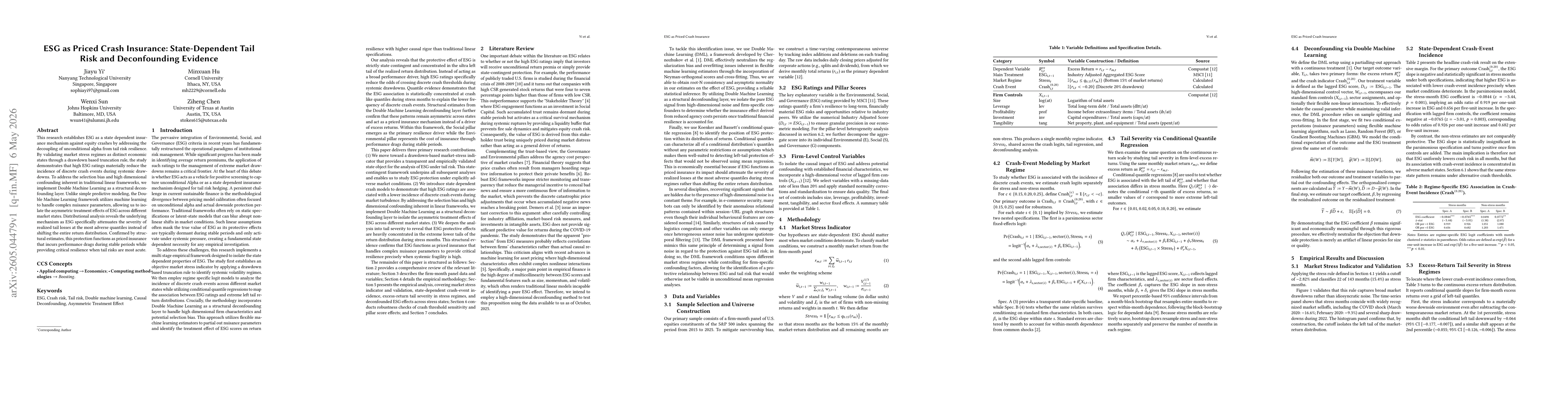

This research establishes ESG as a state dependent insurance mechanism against equity crashes by addressing the decoupling of unconditional alpha from tail risk resilience. By validating market stress...

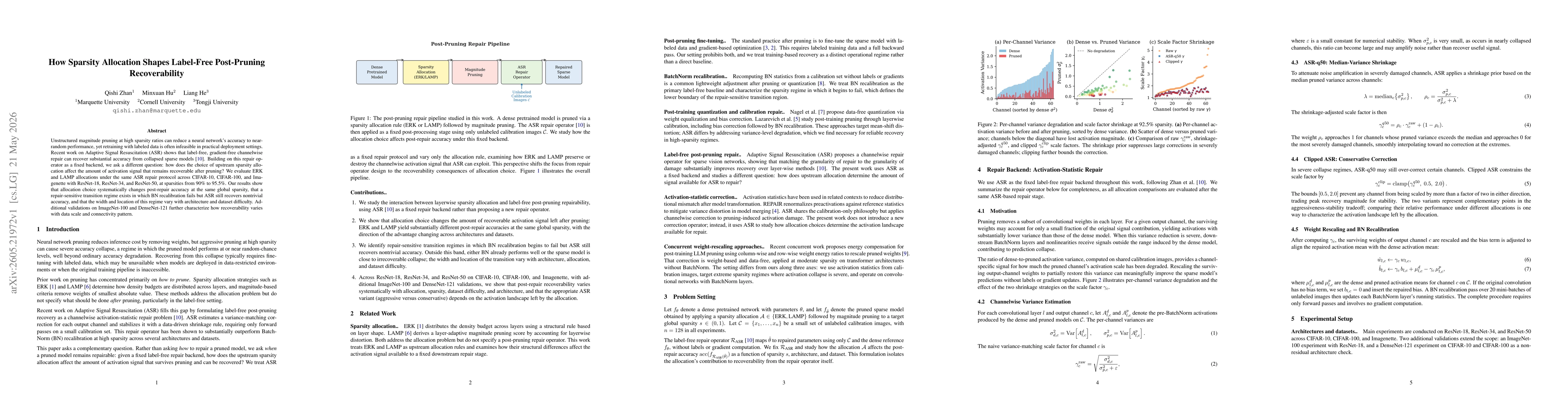

Unstructured magnitude pruning at high sparsity can reduce neural network accuracy to near-random performance, while labeled retraining may be unavailable in practical deployment settings. Label-free ...

