Academic Profile

Statistics

Similar Authors

Papers on arXiv

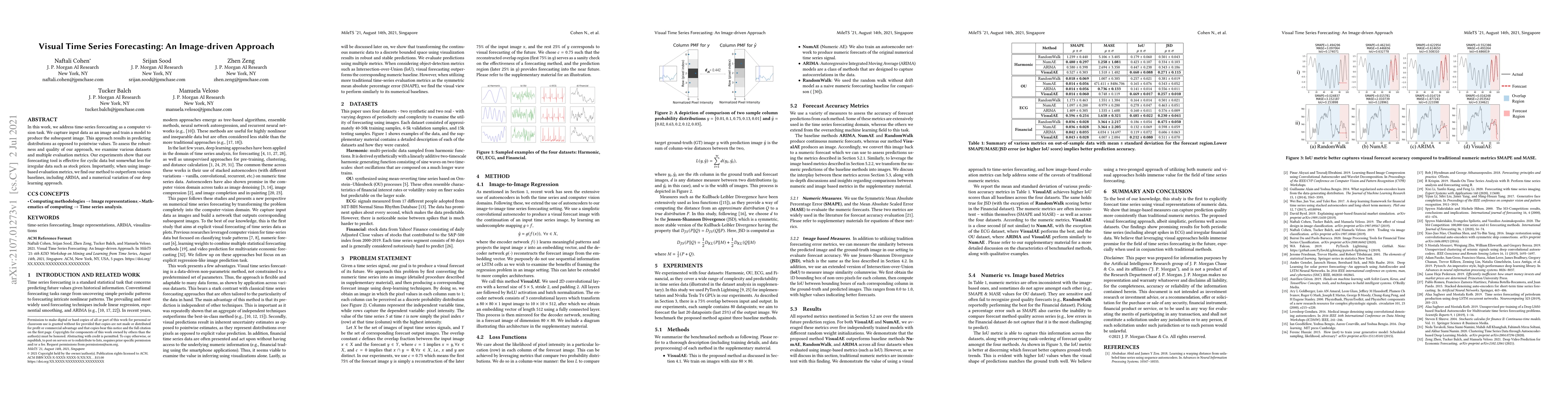

In this work, we address time-series forecasting as a computer vision task. We capture input data as an image and train a model to produce the subsequent image. This approach results in predicting d...

Companies survey their customers to measure their satisfaction levels with the company and its services. The received responses are crucial as they allow companies to assess their respective perform...

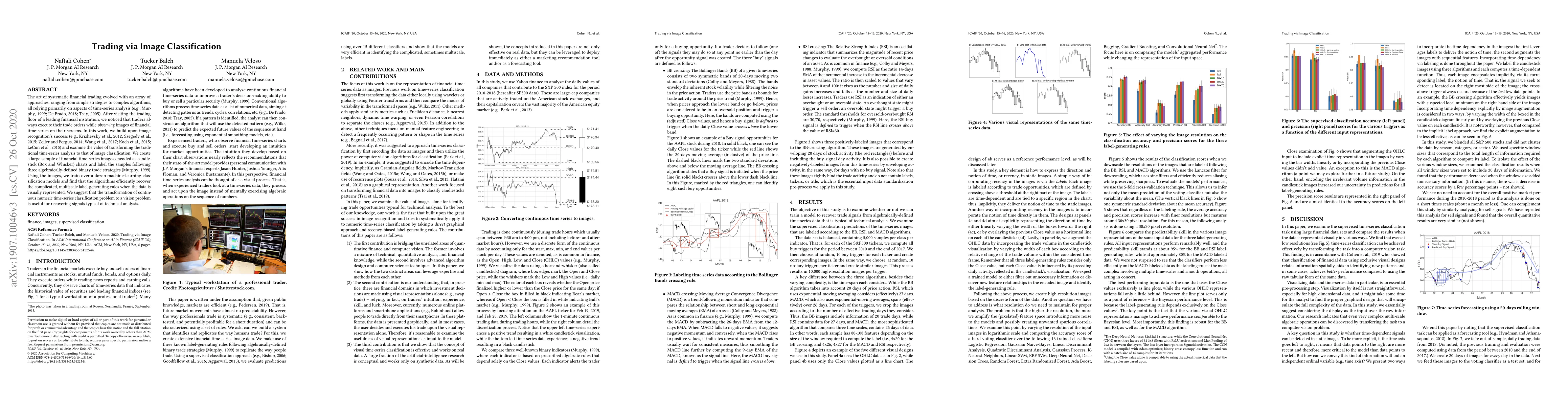

The art of systematic financial trading evolved with an array of approaches, ranging from simple strategies to complex algorithms all relying, primary, on aspects of time-series analysis. Recently, ...

Financial companies continuously analyze the state of the markets to rethink and adjust their investment strategies. While the analysis is done on the digital form of data, decisions are often made ...

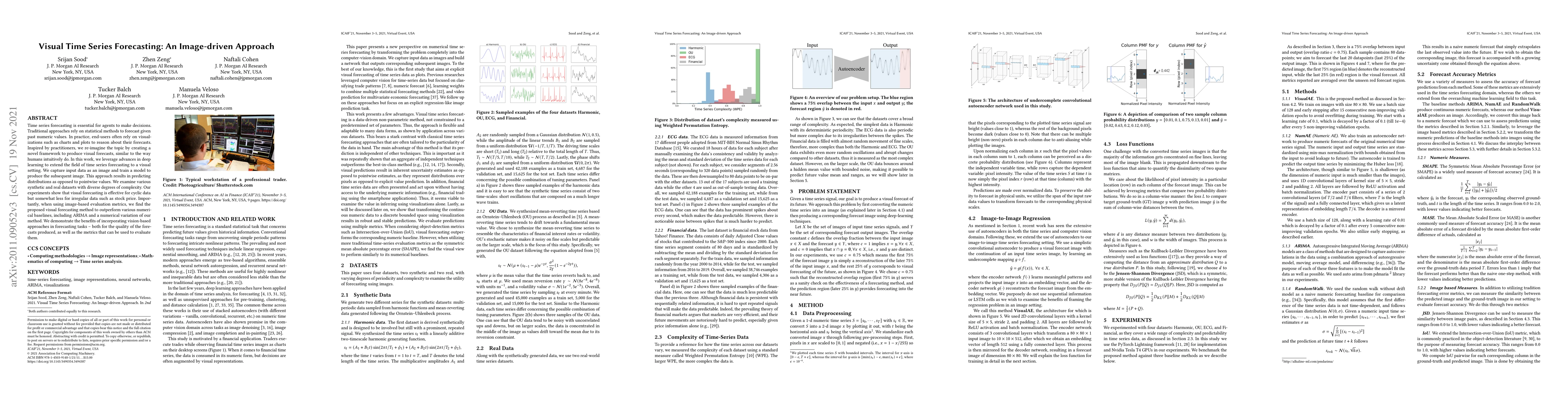

Time series forecasting is essential for agents to make decisions. Traditional approaches rely on statistical methods to forecast given past numeric values. In practice, end-users often rely on visual...

The CAPM regression is typically interpreted as if the market return contemporaneously \emph{causes} individual returns, motivating beta-neutral portfolios and factor attribution. For realized equity ...