Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce a new class of algorithms, Stochastic Generalized Method of Moments (SGMM), for estimation and inference on (overidentified) moment restriction models. Our SGMM is a novel stochastic ap...

Many economic panel and dynamic models, such as rational behavior and Euler equations, imply that the parameters of interest are identified by conditional moment restrictions. We introduce a novel i...

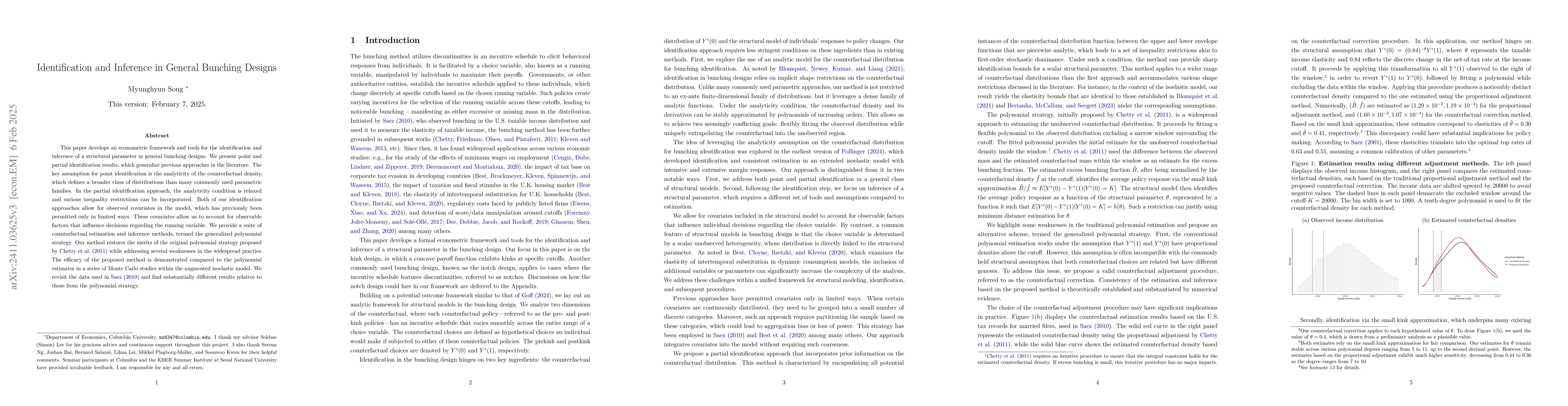

This paper develops a formal econometric framework and tools for the identification and inference of a structural parameter in general bunching designs. We present both point and partial identificatio...

We propose SLIM (Stochastic Learning and Inference in overidentified Models), a scalable stochastic approximation framework for nonlinear GMM. SLIM forms iterative updates from independent mini-batche...

We develop an empirical Bayes (EB) G-modeling framework for short-panel linear models with multidimensional heterogeneity and nonparametric prior. Specifically, we allow heterogeneous intercepts, slop...