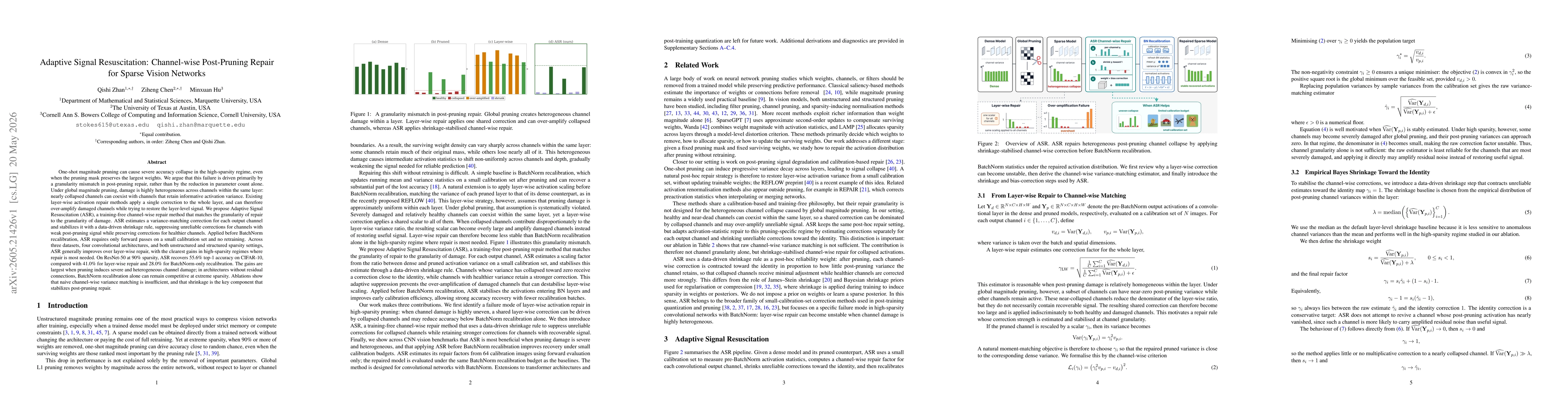

One-shot magnitude pruning can cause severe accuracy collapse in the high-sparsity regime, even when the pruning mask preserves the largest weights. We argue that this failure reflects a granularity m...

