Academic Profile

Statistics

Similar Authors

Papers on arXiv

Particle Markov Chain Monte Carlo methods are used to carry out inference in non-linear and non-Gaussian state space models, where the posterior density of the states is approximated using particles...

Speeding up Markov Chain Monte Carlo (MCMC) for datasets with many observations by data subsampling has recently received considerable attention. A pseudo-marginal MCMC method is proposed that estim...

Directed acyclic graph (DAG) learning is a rapidly expanding field of research. Though the field has witnessed remarkable advances over the past few years, it remains statistically and computational...

We provide a simple and general solution to the fundamental open problem of inaccurate uncertainty quantification of Bayesian inference in misspecified or approximate models, and of generalized Baye...

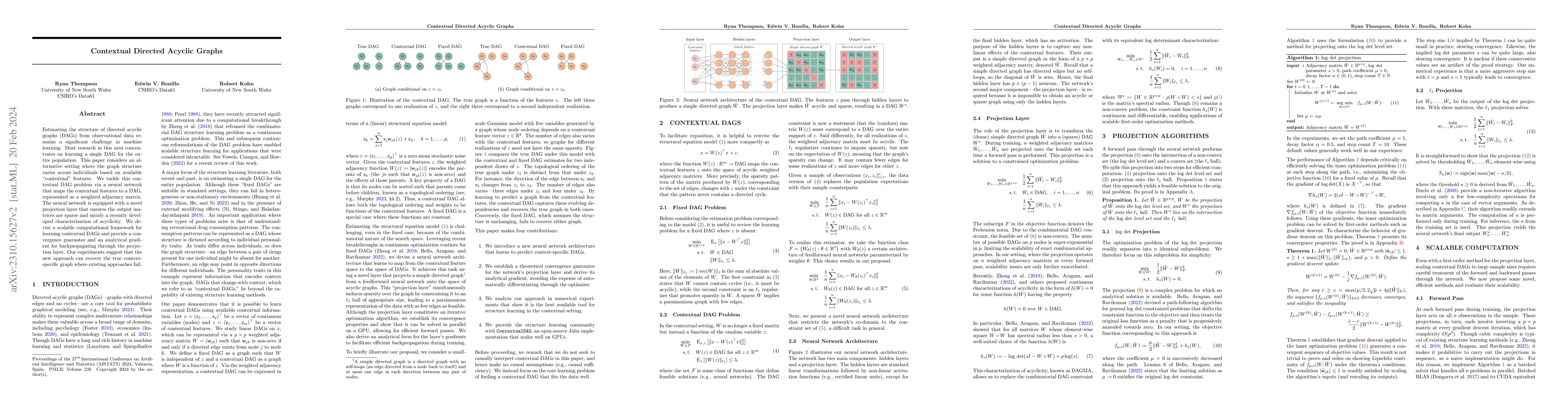

Estimating the structure of directed acyclic graphs (DAGs) from observational data remains a significant challenge in machine learning. Most research in this area concentrates on learning a single D...

For years, researchers investigated the applications of deep learning in forecasting financial time series. However, they continued to rely on the conventional econometric approach for model trainin...

Sequential Monte Carlo squared (SMC$^2$; Chopin et al., 2012) methods can be used to sample from the exact posterior distribution of intractable likelihood state space models. These methods are the ...

The Mean Field Variational Bayes (MFVB) method is one of the most computationally efficient techniques for Bayesian inference. However, its use has been restricted to models with conjugate priors or...

