Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose a novel generative model for multivariate discrete-time time series data. Drawing inspiration from the construction of neural spline flows, our algorithm incorporates linear transformatio...

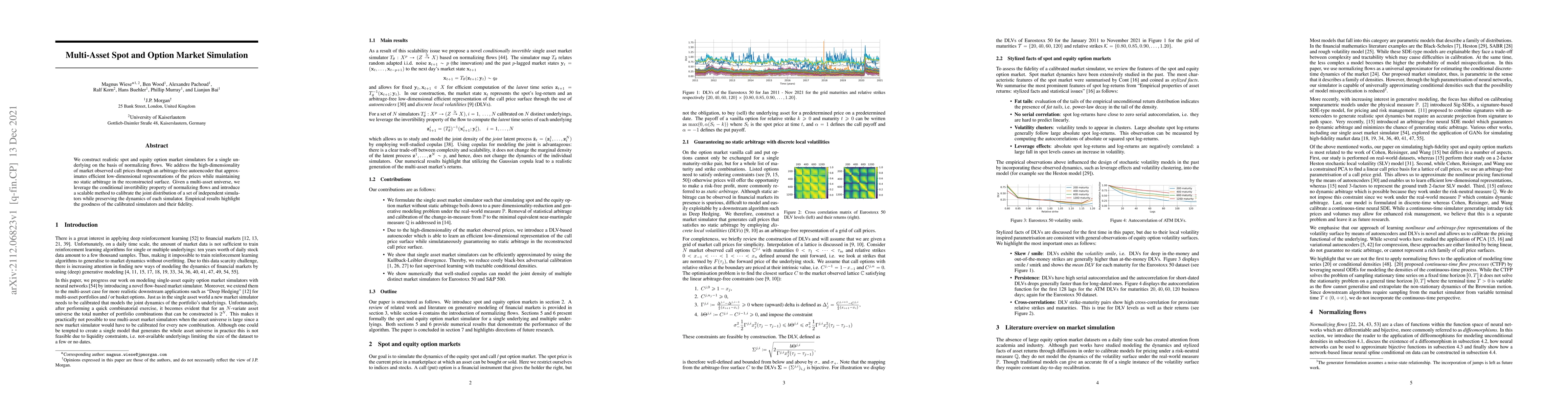

We construct realistic spot and equity option market simulators for a single underlying on the basis of normalizing flows. We address the high-dimensionality of market observed call prices through a...

Estimation of the value-at-risk (VaR) of a large portfolio of assets is an important task for financial institutions. As the joint log-returns of asset prices can often be projected to a latent spac...

In this paper we introduce a new concept for modelling electricity prices through the introduction of an unobservable intrinsic electricity price $p(\tau)$. We use it to connect the classical theory...

We consider a variational autoencoder (VAE) for binary data. Our main innovations are an interpretable lower bound for its training objective, a modified initialization and architecture of such a VA...

Birth rates have dramatically decreased and, with continuous improvements in life expectancy, pension expenditure is on an irreversibly increasing path. This will raise serious concerns for the sust...

Under the Solvency II regime, life insurance companies are asked to derive their solvency capital requirements from the full loss distributions over the coming year. Since the industry is currently ...

Modeling financial time series by stochastic processes is a challenging task and a central area of research in financial mathematics. As an alternative, we introduce Quant GANs, a data-driven model ...

Deep generative networks such as GANs and normalizing flows flourish in the context of high-dimensional tasks such as image generation. However, so far exact modeling or extrapolation of distributio...