Academic Profile

Statistics

Similar Authors

Papers on arXiv

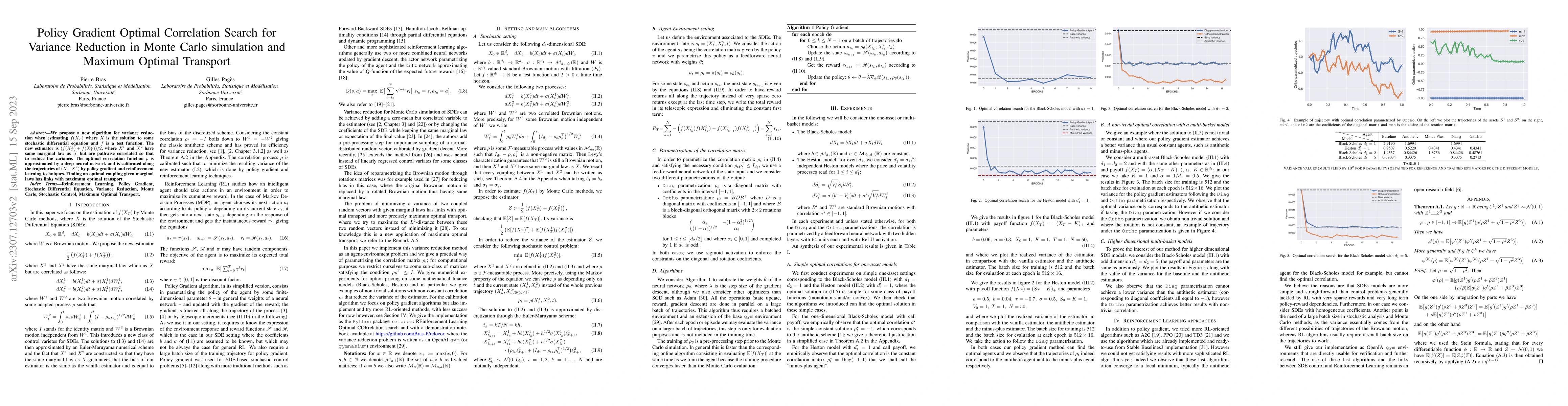

We propose a new algorithm for variance reduction when estimating $f(X_T)$ where $X$ is the solution to some stochastic differential equation and $f$ is a test function. The new estimator is $(f(X^1...

For $V : \mathbb{R}^d \to \mathbb{R}$ coercive, we study the convergence rate for the $L^1$-distance of the empiric minimizer, which is the true minimum of the function $V$ sampled with noise with a...