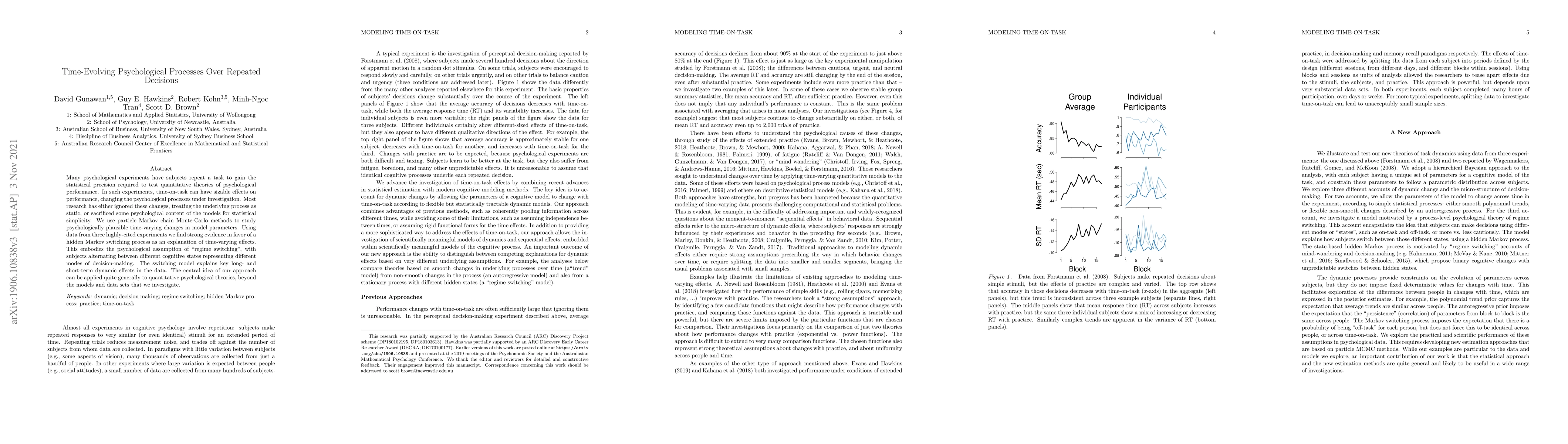

Evidence accumulation models (EAMs) are an important class of cognitive models used to analyze both response time and response choice data recorded from decision-making tasks. Developments in estima...

We propose a new approach to volatility modeling by combining deep learning (LSTM) and realized volatility measures. This LSTM-enhanced realized GARCH framework incorporates and distills modeling ad...

We provide a general solution to a fundamental open problem in Bayesian inference, namely poor uncertainty quantification, from a frequency standpoint, of Bayesian methods in misspecified models. Wh...

Although there is much recent work developing flexible variational methods for Bayesian computation, Gaussian approximations with structured covariance matrices are often preferred computationally i...

Sparse linear models are one of several core tools for interpretable machine learning, a field of emerging importance as predictive models permeate decision-making in many domains. Unfortunately, sp...

Doubly intractable models are encountered in a number of fields, e.g. social networks, ecology and epidemiology. Inference for such models requires the evaluation of a likelihood function, whose nor...

In materials that undergo martensitic phase transformation, macroscopic loading often leads to the creation and/or rearrangement of elastic domains. This paper considers an example {involving} a sin...

Sequential Monte Carlo squared (SMC$^2$) methods can be used for parameter inference of intractable likelihood state-space models. These methods replace the likelihood with an unbiased particle filt...

Particle Marginal Metropolis-Hastings (PMMH) is a general approach to Bayesian inference when the likelihood is intractable, but can be estimated unbiasedly. Our article develops an efficient PMMH m...

A mixture of experts models the conditional density of a response variable using a mixture of regression models with covariate-dependent mixture weights. We extend the finite mixture of experts mode...

Variational Bayes methods approximate the posterior density by a family of tractable distributions whose parameters are estimated by optimisation. Variational approximation is useful when exact infe...

