Academic Profile

Statistics

Similar Authors

Papers on arXiv

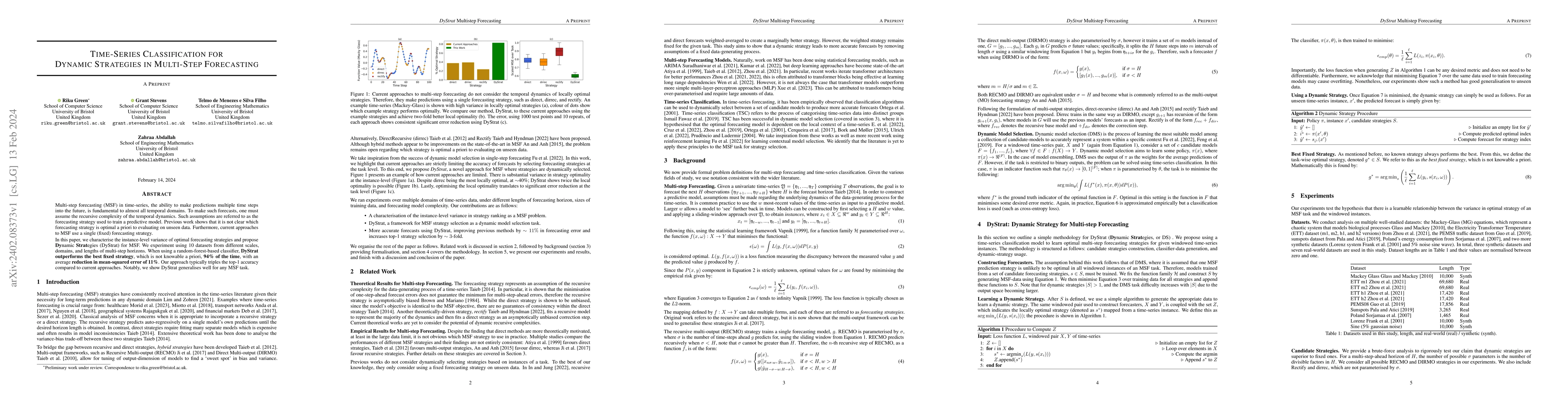

Multi-step forecasting (MSF) in time-series, the ability to make predictions multiple time steps into the future, is fundamental to almost all temporal domains. To make such forecasts, one must assu...

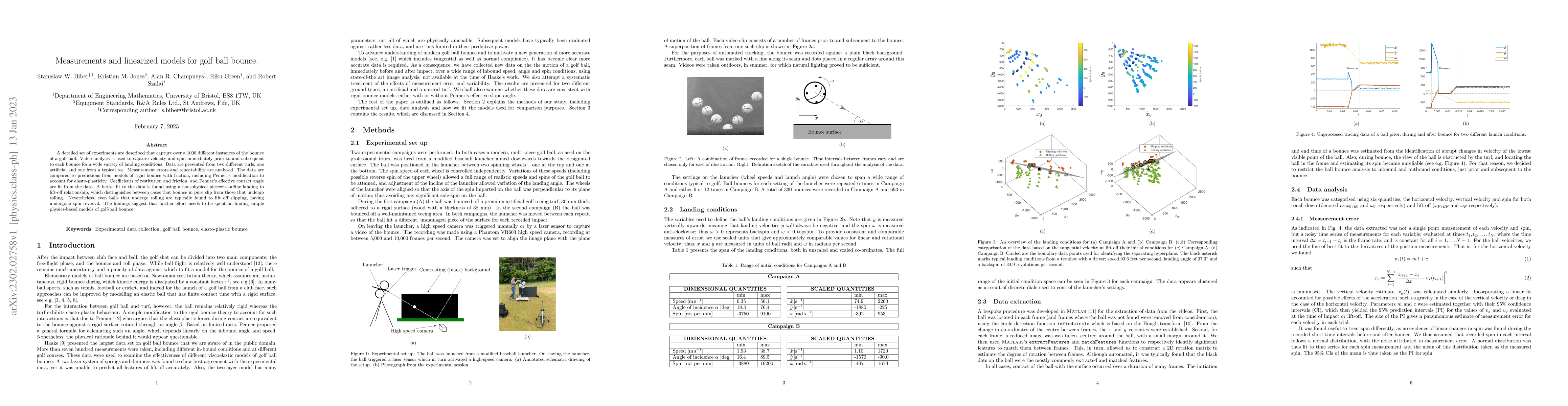

A detailed set of experiments are described that capture over a 1000 different instances of the bounce of a golf ball. Video analysis is used to capture velocity and spin immediately prior to and su...

