2

arXiv Papers

4

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

4

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Application of Tensor Neural Networks to Pricing Bermudan Swaptions

The Cheyette model is a quasi-Gaussian volatility interest rate model widely used to price interest rate derivatives such as European and Bermudan Swaptions for which Monte Carlo simulation has beco...

arXiv

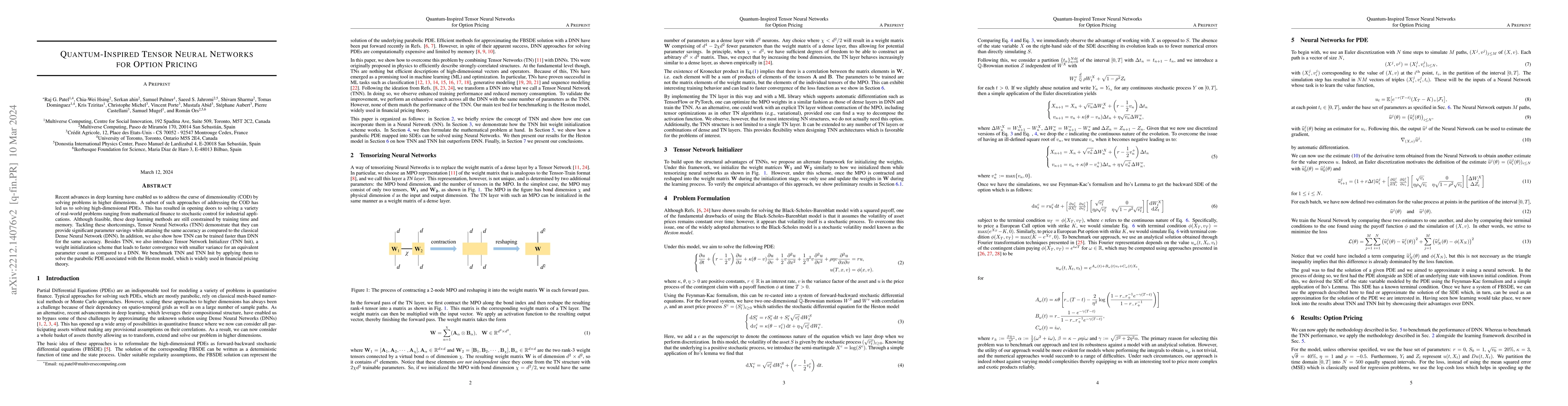

Quantum-Inspired Tensor Neural Networks for Option Pricing

Recent advances in deep learning have enabled us to address the curse of dimensionality (COD) by solving problems in higher dimensions. A subset of such approaches of addressing the COD has led us t...