Academic Profile

Statistics

Similar Authors

Papers on arXiv

A key task in actuarial modelling involves modelling the distributional properties of losses. Classic (distributional) regression approaches like Generalized Linear Models (GLMs; Nelder and Wedderbu...

The Hawkes process is a model for counting the number of arrivals to a system which exhibits the self-exciting property - that one arrival creates a heightened chance of further arrivals in the near...

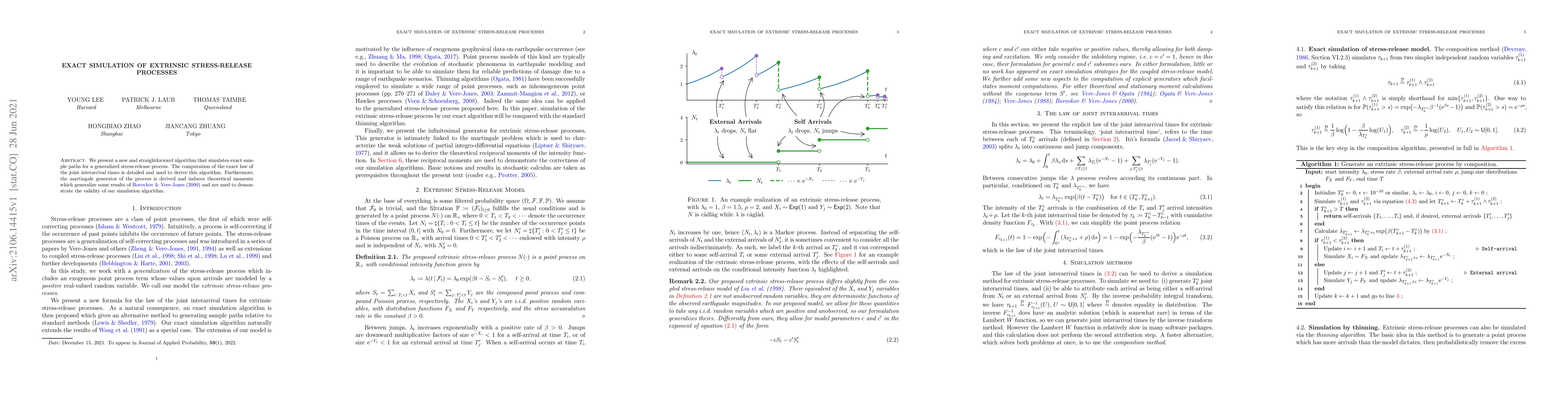

We present a new and straightforward algorithm that simulates exact sample paths for a generalized stress-release process. The computation of the exact law of the joint interarrival times is detaile...

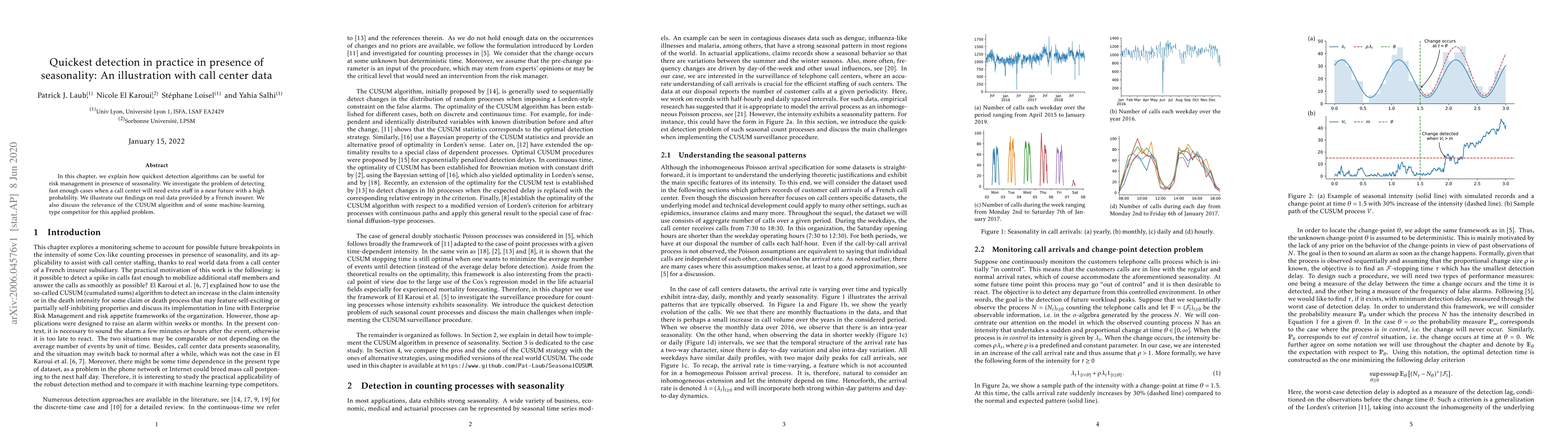

In this chapter, we explain how quickest detection algorithms can be useful for risk management in presence of seasonality. We investigate the problem of detecting fast enough cases when a call cent...

A numerical method is proposed to evaluate the survival function of a compound distribution and the stop-loss premiums associated with a non-proportional global reinsurance treaty. The method relies...

In this paper, we consider catastrophe stop-loss reinsurance valuation for a reinsurance company with dynamic contagion claims. To deal with conventional and emerging catastrophic events, we propose t...

This paper introduces the Actuarial Neural Additive Model, an inherently interpretable deep learning model for general insurance pricing that offers fully transparent and interpretable results while r...