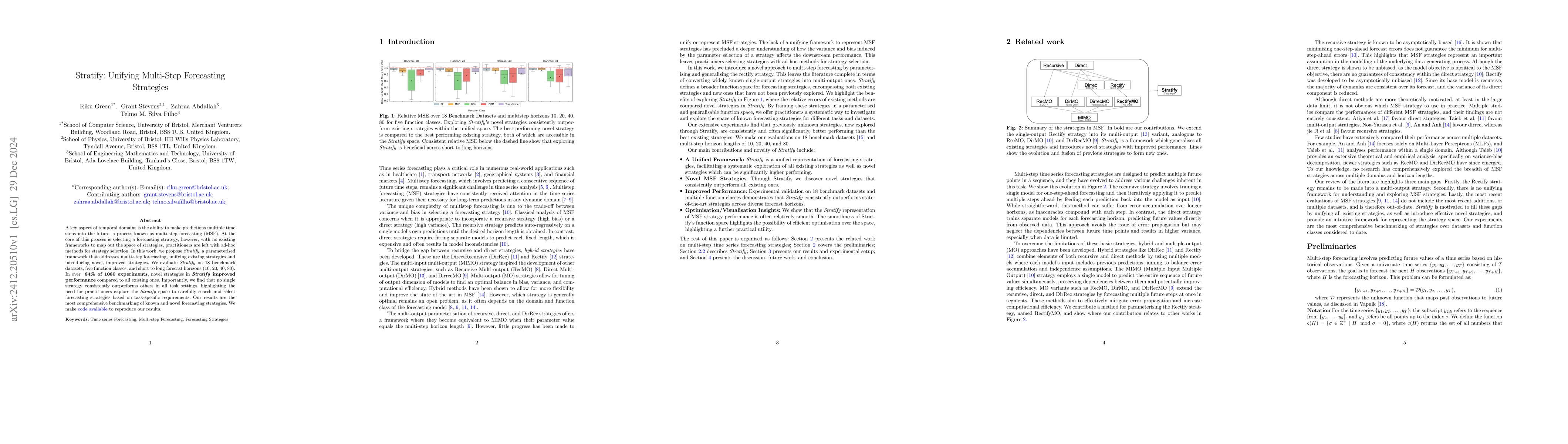

A key aspect of temporal domains is the ability to make predictions multiple time steps into the future, a process known as multi-step forecasting (MSF). At the core of this process is selecting a for...

