Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider scalar ODE with a power singularity at the origin, regularized by an additive fractional noise. We show that, as the intensity in front of the noise goes to $0$, the solution converges t...

Inspired by recent advances in singular SPDE theory, we use the Poincar\'e inequality on Wiener space to show that controlled complementary Young regularity is sufficient to obtain Gaussian rough pa...

The long-time behavior of stochastic Hamilton-Jacobi equations is analyzed, including the stochastic mean curvature flow as a special case. In a variety of settings, new and sharpened results are ob...

We obtain well-posedness results for a class of ODE with a singular drift and additive fractional noise, whose right-hand-side involves some bounded variation terms depending on the solution. Exampl...

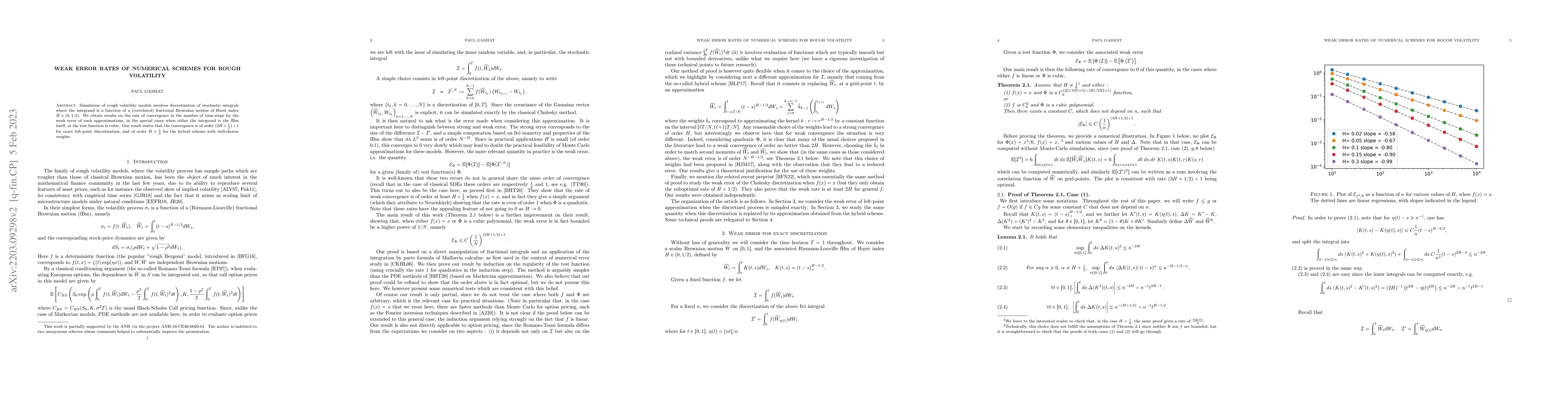

Simulation of rough volatility models involves discretization of stochastic integrals where the integrand is a function of a (correlated) fractional Brownian motion of Hurst index $H \in (0,1/2)$. W...

We generalize the notion of pathwise viscosity solutions, put forward by Lions and Souganidis to study fully nonlinear stochastic partial differential equations, to equations set on a sub-domain wit...

In [Precise Asymptotics for Robust Stochastic Volatility Models; Ann. Appl. Probab. 2021] we introduce a new methodology to analyze large classes of (classical and rough) stochastic volatility model...

We give an example of a reflected diffferential equation which may have infinitely many solutions if the driving signal is rough enough (e.g. of infinite $p$-variation, for some $p>2$). For this equ...

We present a new methodology to analyze large classes of (classical and rough) stochastic volatility models, with special regard to short-time and small noise formulae for option prices. Our main to...

We consider the (sub-Riemannian type) control problem of finding a path going from an initial point $x$ to a target point $y$, by only moving in certain admissible directions. We assume that the corre...

We study the martingale property and moment explosions of a signature volatility model, where the volatility process of the log-price is given by a linear form of the signature of a time-extended Brow...

We show that Young translation has dense orbits in the space of rough paths: for any two geometric rough paths, one can translate the first by a sequence of smooth paths so that it converges to the se...