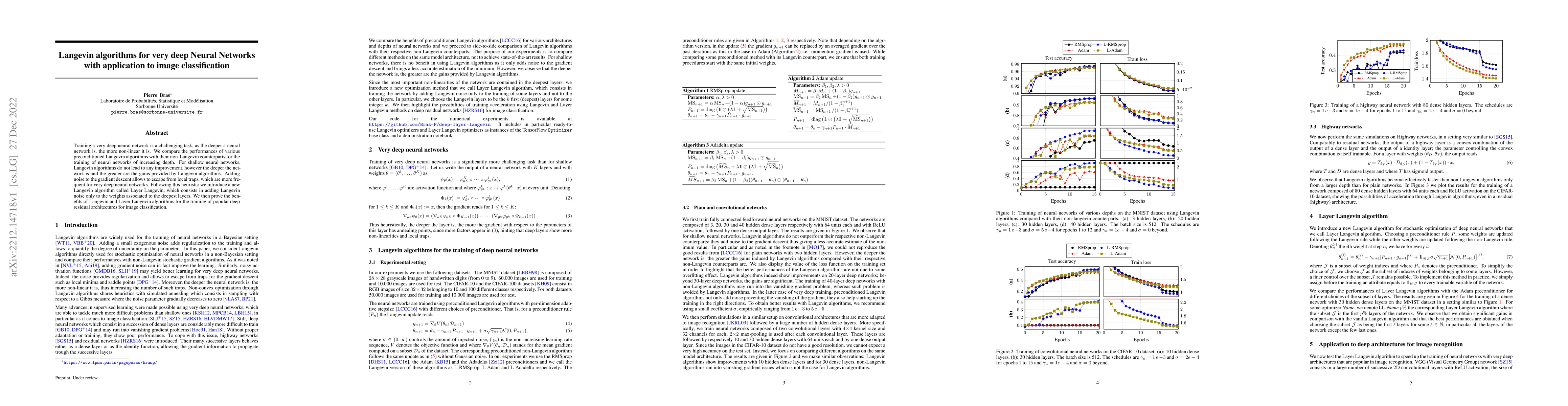

Training a very deep neural network is a challenging task, as the deeper a neural network is, the more non-linear it is. We compare the performances of various preconditioned Langevin algorithms wit...

Stochastic Gradient Descent Langevin Dynamics (SGLD) algorithms, which add noise to the classic gradient descent, are known to improve the training of neural networks in some cases where the neural ...

We study the convergence of Langevin-Simulated Annealing type algorithms with multiplicative noise, i.e. for $V : \mathbb{R}^d \to \mathbb{R}$ a potential function to minimize, we consider the stoch...

We give bounds for the total variation distance between the solutions to two stochastic differential equations starting at the same point and with close coefficients, which applies in particular to ...

We study the convergence of Langevin-Simulated Annealing type algorithms with multiplicative noise, i.e. for $V : \mathbb{R}^d \to \mathbb{R}$ a potential function to minimize, we consider the stoch...

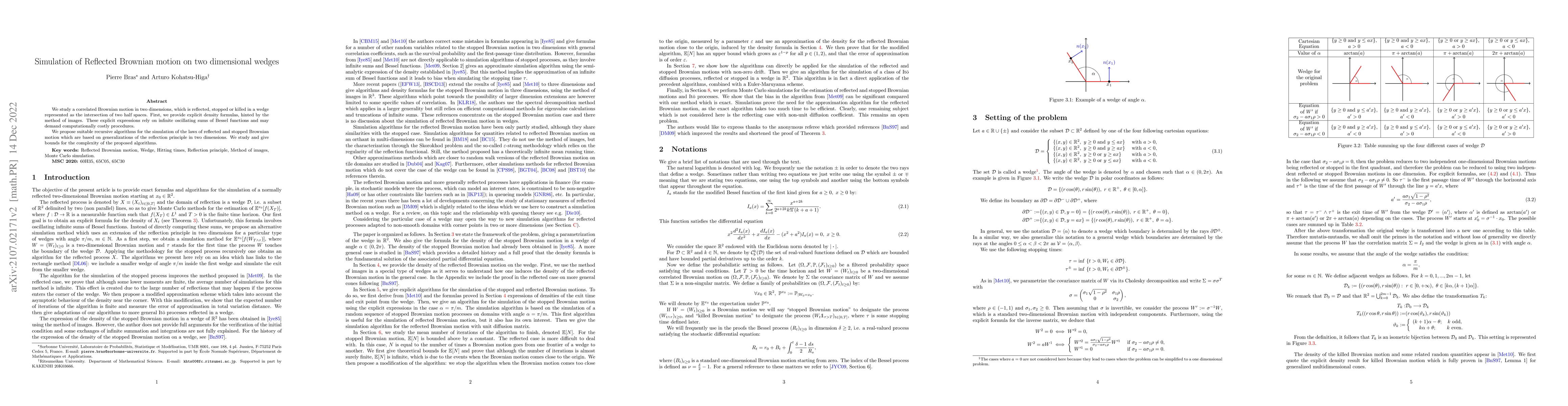

We study a correlated Brownian motion in two dimensions, which is reflected, stopped or killed in a wedge represented as the intersection of two half spaces. First, we provide explicit density formu...

We study convergence rates for Gibbs measures, with density proportional to $e^{-f(x)/t}$, as $t \rightarrow 0$ where $f : \mathbb{R}^d \rightarrow \mathbb{R}$ admits a unique global minimum at $x^\...