Academic Profile

Statistics

Similar Authors

Papers on arXiv

Competition between times series often arises in sales prediction, when similar products are on sale on a marketplace. This article provides a model of the presence of cannibalization between times ...

Concentration inequalities are widely used for analyzing machine learning algorithms. However, current concentration inequalities cannot be applied to some of the most popular deep neural networks, ...

We revisit the interest of classical statistical techniques for sales forecasting like exponential smoothing and extensions thereof (as Holt's linear trend method). We do so by considering ensemble ...

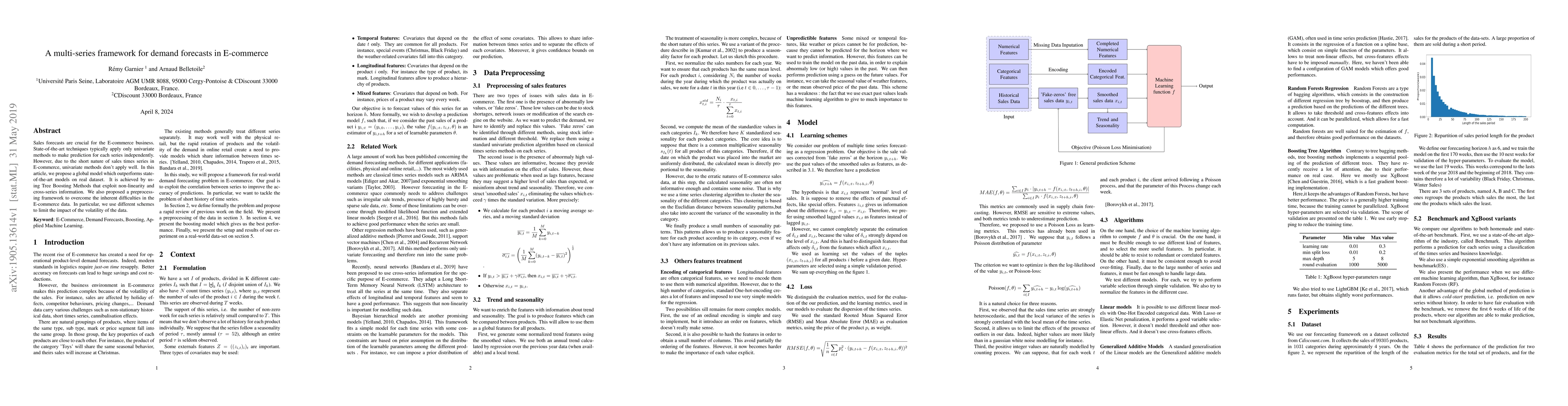

Sales forecasts are crucial for the E-commerce business. State-of-the-art techniques typically apply only univariate methods to make prediction for each series independently. However, due to the sho...

We propose a vector auto-regressive (VAR) model with a low-rank constraint on the transition matrix. This new model is well suited to predict high-dimensional series that are highly correlated, or t...