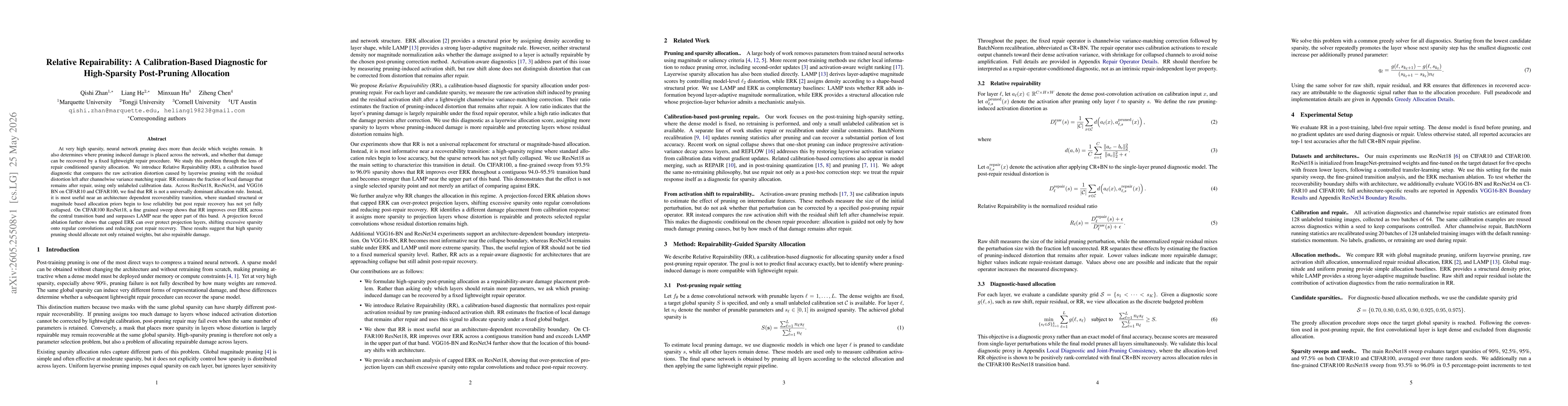

At very high sparsity, neural network pruning does more than decide which weights remain. It also determines where pruning induced damage is placed across the network, and whether that damage can be r...

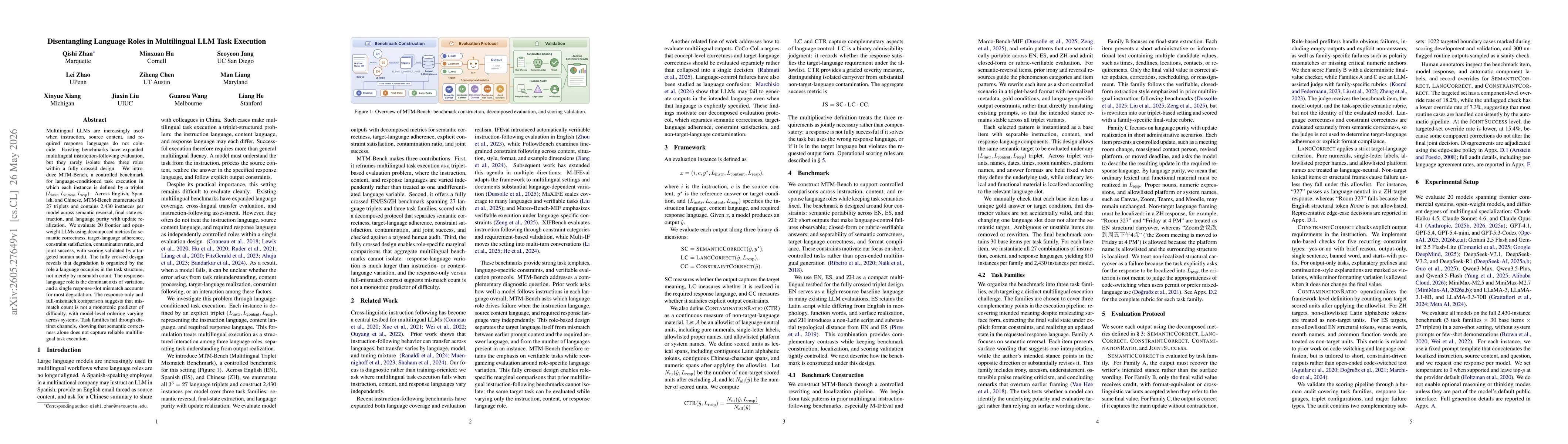

Multilingual LLMs are increasingly used when instruction, source content, and required response languages do not coincide. Existing benchmarks have expanded multilingual instruction-following evaluati...