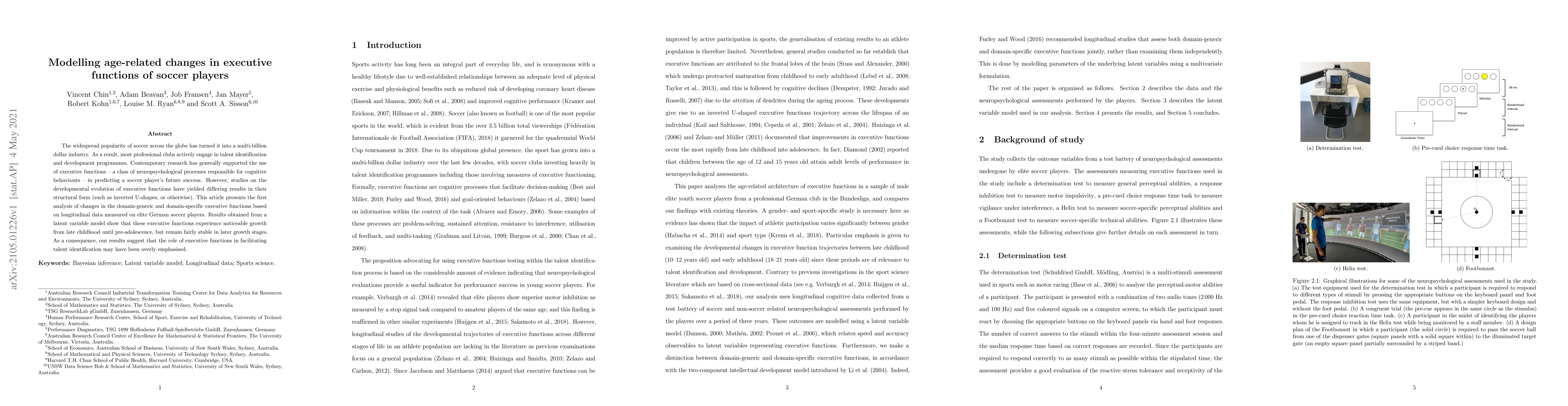

The widespread popularity of soccer across the globe has turned it into a multi-billion dollar industry. As a result, most professional clubs actively engage in talent identification and development...

Spectral subsampling MCMC was recently proposed to speed up Markov chain Monte Carlo (MCMC) for long stationary univariate time series by subsampling periodogram observations in the frequency domain...

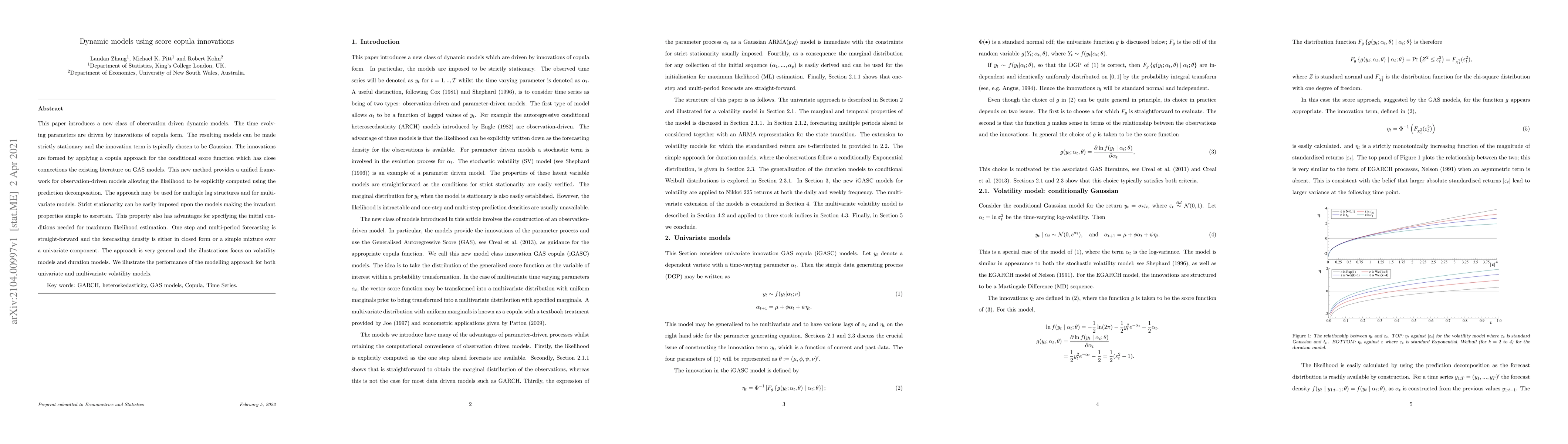

This paper introduces a new class of observation driven dynamic models. The time evolving parameters are driven by innovations of copula form. The resulting models can be made strictly stationary an...

Estimation and prediction in high dimensional multivariate factor stochastic volatility models is an important and active research area because such models allow a parsimonious representation of mul...

This article investigates retirement decumulation behaviours using the Grouped Fixed-Effects (GFE) estimator applied to Australian panel data on drawdowns from phased withdrawal retirement income pr...

Can uncertainty about credit availability trigger a slowdown in real activity? This question is answered by using a novel method to identify shocks to uncertainty in access to credit. Time-variation...

Bayesian inference using Markov Chain Monte Carlo (MCMC) on large datasets has developed rapidly in recent years. However, the underlying methods are generally limited to relatively simple settings ...

Faltering growth among children is a nutritional problem prevalent in low to medium income countries; it is generally defined as a slower rate of growth compared to a reference healthy population of...

