Academic Profile

Statistics

Similar Authors

Papers on arXiv

We develop a model for the long-term dynamics of electricity market, based on mean-field games of optimal stopping. Our paper extends the recent contribution [A\"id, Ren\'e, Roxana Dumitrescu, and P...

We build a model of a financial market where a large number of firms determine their dynamic emission strategies under climate transition risk in the presence of both green-minded and neutral invest...

We study the impact of transition scenario uncertainty, namely that of future carbon price and electricity demand, on the pace of decarbonization of the electricity industry. To this end, we develop...

The standard Hotelling model assumes that the stock of an exhaustible resource is known. We expand on the model by Arrow and Chang that introduced stochastic discoveries and for the first time compl...

We develop the fictitious play algorithm in the context of the linear programming approach for mean field games of optimal stopping and mean field games with regular control and absorption. This alg...

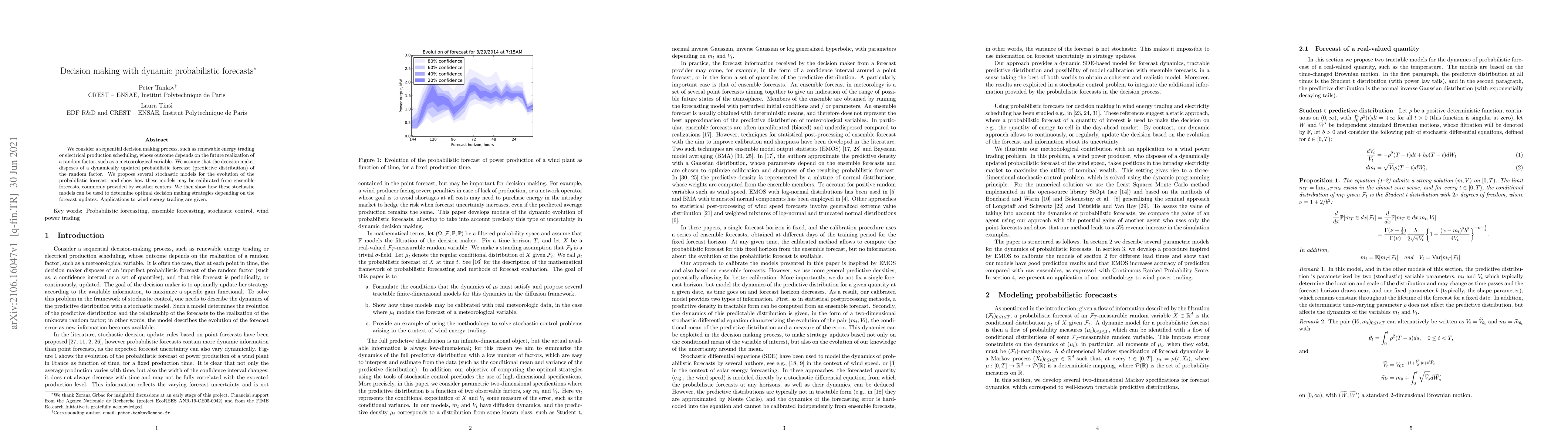

We consider a sequential decision making process, such as renewable energy trading or electrical production scheduling, whose outcome depends on the future realization of a random factor, such as a ...

In this chapter we first briefly review the existing approaches to hedging in rough volatility models. Next, we present a simple but general result which shows that in a one-factor rough stochastic ...

We develop the linear programming approach to mean-field games in a general setting. This relaxed control approach allows to prove existence results under weak assumptions, and lends itself well to ...

We study price formation in intraday electricity markets in the presence of intermittent renewable generation. We consider the setting where a major producer may interact strategically with a large ...

We develop a tractable equilibrium model for price formation in intraday electricity markets in the presence of intermittent renewable generation. Using stochastic control theory, we identify the op...

We develop a model for the industry dynamics in the electricity market, based on mean-field games of optimal stopping. In our model, there are two types of agents: the renewable producers and the co...

We consider the mean-field game where each agent determines the optimal time to exit the game by solving an optimal stopping problem with reward function depending on the density of the state proces...

We study a problem of optimal irreversible investment and emission reduction formulated as a nonzero-sum dynamic game between an investor with environmental preferences and a firm. The game is set in ...

Aiming to analyze the impact of environmental transition on the value of assets and on asset stranding, we study optimal stopping and divestment timing decisions for an economic agent whose future rev...

We study the price impact of storage facilities in electricity markets and analyze the long-term profitability of these facilities in prospective scenarios of energy transition. To this end, we begin ...

Climate Finance Bench introduces an open benchmark that targets question-answering over corporate climate disclosures using Large Language Models. We curate 33 recent sustainability reports in English...

We introduce a new mean-field game framework to analyze the impact of carbon pricing in a multi-sector economy with defaultable firms. Each sector produces a homogeneous good, with its price endogenou...