Academic Profile

Statistics

Similar Authors

Papers on arXiv

We explore the existence of a continuous marginal law with respect to the Lebesgue measure for each component $(X,Y,Z)$ of the solution to coupled quadratic forward-backward stochastic differential ...

We prove the existence of a unique Malliavin differentiable strong solution to a stochastic differential equation on the plane with merely integrable coefficients driven by the fractional Brownian s...

In this paper we are interested in a quasi-linear hyperbolic stochastic differential equation (HSPDE) when the vector field is merely bounded and measurable. Although the deterministic counterpart o...

In this paper, we consider quadratic forward-backward SDEs (QFBSDEs), for {which} the drift in the forward equation does not satisfy the standard globally Lipschitz condition and the driver of the b...

We prove path-by-path uniqueness of solution to hyperbolic stochastic partial differential equations when the drift coefficient is the difference of two componentwise monotone Borel measurable funct...

In this work, we generalise the stochastic local time space integration introduced in \cite{Ei00} to the case of Brownian sheet. %We develop a stochastic local time-space calculus with respect to th...

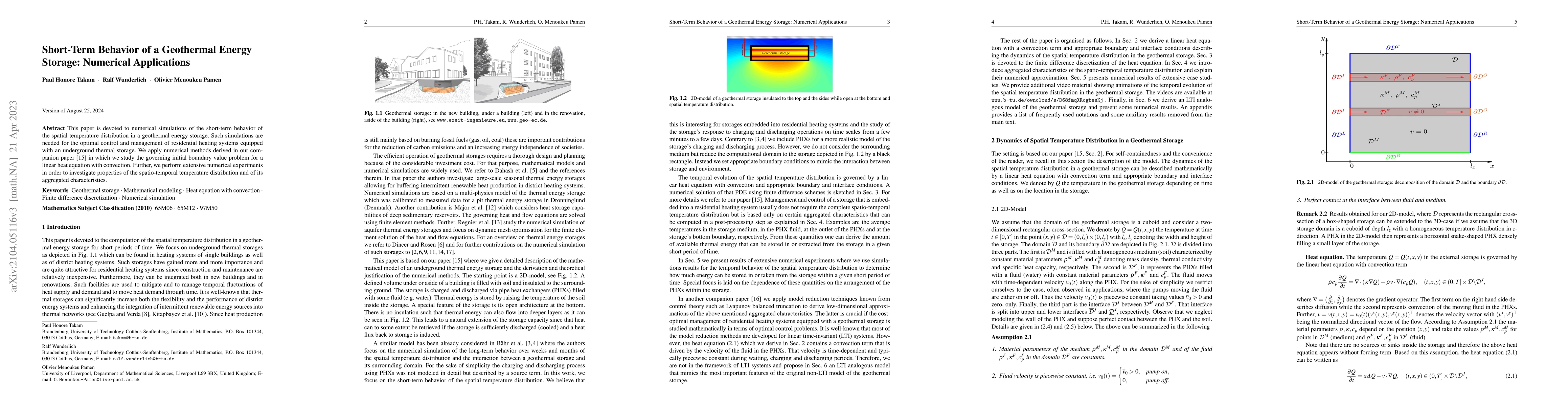

