Academic Profile

Statistics

Similar Authors

Papers on arXiv

Training an effective deep learning model to learn ocean processes involves careful choices of various hyperparameters. We leverage the advanced search algorithms for multiobjective optimization in ...

For a covariance matrix coming from a factor model of returns, we investigate the relationship between the long-only global minimum variance portfolio and the asset exposures to the factors. In the ca...

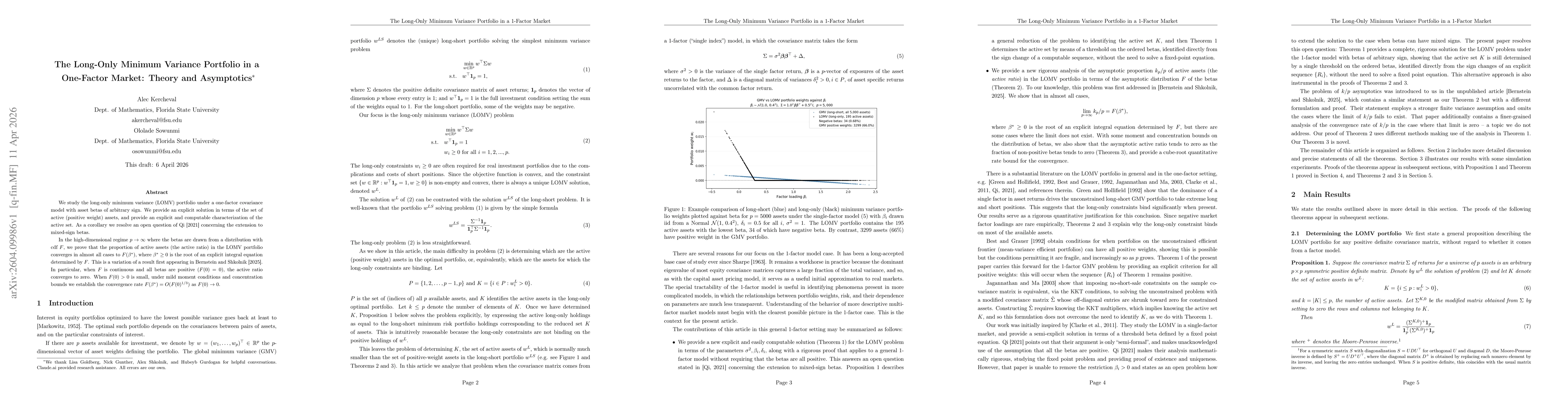

We study the long-only minimum variance (LOMV) portfolio under a one-factor covariance model with asset betas of arbitrary sign. We provide an explicit solution in terms of the set of active (positi...