Academic Profile

Statistics

Similar Authors

Papers on arXiv

Bootstrap percolation is a process that is used to model the spread of an infection on a given graph. In the model considered here each vertex is equipped with an individual threshold. As soon as th...

The aim of this paper is to quantify and manage systemic risk caused by default contagion in the interbank market. We model the market as a random directed network, where the vertices represent fina...

We propose a mean field control game model for the intra-and-inter-bank borrowing and lending problem. This framework allows to study the competitive game arising between groups of collaborative ban...

Bootstrap percolation in (random) graphs is a contagion dynamics among a set of vertices with certain threshold levels. The process is started by a set of initially infected vertices, and an initial...

We present a new combined \textit{mean field control game} (MFCG) problem which can be interpreted as a competitive game between collaborating groups and its solution as a Nash equilibrium between g...

We propose a new methodology for pricing options on flow forwards by applying infinite-dimensional neural networks. We recast the pricing problem as an optimization problem in a Hilbert space of rea...

We consider a network of bank holdings, where every holding has two subsidiaries of different types. A subsidiary can trade with another holding's subsidiary of the same type. Holdings support their...

We suggest a novel approach to polynomial processes solely based on a polynomial action operator. With this approach, we can analyse such processes on general state spaces, going far beyond Banach s...

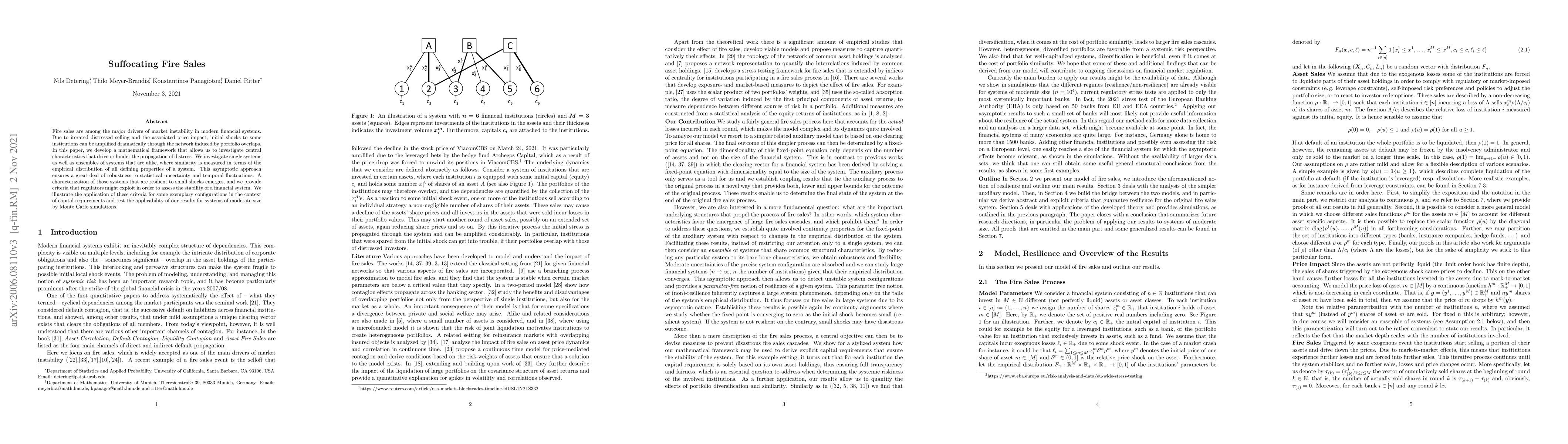

Fire sales are among the major drivers of market instability in modern financial systems. Due to iterated distressed selling and the associated price impact, initial shocks to some institutions can ...

We price European-style options written on forward contracts in a commodity market, which we model with an infinite-dimensional Heath-Jarrow-Morton (HJM) approach. For this purpose we introduce a ne...

We observe a multilinearity preserving property of conditional expectation for infinite dimensional independent increment processes defined on some abstract Banach space $B$. It is similar in nature...

We propose a particle system of diffusion processes coupled through a chain-like network structure described by an infinite-dimensional, nonlinear stochastic differential equation of McKean-Vlasov t...

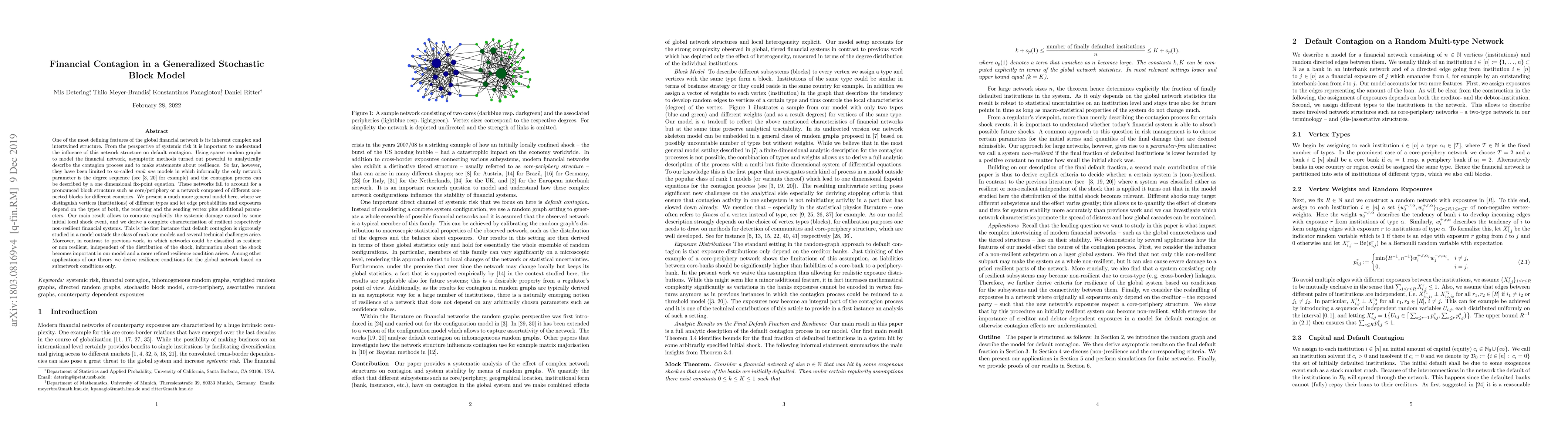

One of the most defining features of the global financial network is its inherent complex and intertwined structure. From the perspective of systemic risk it is important to understand the influence...

In this paper, we present a framework for learning the solution map of a backward parabolic Cauchy problem. The solution depends continuously but nonlinearly on the final data, source, and force terms...

We study operator learning in the context of linear propagator models for optimal order execution problems with transient price impact \`a la Bouchaud et al. (2004) and Gatheral (2010). Transient pric...

We present a dynamic model for forward curves within the Heath-Jarrow-Morton framework under the Musiela parametrization. The forward curves take values in a function space H, and their dynamics follo...

Since their introduction by Kipf and Welling in $2017$, a primary use of graph convolutional networks is transductive node classification, where missing labels are inferred within a single observed gr...

In this paper, we consider a Monte Carlo simulation method (MinMC) that approximates prices and risk measures for a range $\Gamma$ of model parameters at once. The simulation method that we study has ...