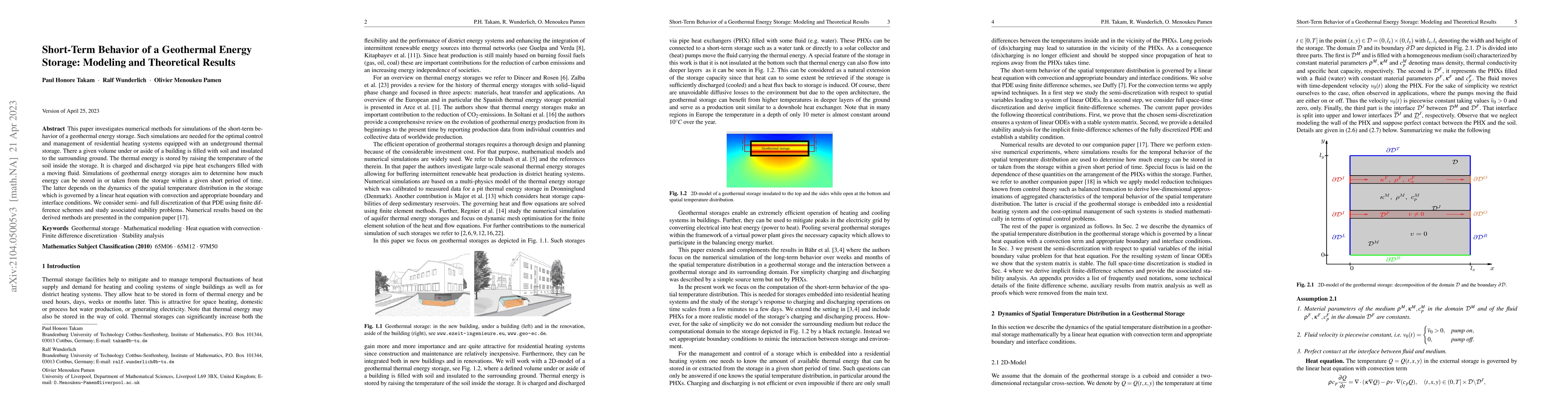

This paper is devoted to numerical simulations of the short-term behavior of the spatial temperature distribution in a geothermal energy storage. Such simulations are needed for the optimal control ...

This paper investigates numerical methods for simulations of the short-term behavior of a geothermal energy storage. Such simulations are needed for the optimal control and management of residential...

In this paper, we investigate a complex variation of the standard joint life annuity policy by introducing three distinct contingent benefits for the surviving member(s) of a couple, along with a cont...

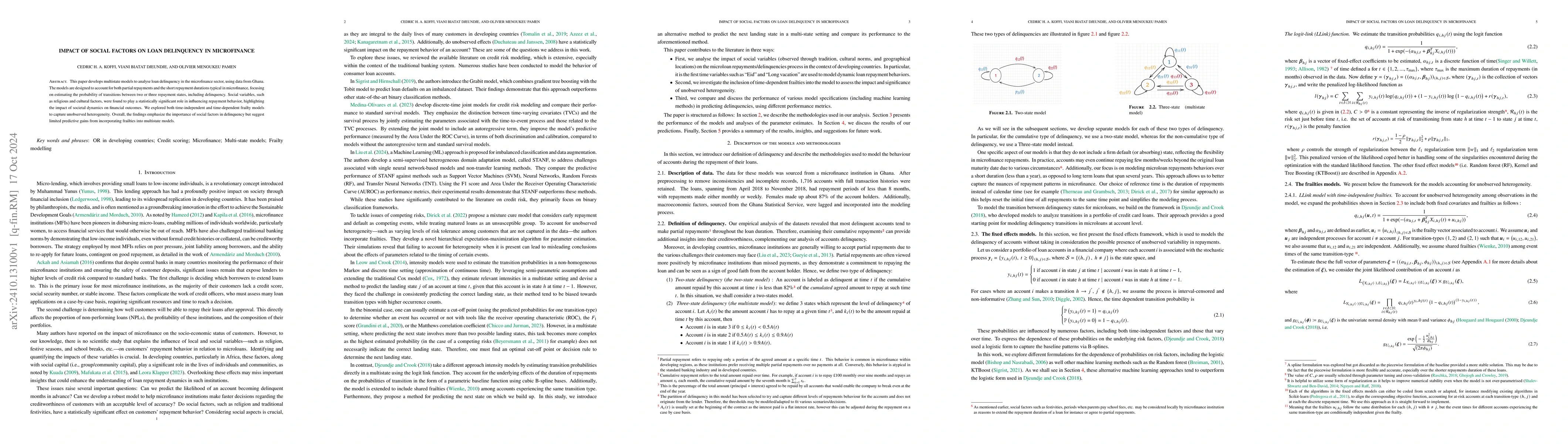

This paper develops multistate models to analyse loan delinquency in the microfinance sector, using data from Ghana. The models are designed to account for both partial repayments and the short repaym...

We investigate the convergence rate for the time discretization of a class of quadratic backward SDEs -- potentially involving path-dependent terminal values -- when coupled with non-standard Lipschit...

In this paper, we study the problem of stochastic optimal control for systems governed by stochastic differential equations (SDEs) with drift coefficients of bounded variation. We establish both neces...