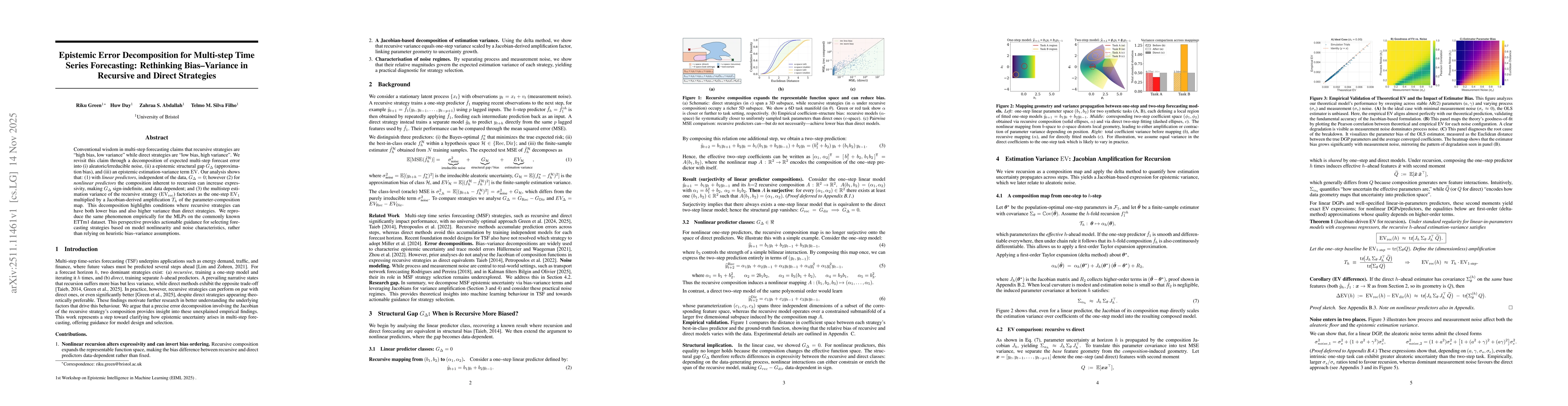

Multi-step forecasting is often described through a simple rule of thumb: recursive strategies are said to have high bias and low variance, while direct strategies are said to have low bias and high v...

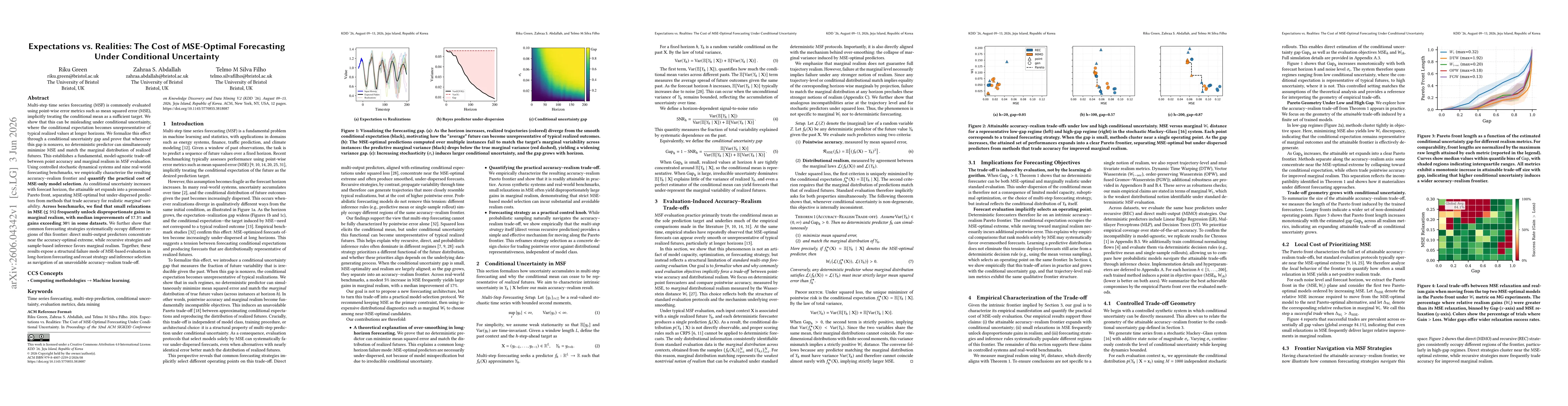

Multi-step time series forecasting (MSF) is commonly evaluated using point-wise error metrics such as mean squared error (MSE), implicitly treating the conditional mean as a sufficient target. We show...