Many psychological experiments have subjects repeat a task to gain the statistical precision required to test quantitative theories of psychological performance. In such experiments, time-on-task ca...

We show how to speed up Sequential Monte Carlo (SMC) for Bayesian inference in large data problems by data subsampling. SMC sequentially updates a cloud of particles through a sequence of distributi...

Density tempering (also called density annealing) is a sequential Monte Carlo approach to Bayesian inference for general state models; it is an alternative to Markov chain Monte Carlo. When applied ...

Particle Markov Chain Monte Carlo (PMCMC) is a general computational approach to Bayesian inference for general state space models. Our article scales up PMCMC in terms of the number of observations...

Hamiltonian Monte Carlo (HMC) samples efficiently from high-dimensional posterior distributions with proposed parameter draws obtained by iterating on a discretized version of the Hamiltonian dynami...

Copulas are now frequently used to construct or estimate multivariate distributions because of their ability to take into account the multivariate dependence of the different variables while separat...

Inference for locally stationary processes is often based on some local Whittle-type approximation of the likelihood function defined in the frequency domain. The main reasons for using such a likelih...

Dynamic linear regression models forecast the values of a time series based on a linear combination of a set of exogenous time series while incorporating a time series process for the error term. This...

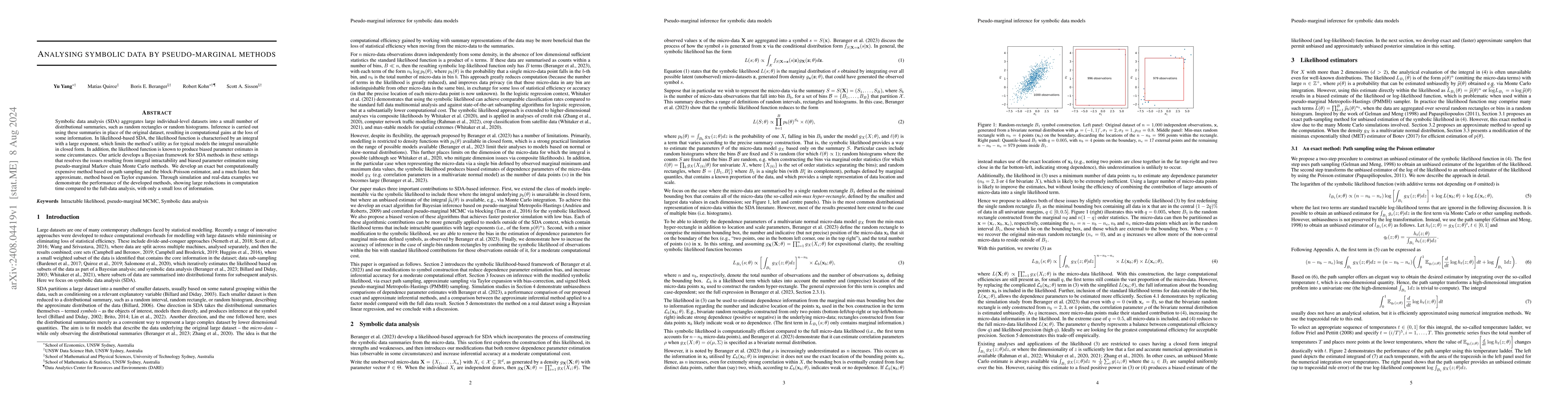

Symbolic data analysis (SDA) aggregates large individual-level datasets into a small number of distributional summaries, such as random rectangles or random histograms. Inference is carried out using ...

