Academic Profile

Statistics

Similar Authors

Papers on arXiv

We explore online learning in episodic loop-free Markov decision processes on non-stationary environments (changing losses and probability transitions). Our focus is on the Concave Utility Reinforce...

Many machine learning tasks can be solved by minimizing a convex function of an occupancy measure over the policies that generate them. These include reinforcement learning, imitation learning, amon...

In this paper, we propose an alternative technique to dynamic programming for solving stochastic control problems. We consider a weak formulation that is written as an optimization (minimization) pr...

Integrating renewable energy into the power grid while balancing supply and demand is a complex issue, given its intermittent nature. Demand side management (DSM) offers solutions to this challenge....

A class of finite-state and discrete-time optimal control problems is introduced. The problems involve a large number of agents with independent dynamics, which interact through an aggregative term ...

We address a large-scale and nonconvex optimization problem, involving an aggregative term. This term can be interpreted as the sum of the contributions of N agents to some common good, with N large...

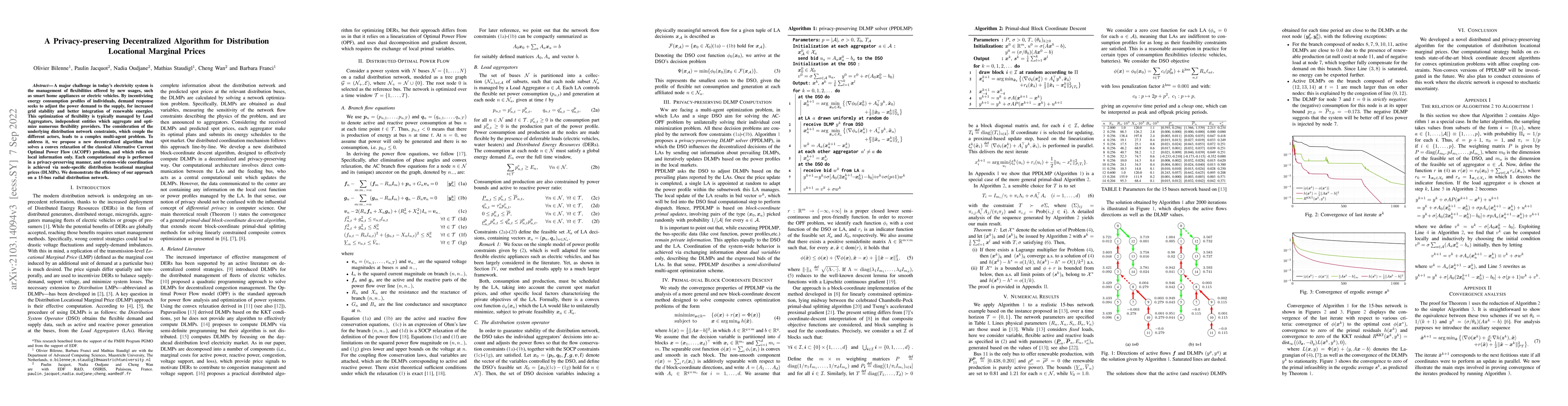

An important issue in today's electricity markets is the management of flexibilities offered by new practices, such as smart home appliances or electric vehicles. By inducing changes in the behavior...

This paper shows the existence of $\mathcal{O}(\frac{1}{n^\gamma})$-Nash equilibria in $n$-player noncooperative sum-aggregative games in which the players' cost functions, depending only on their o...

We consider the framework of convex high dimensional stochastic control problems, in which the controls are aggregated in the cost function. As first contribution, we introduce a modified problem, w...

This paper presents a partial state of the art about the topic of representation of generalized Fokker-Planck Partial Differential Equations (PDEs) by solutions of McKean Feynman-Kac Equations (MFKE...

We consider a resource allocation problem involving a large number of agents with individual constraints subject to privacy, and a central operator whose objective is to optimize a global, possibly ...

We analyze the well-posedness of a so called McKean Feynman-Kac Equation (MFKE), which is a McKean type equation with a Feynman-Kac perturbation. We provide in particular weak and strong existence c...

We present an optimization algorithm that can identify a global minimum of a potentially nonconvex smooth function with high probability, assuming the Gibbs measure of the potential satisfies a logari...

In this paper we study the exponential twist, i.e. a path-integral exponential change of measure, of a Markovian reference probability measure $\P$. This type of transformation naturally appears in va...

This paper focuses on stochastic optimal control problems with constraints in law, which are rewritten as optimization (minimization) of probability measures problem on the canonical space. We introdu...

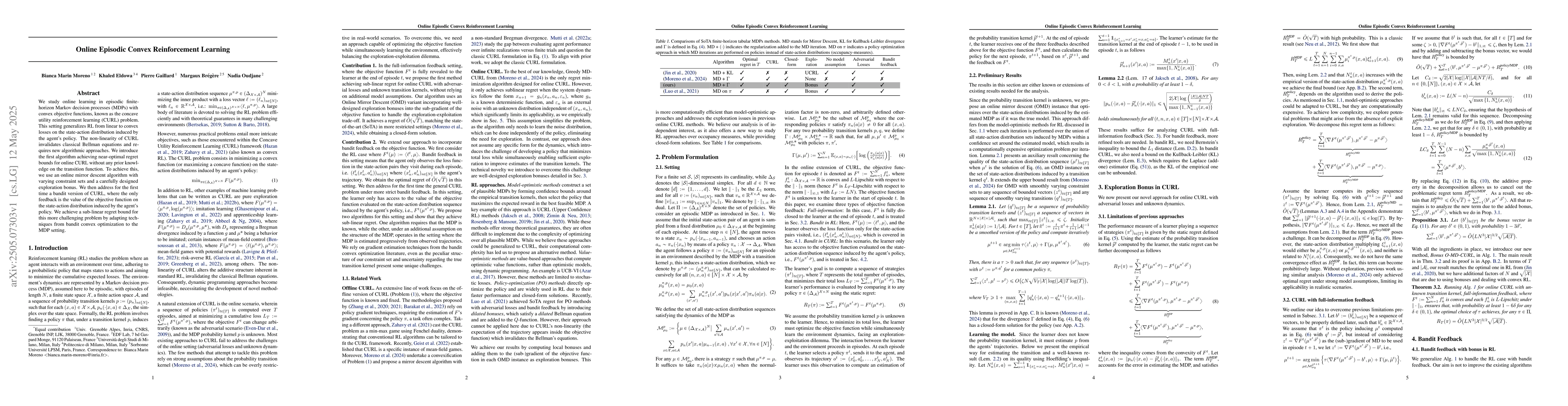

We study online learning in episodic finite-horizon Markov decision processes (MDPs) with convex objective functions, known as the concave utility reinforcement learning (CURL) problem. This setting g...

Traditional reinforcement learning usually assumes either episodic interactions with resets or continuous operation to minimize average or cumulative loss. While episodic settings have many theoretica...

We consider nonsmooth optimization problems under affine constraints, where the objective consists of the average of the component functions of a large number $N$ of agents, and we only assume access ...