Academic Profile

Statistics

Similar Authors

Papers on arXiv

"The rich are getting richer" implies that the population income distributions are getting more right skewed and heavily tailed. For such distributions, the mean is not the best measure of the cente...

To accommodate numerous practical scenarios, in this paper we extend statistical inference for smoothed quantile estimators from finite domains to infinite domains. We accomplish the task with the h...

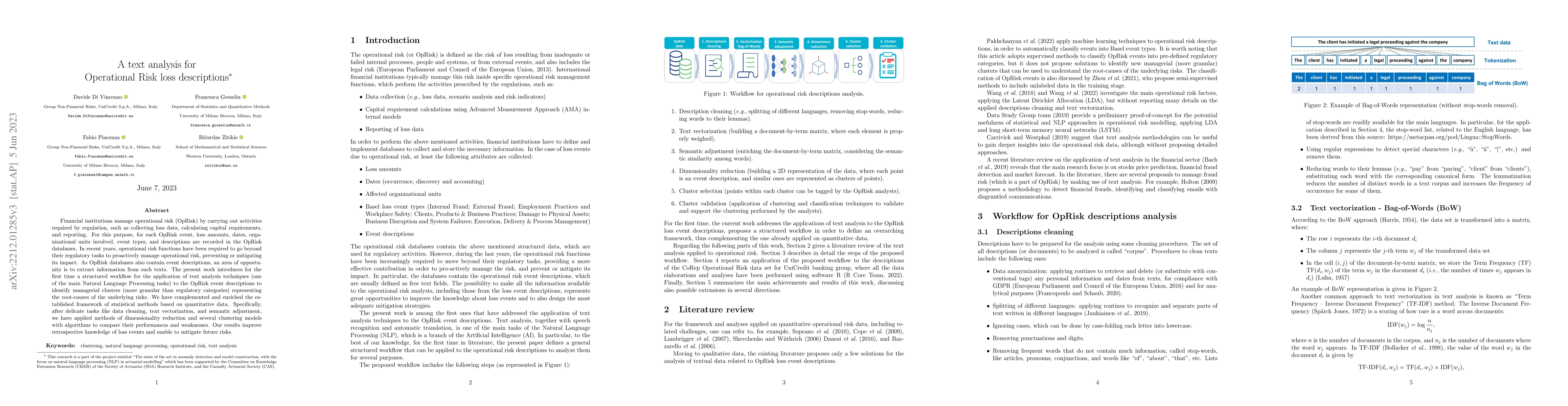

Financial institutions manage operational risk (OpRisk) by carrying out activities required by regulation, such as collecting loss data, calculating capital requirements, and reporting. For this pur...

This paper offers a mathematical invention that shows how to convert integrated quantiles, which often appear in risk measures, into integrated cumulative distribution functions, which are technical...

The Expected Shortfall (ES) is one of the most important regulatory risk measures in finance, insurance, and statistics, which has recently been characterized via sets of axioms from perspectives of...

Zero factorial, defined to be one, is often counterintuitive to students but nonetheless an interesting concept to convey in a classroom environment. The challenge is to delineate the concept in a s...

The classical notion of comonotonicity has played a pivotal role when solving diverse problems in economics, finance, and insurance. In various practical problems, however, this notion of extreme po...