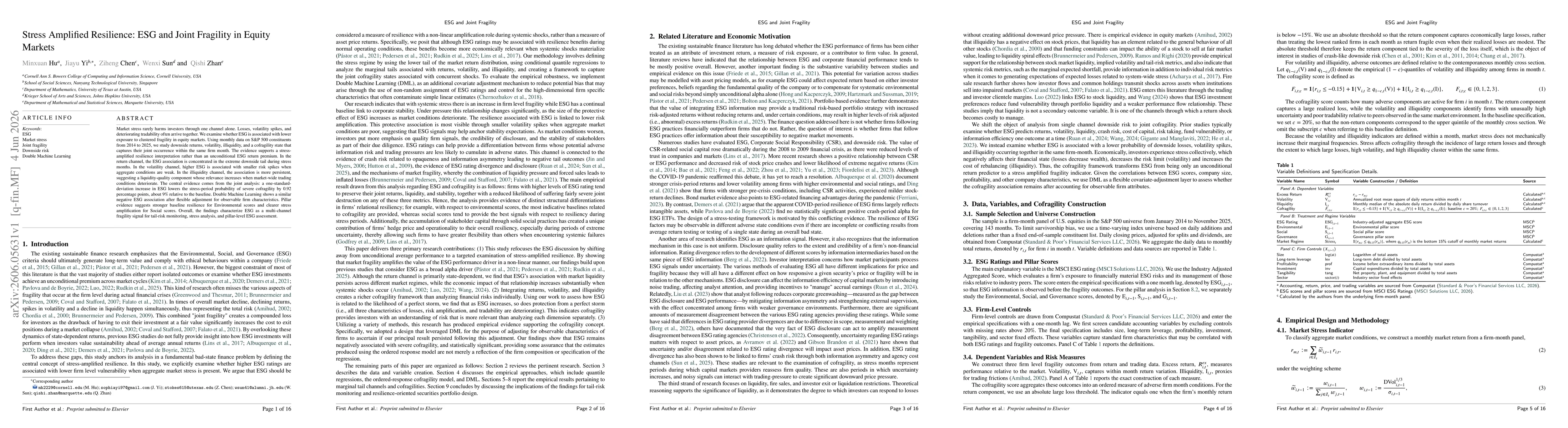

Market stress rarely harms investors through one channel alone. Losses, volatility spikes, and deteriorating tradability often arrive together. We examine whether ESG is associated with lower exposure...

Segmenting slender curvilinear structures such as retinal vessels, cracks, and roads demands topological correctness, as even a single-pixel discontinuity can fragment a continuous network and invalid...

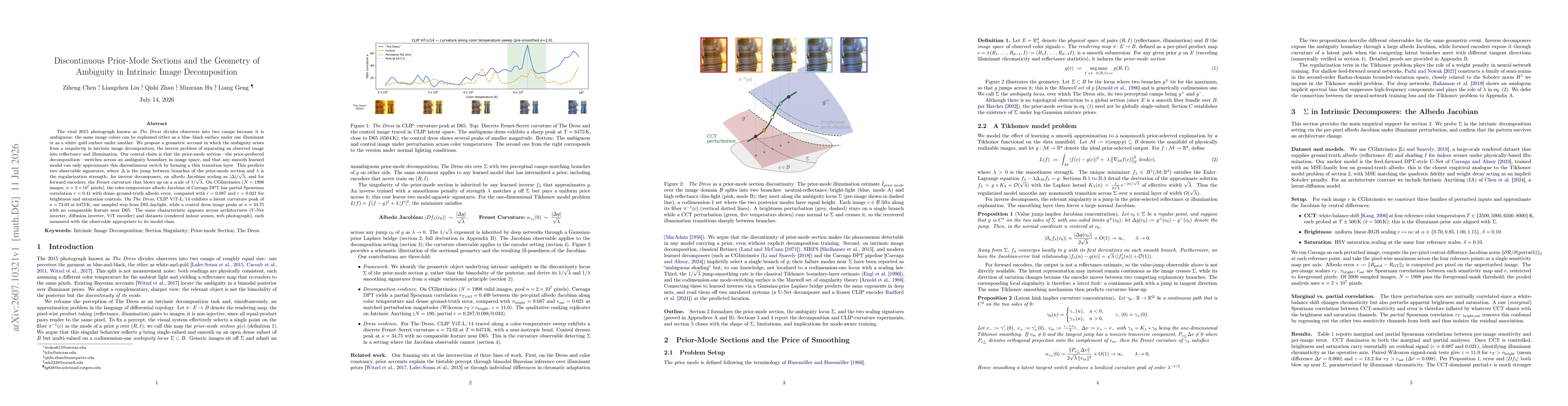

The viral 2015 photograph known as "The Dress" divides observers into two camps because it is ambiguous: the same image colors can be explained either as a blue-black surface under one illuminant or a...