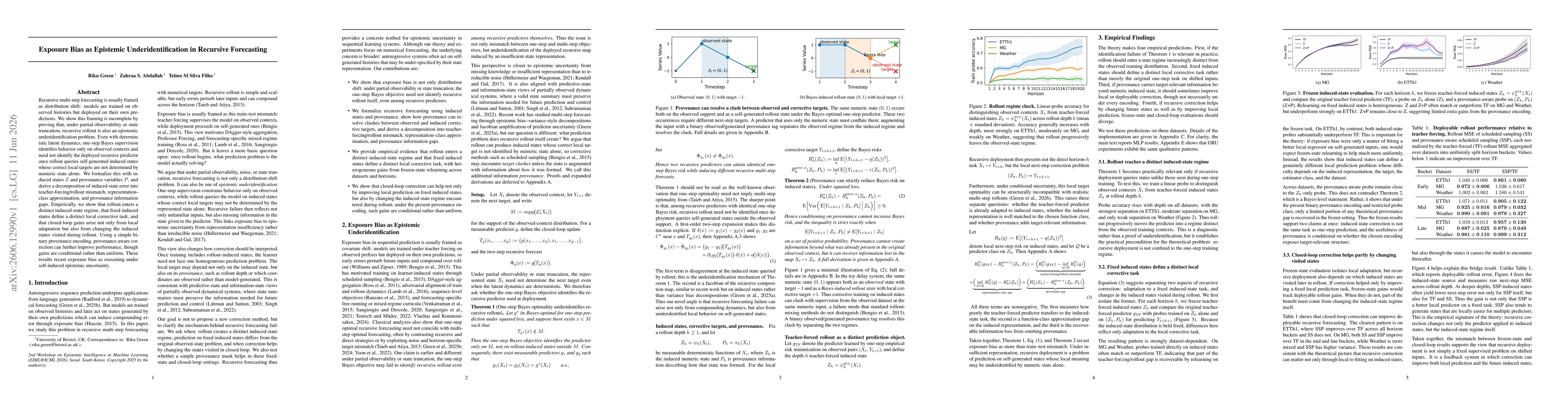

Recursive multi-step forecasting is usually framed as distribution shift: models are trained on observed histories but deployed on their own predictions. We show this framing is incomplete by proving ...

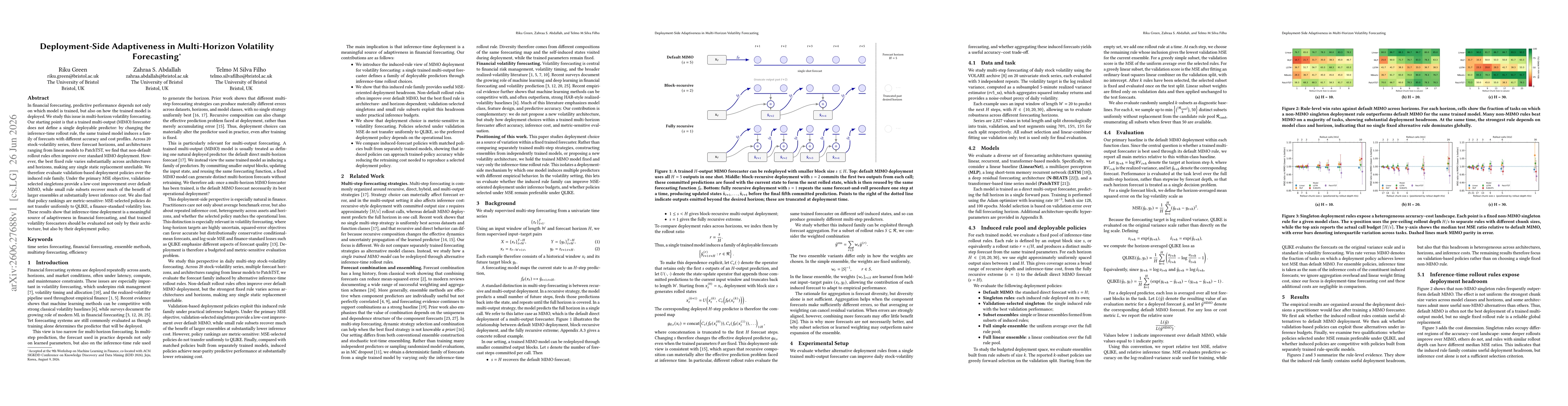

In financial forecasting, predictive performance depends not only on which model is trained, but also on how the trained model is deployed. We study this issue in multi-horizon volatility forecasting....