Academic Profile

Statistics

Similar Authors

Papers on arXiv

We seek to extract a small number of representative scenarios from large and high-dimensional panel data that are consistent with sample moments. Among two novel algorithms, the first identifies sce...

We consider portfolio selection under nonparametric $\alpha$-maxmin ambiguity in the neighbourhood of a reference distribution. We show strict concavity of the portfolio problem under ambiguity aver...

We develop a new framework for embedding joint probability distributions in tensor product reproducing kernel Hilbert spaces (RKHS). Our framework accommodates a low-dimensional, normalized and posi...

We develop a non-negative polynomial minimum-norm likelihood ratio (PLR) of two distributions of which only moments are known. The sample PLR converges to the unknown population PLR under mild condi...

We propose a novel nonparametric kernel-based estimator of cross-sectional conditional mean and covariance matrices for large unbalanced panels. We show its consistency and provide finite-sample guara...

We study conditional linear factor models in the context of asset pricing panels. Our analysis focuses on conditional means and covariances to characterize the cross-sectional and inter-temporal prope...

We introduce kernel density machines (KDM), a novel density ratio estimator in a reproducing kernel Hilbert space setting. KDM applies to general probability measures on countably generated measurable...

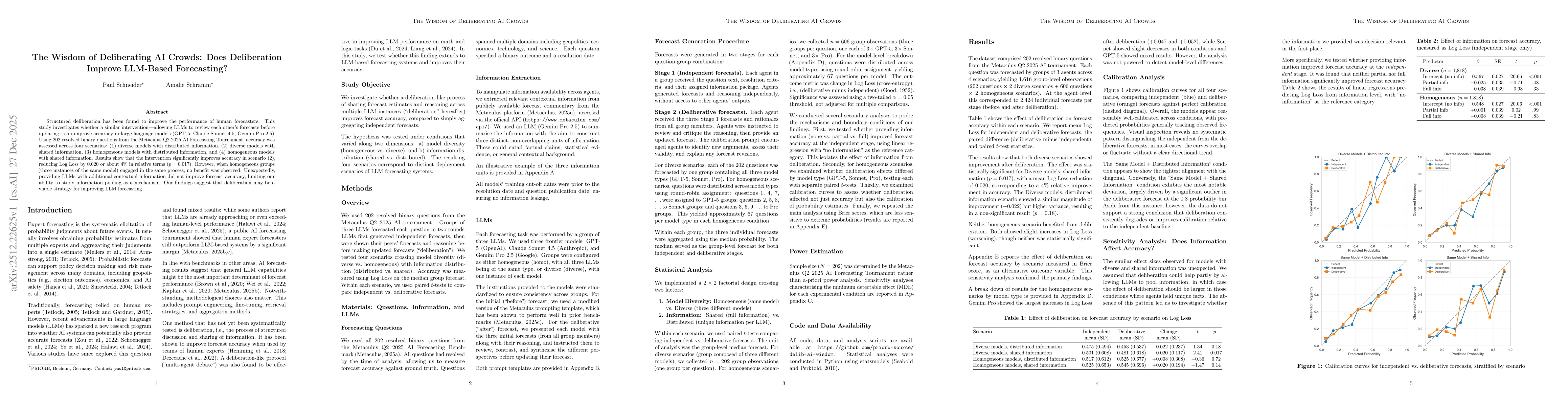

Structured deliberation has been found to improve the performance of human forecasters. This study investigates whether a similar intervention, i.e. allowing LLMs to review each other's forecasts befo...

This paper introduces a novel parameter free skewness coefficient for fuzzy numbers, addressing a critical gap in quantifying asymmetry under imprecision. Existing fuzzy literature substitutes members...

We propose a scalable and theoretically grounded low-rank conditional expectation model for recursive Monte Carlo optimal stopping problems, in particular American option pricing. Our method reformula...