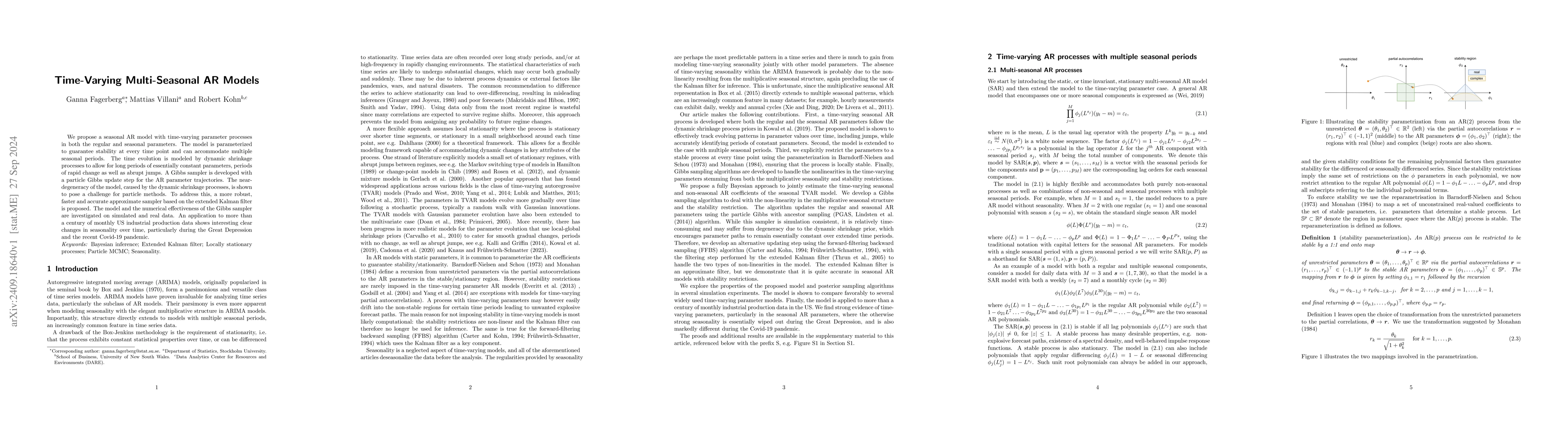

We propose a seasonal AR model with time-varying parameter processes in both the regular and seasonal parameters. The model is parameterized to guarantee stability at every time point and can accommod...

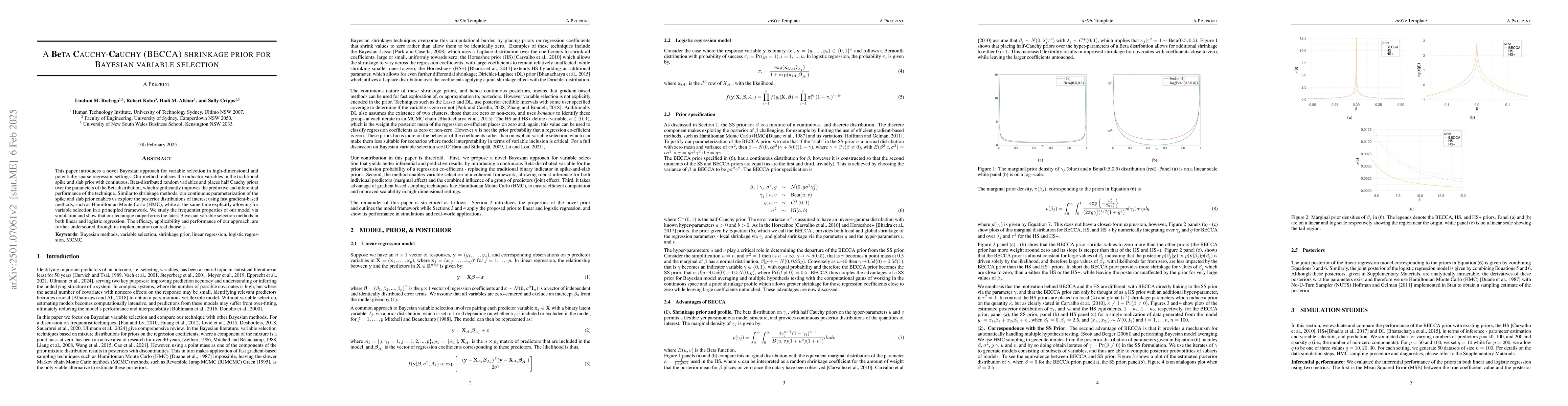

This paper introduces a novel Bayesian approach for variable selection in high-dimensional and potentially sparse regression settings. Our method replaces the indicator variables in the traditional sp...

We consider the problem of estimating complex statistical latent variable models using variational Bayes methods. These methods are used when exact posterior inference is either infeasible or computat...

Bayesian inference for stationary random fields is computationally demanding. Whittle-type likelihoods in the frequency domain based on the fast Fourier Transform (FFT) have several appealing features...

Subsampling-based Markov chain Monte Carlo (MCMC) algorithms aim to accelerate Bayesian inference by evaluating the likelihood using only a subset of the data at each iteration. However, in many stand...