Academic Profile

Statistics

Papers on arXiv

Quantum computing has recently appeared in the headlines of many scientific and popular publications. In the context of quantitative finance, we provide here an overview of its potential.

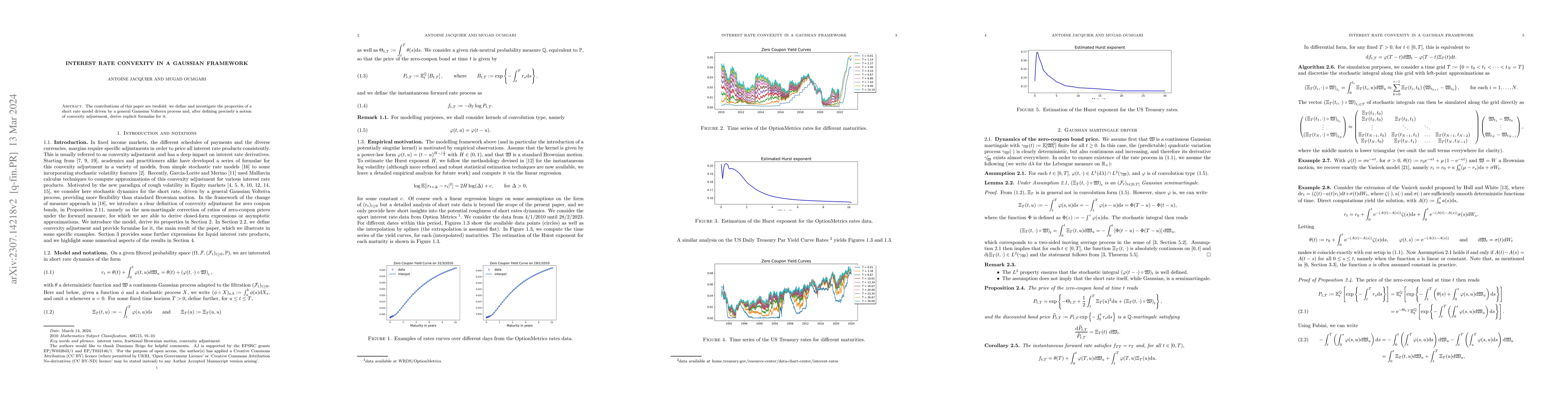

The contributions of this paper are twofold: we define and investigate the properties of a short rate model driven by a general Gaussian Volterra process and, after defining precisely a notion of co...

We propose a hybrid quantum-classical algorithm, originated from quantum chemistry, to price European and Asian options in the Black-Scholes model. Our approach is based on the equivalence between t...

We introduce a new deep-learning based algorithm to evaluate options in affine rough stochastic volatility models. Viewing the pricing function as the solution to a curve-dependent PDE (CPDE), depen...